By Hok Yean CHEE

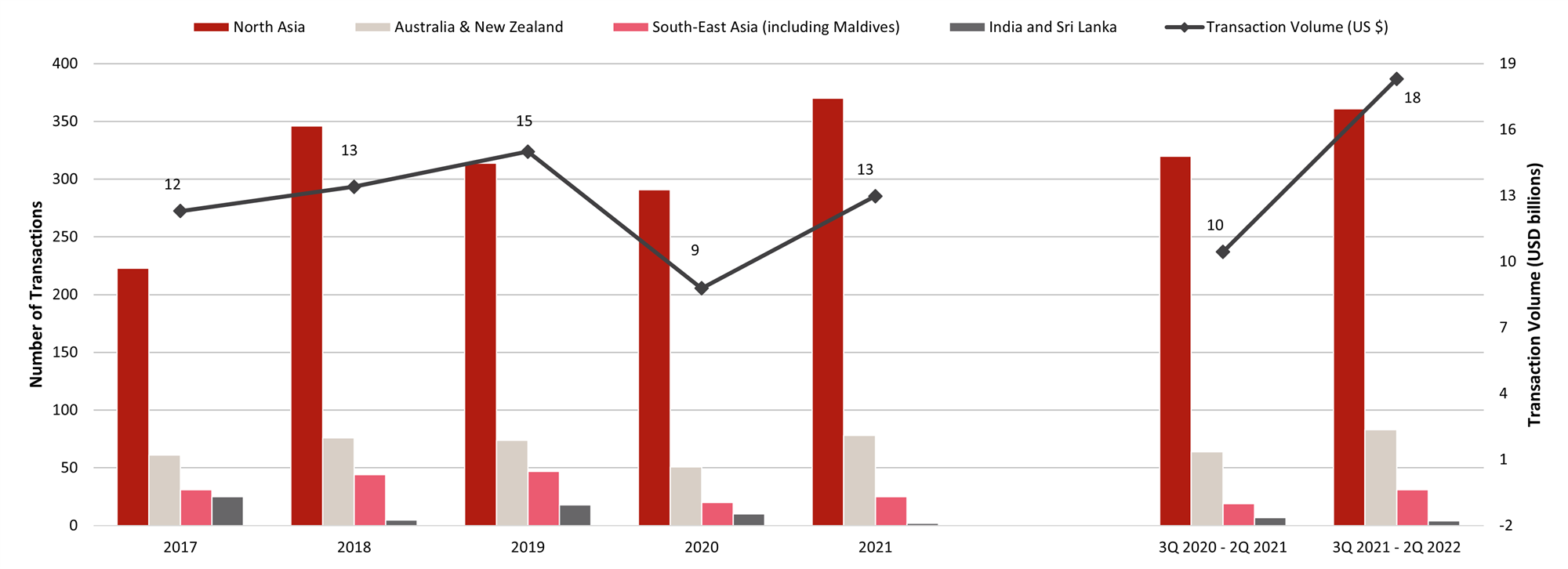

In 2021, transaction activity in the Asia Pacific recorded a strong recovery, achieving a transaction volume of approximately USD13 billion worth of hospitality assets, indicating a 47.7% growth year-on-year. Similarly, from 3Q 2021 to 2Q 2022, transaction activity in the Asia Pacific has continued to escalate by 16.8% compared to 3Q 2020 to 2Q 2021. Specifically, growing interest in hospitality assets continues to be observed in markets such as Hong Kong SAR, China, Japan, Indonesia, Thailand, Singapore, and certain markets in the South-East Asia regions.

Australia, New Zealand, and South-East Asia saw an upswing mainly attributed to the reopening of international borders and dropping of COVID-19 restrictions which revitalised international travel and enhanced market performance growth. Improvement was also observed in North Asia as many investors would like to take the opportunity to purchase valuable hospitality assets at a discounted price during the pandemic. Investment interest is anticipated to pick up even more in the second half of 2022 as investors continue to seize opportunities to tap on the gradual recovery of the tourism sector, albeit with a cautious approach.

Transaction History in the Asia Pacific (2017 – 2Q 2022)

Source: HVS Research

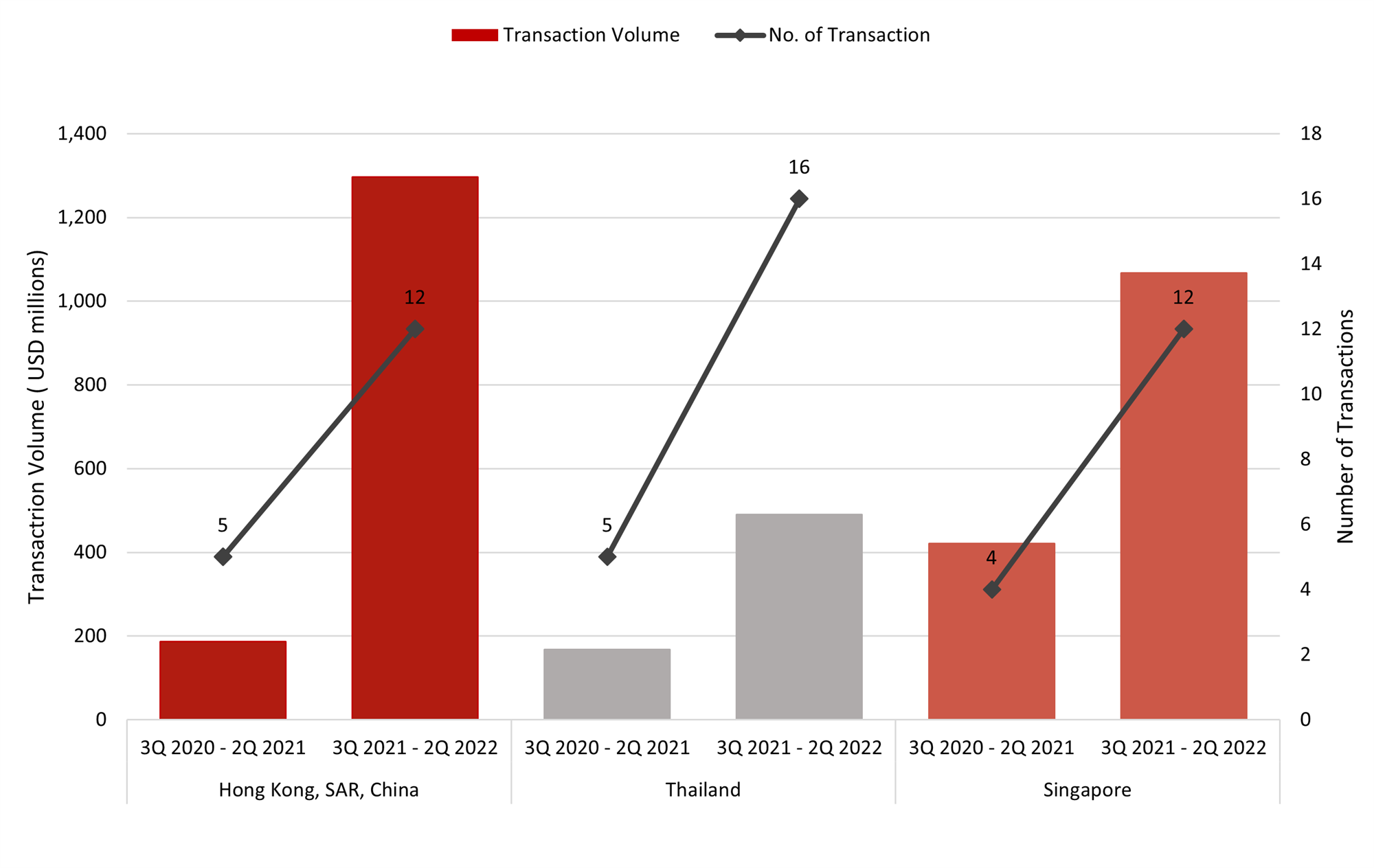

Top Three Most Active Markets (3Q 2021 to 2Q 2022)

Both transaction activity by the number of completed transactions and transaction volume for hospitality assets is observed to rapidly increase over the last four quarters (3Q 2021 – 2Q 2022) in Hong Kong SAR, Thailand, and Singapore. In particular, Hong Kong SAR has seen transaction volume increase six times from USD0.2 billion to USD1.3 billion with 12 hospitality assets traded hands. The strong investor appetite is mainly contributed by foreign investors.

Transaction Volume in Top Three Most Active Markets (3Q 2021- 2Q 2022)

Source: HVS Research

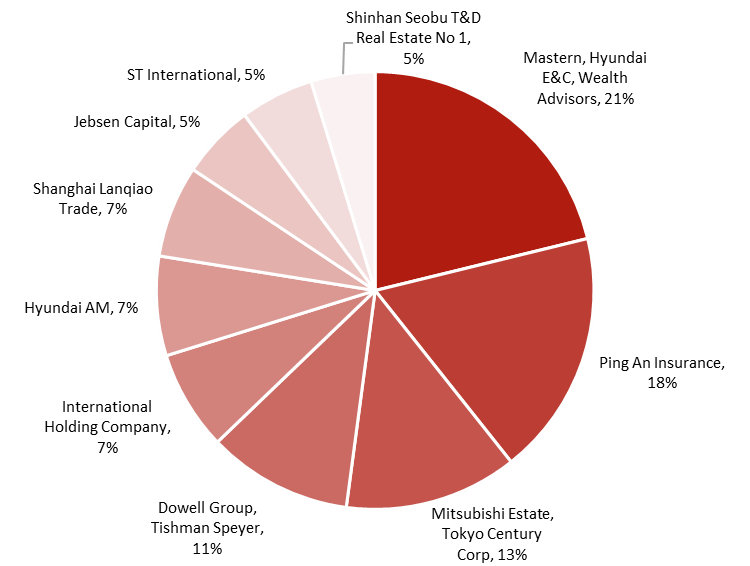

Major Investors in the Asia Pacific

In 2021, transaction activity from the top ten investors in the Asia Pacific accounted for approximately USD2.96 billion or 24.1% of total transaction volume. The majority of the transaction volume by the top ten investors are local investments (investments in the country of origin), representing approximately USD2.4 billion. Despite the coronavirus pandemic, there is an increasing interest from foreign investors. In terms of the transaction activity by the number of transactions, Japan-based Kenedix tops the list with ten deals in Japan while US-based Blackstone recorded eight in Japan. This is followed by India-based Express Group of Hotels which recorded seven in India. China-based Ping An Insurance, South Korea-based One Holdings Co, Hong Kong-based Sure Spread Limited, and Japan-based APA Group have each recorded five in 2021.

Top Ten Investors

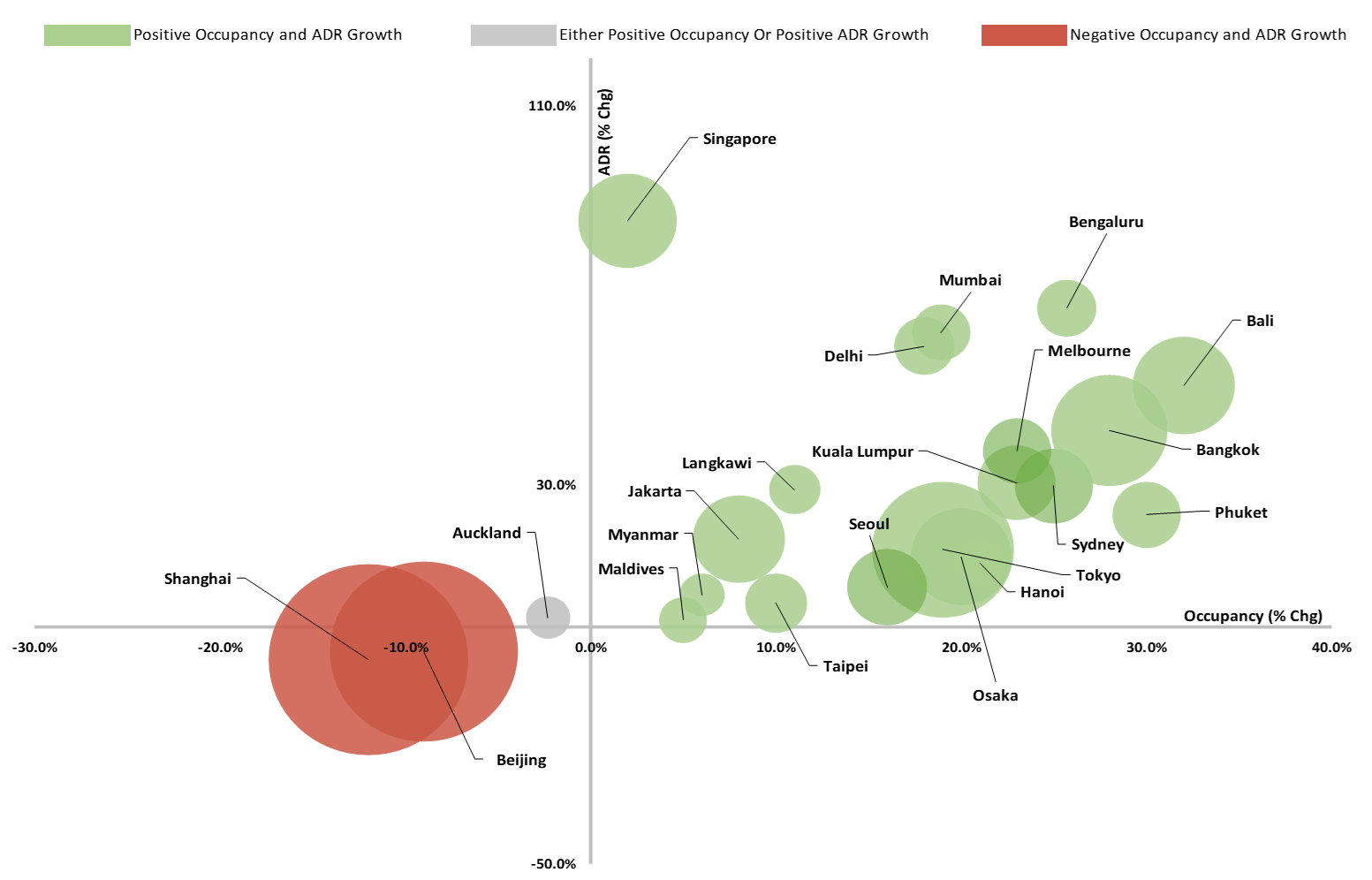

Hotel Performance in the Asia Pacific (2022)

Overall hotel performance across the tracked markets in 2022 is anticipated for a recovery phase from the impacts of the COVID-19 pandemic. Most tracked markets emerge to be more resilient and rebound faster due to earlier ease of Covid restrictions and reopening its borders to travelers after successfully controlling the spread of the coronavirus and extensive tourism sector support from the government. On the other hand, China markets face more challenges due to the zero covid approach, which includes prolonging strict lockdown, travel restrictions, and social distancing measures.

The top five market growth in hotel performances are Bali, Phuket, Bangkok, Kuala Lumpur, and Ho Chi Minh City, while static markets are Shanghai, Beijing, and Auckland. In general, hotel performance in Southeast Asia is forecasted to improve from 2021. The overall sentiment in Myanmar seems to be bearish due to the aftermath of the military coup. Similar to the case of the Maldives tourism recovery, resort locations are anticipated to rebound relatively faster as the pent-up demand from overseas is evident from the rapid growth of hotel performances in resort destinations as of YTD June 2022.

Hotel Performance in the Asia Pacific (2022)

Australia

Key Points

- Tourism contributed 4.7% to GDP in 2021, down from 9.3% in 2019

- 3.0% Real GDP growth is expected in 2022

- 700 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 8,164,673

- Active Cases: 247,128

Infrastructure Projects

- AUD5.3 billion construction of Sydney West Airport by 2026

- AUD10 billion Melbourne Airport Rail Link to connect to entire Victoria state by 2029

- Third runway construction for Melbourne Airport by 2030

Notable Upcoming Hotel Openings in Sydney and Melbourne (2022)

Top 3 Largest Inventory

- Meriton Suites Melbourne, 298 keys

- 388 William, 288 keys

- MOXY South Yarra, 180 keys

Notable Transactions

- 587-key Hilton Sydney transacted at AUD530 million (AUD903k/key) in May 2022

- 59-key Hotel Lindrum transacted at AUD50 million (AUD847k/key) in Mar 2022

- 436-Key Sofitel Wentworth Sydney transacted at AUD315 million (AUD722k/key) in Mar 2022

Demand

In 2021, total tourist arrivals contracted marginally by 0.2% year-on-year. While international arrivals have decreased by 85.4%, domestic arrivals have increased by 21.2% in 2021. As of year-to-date (YTD) May 2022, international arrivals have increased 784.5% as the Australian government moved towards ‘live with COVID’ in November 2021 and opened its international border in February 2022. Leisure, corporate and group travellers have been returning to Australia with various large-scale events and conferences occurring in Australia.

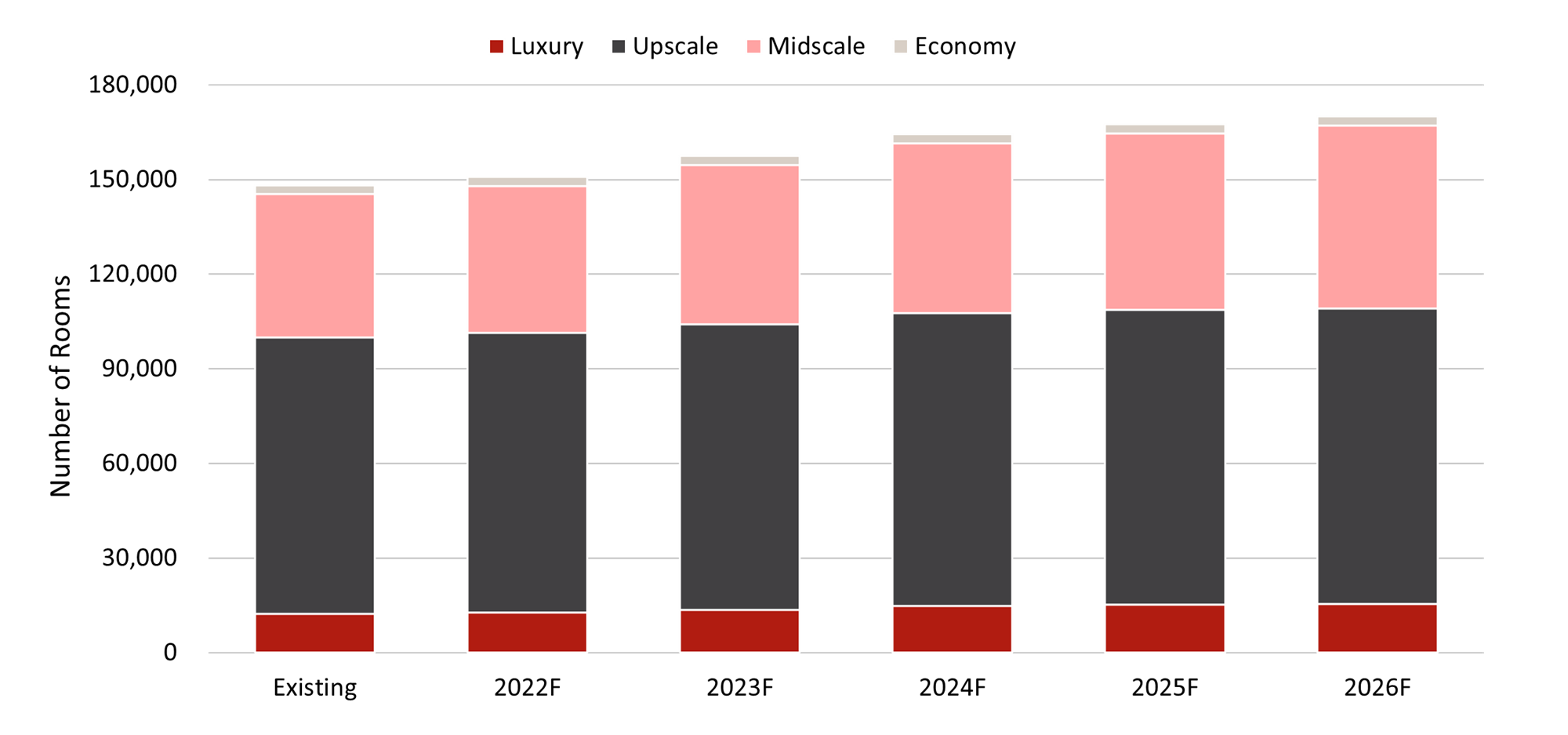

Supply

*Include non-branded hotels

Source: HVS Research

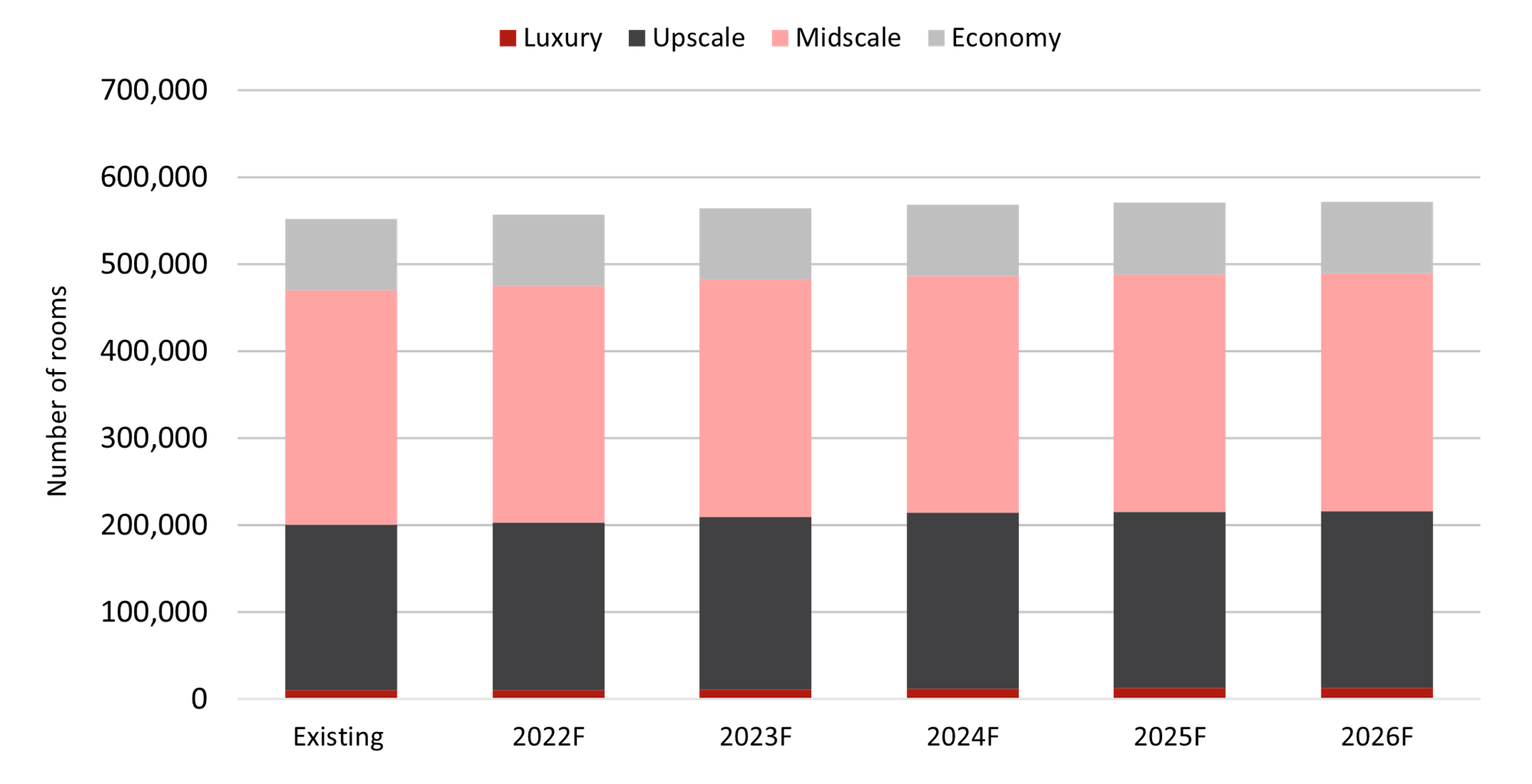

HVS has noted that there will be 124 additional hotels with approximately 21,906 keys by 2026; 17 properties with a total of approximately 2,760 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

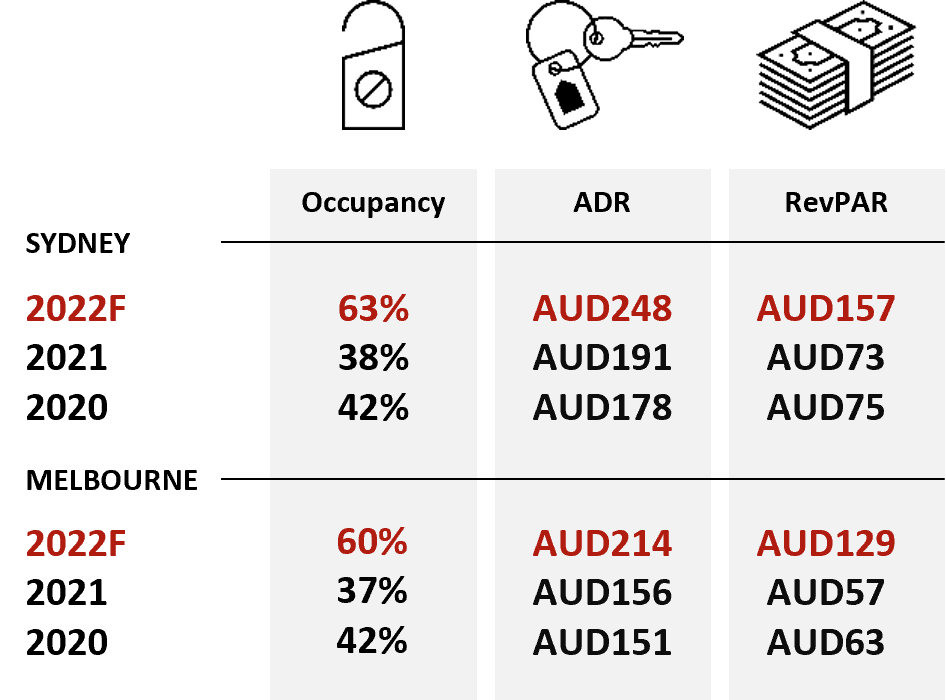

Hotel Performance

Source: HVS Research

As of YTD June 2022, hotel occupancy in Sydney and Melbourne increased by 10.9 percentage points (p.p.) and 12.0 p.p y-o-y, respectively. Sydney’s ADR and RevPAR increased by 21.4% and 50.4% y-o-y. Similarly, Melbourne’s ADR and RevPAR increased by 33.4% and 71.4%. Australia has welcomed international travellers since February 2022, which has improved the occupancy and ADR.

Transactions

From 2017 to YTD June 2022, New South Wales has recorded the highest transaction value, amounting to 45% of the total amount in Australia. This is followed by Queensland with 21% and Victoria with 21%. Transaction levels in 2021 recorded a 129% y-o-y increase. As of YTD June 2022, the total transaction volume has reached AUD2.3 billion with large portfolio sales including Travelodge Australia Hotel Portfolio sale.

Source: HVS Research

China

Key Points

- Tourism contributes 4.6% to GDP in 2021, down from 11.6% in 2019

- 4.0% Real GDP growth expected in 2022

- 3.3 billion domestic tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 888,657

- Active Cases: 426

Infrastructure Projects

- The 14th Five-Year Plan: Digital China Development

- National 5G Network Coverage

- Big Data Centre

- AI Implication

- RMB141 billion Chongqing-Kunming High-Speed Railway by 2025

- RMB123 billion Shenzhen Bao’an Airport Third Runway Expansion by 2025

Notable Upcoming Hotel Openings in Beijing and Shanghai (2022)

Top 3 Largest Inventory

- Harbour Plaza Metropolitan Shanghai, 792 keys

- Somerset Pudong Riverside Shanghai, 602 keys

- HUALUXE Shanghai Pudong Kangqiao, 586 keys

Notable Transactions

- 631-key Hyatt on the Bund sold for RMB4.5 billion (RMB7.1m/key) in Feb 2022

Demand

In 2019, international inbound tourist arrivals displayed a 2.9% y-o-y growth. Arrivals from Hongkong, Macau, and Taiwan account for 78.1% of the total inbound arrivals. Domestic visitors continue to play a major role as they account for 97.4% of the total visitor arrivals with 7.8% y-o-y growth. China’s domestic tourism is expected to dominate the market with the international border remaining shut. In 2021, more than 3.3 billion domestic tourists were recorded, displaying a 12.6% y-o-y growth.

Supply

Source: Ministry of Culture and Tourism of the People’s Republic of China

HVS has noted that going forward, there will be 1,994 additional hotels with approximately 403,046 keys in China by 2026; 404 hotels with approximately 80,116 keys in China will be opened by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

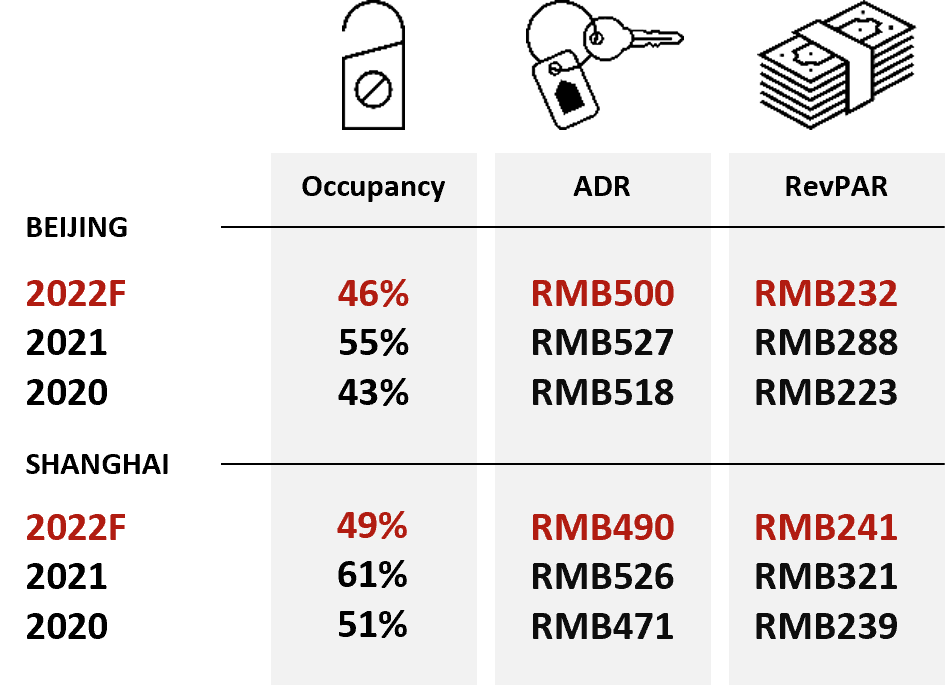

The Chinese market is greatly affected by the COVID spikes in 2022. As of YTD June 2022, the occupancy in Beijing and Shanghai has decreased by 12.2 p.p. and 12.8 p.p. respectively. ADR has also decreased for both cities, resulting in a decline in RevPAR for Beijing and Shanghai by 30.2% and 29.4% respectively.

Transactions

Hotel transactions has peaked in 2018, reaching almost RMB35 billion in total. The transaction volume in 2020 halved with the outbreak of the pandemic, but it has risen back to RMB25 billion in 2021. As of YTD June 2022, 20 transactions were recorded with a total volume of RMB7.7 billion. The RMB4.5 billion sale of Hyatt on the Bund in February 2022 marked the highest sale in China in five years.

Source: HVS Research

Hong Kong

Key Points

- Tourism contributed 3.2% to GDP in 2021, down from 12.1% in 2019

- 0.8% Real GDP growth is expected in 2022

- 28 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 1,245,797

- Active Cases: 34,708

Infrastructure Projects

- HKD42.4 billion is budgeted for the construction of the 4.7-kilometre Central Kowloon Route Highway by 2025

- Northern Metropolis Development Strategy: to establish the northern economic belt for new town development and to enhance HK-China integration under Hong Kong 2030+

- Northern Link and Tung Chung Line Extension by 2030

Notable Upcoming Hotel Openings in Hong Kong (2022)

Top 3 Largest Inventory

- Regal Hong Kong, 1000 keys

- TRIBE Hong Kong Kowloon, 324 keys

- The Mosaic Collection Y Hotel Hong Kong, 96 keys

Notable Transactions

- 388-key Hotel Sav transacted for HKD1.6 billion (HKD4.2m/key) in Mar 2022

- 162-key Travelodge Central Hollywood Road transacted for HKD850 million (HKD5.7m/key) in Jan 2022

Demand

In the year 2021, the number of visitors to Hong Kong registered a 99.2% decrease, from 3.6 million visitors in 2020 to 28,000 visitors in 2021. However, as of YTD May 2022, visitor arrivals have observed a 252.7% increase when compared to YTD May 2021, recording 18,710 visitors. This is largely attributed to the border closures enforced in March 2020 due to the coronavirus pandemic. While there is no concrete plan for Hong Kong to re-open its border with Mainland China and the world, 92.9% of the population in Hong Kong has received at least 1 dose of the vaccination. Hong Kong Tourism Board has introduced HKD30 million ‘Hot Summer Deals’ with limited quota offers across retail dining and attractions in Hong Kong as well as Staycation offers to revitalize the local tourism demand.

Supply

*Include non-branded hotels and guesthouse

Source: Hong Kong Tourism Board

HVS has noted that there will be eight additional hotels with approximately 2,330 keys in Hong Kong by 2026; three properties with a total of approximately 1,420 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: Hong Kong Tourism Board and HVS Research

As of YTD June 2022, hotel occupancy in Hong Kong increased by 7.0 p.p. Room rates followed a similar trend with an increase of 22.0%. Therefore RevPAR has registered an increase of 37.6%.

Transactions

The transaction activity in Hong Kong has been strong between 2017 and 2019, with the highest transaction volume in 2017, largely contributed by the Intercontinental hotel deal. The observed decline in 2020 and 2021 is largely attributed to the Hong Kong protests and the COVID-19 pandemic. However, YTD June 2022 transaction volume has almost reached the level of 2018.

Source: HVS Research

India

Key Points

- Tourism contributed 5.8% to GDP in 2021, down from 7.0% in 2019

- 7.4% GDP growth is expected in 2022

- 1.4 million international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 43,469,234

- Active Cases: 104,555

Infrastructure Projects

- National Infrastructure Pipeline for FY2019-25 with investments worth INR111 trillion (USD1.5 trillion).

- INR1 trillion (USD13.5 billion) in setting up 100 new airports by 2024.

Notable Upcoming Hotel Openings in New Delhi, Mumbai, and Bengaluru (2022)

- Fortune Park, New Delhi, 70 keys

- Lemon Tree Kalina, Mumbai, 70 keys

- ibis Styles Hebbal, Bengaluru, 154 keys

Notable Transactions

- EaseMyTrip acquired Spree Hospitality, a hospitality management company, at INR182.5 million (USD2.4 million) in Nov 2021

- Sayaji Hotels acquired a majority stake in Intellistay Hotels for an undisclosed sum in Nov 2021

- Express Group of Hotels acquired the Neesa Leisure India Hotel portfolio for an undisclosed sum in Jan 2021

Demand

India started its COVID vaccination drive in January 2021 and had administered 1.45 billion doses by 31 December 2021. This helped in the recovery of domestic travel demand – both leisure and business. Inbound tourism, however, remained subdued as scheduled commercial international flights were not resumed. As a result, tourist arrivals registered a year-on-year (y-o-y) decline of 49% in 2021. Inbound tourism is expected to recover gradually in 2022, as all scheduled international commercial flights resumed in March 2022.

Supply

Source: HVS Research

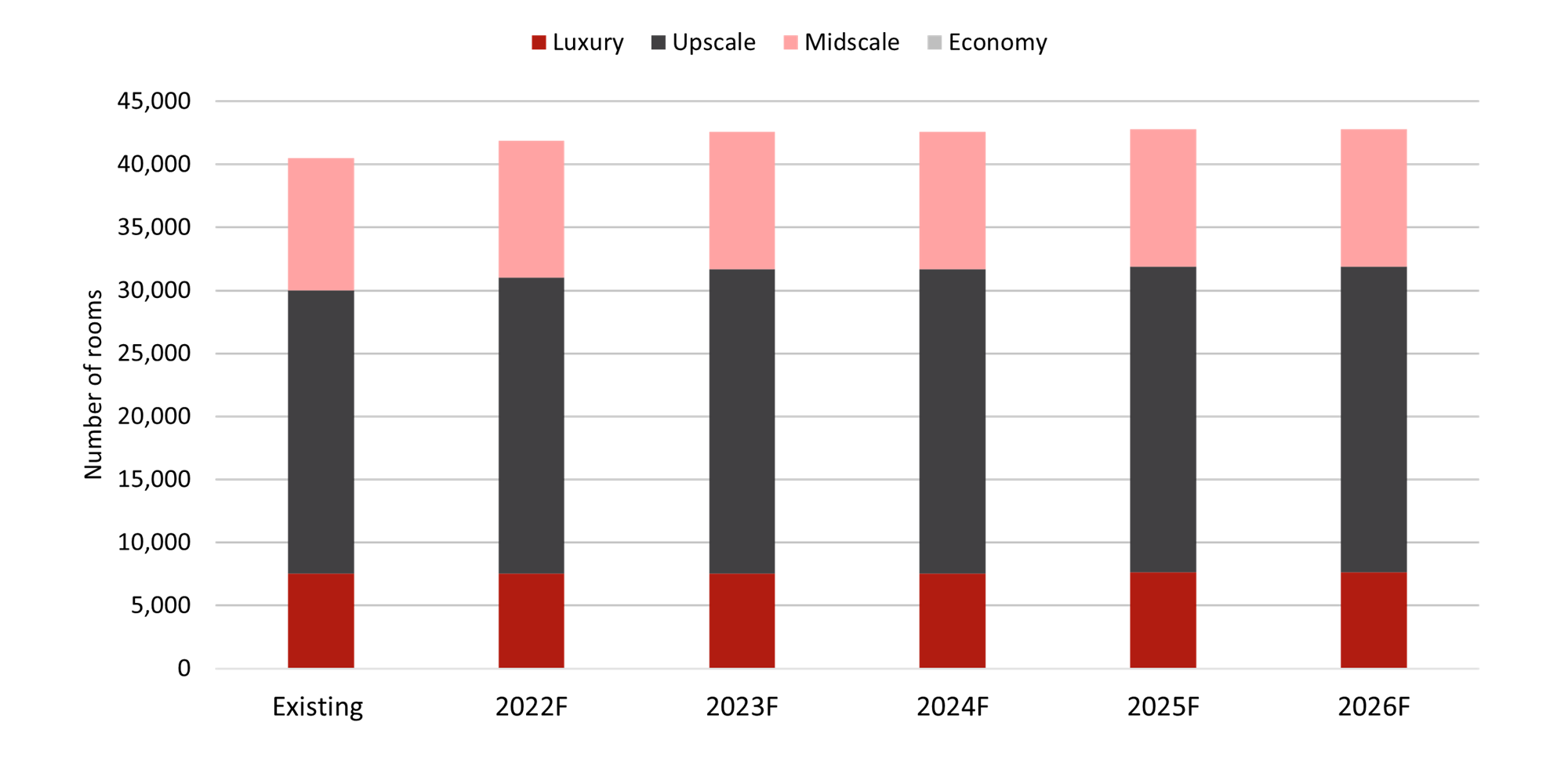

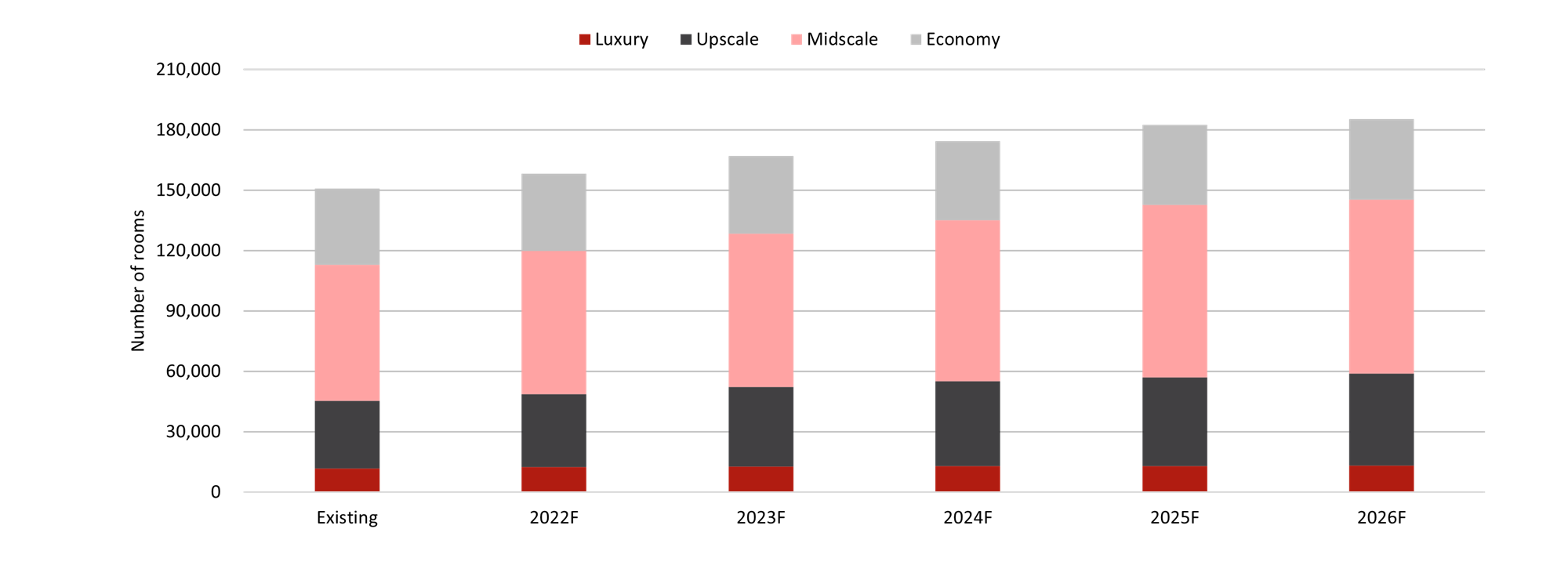

As per HVS estimates, over 41,200 additional keys will be added to the supply in India by 2026. Close to 8,800 branded keys are expected to enter the market in 2022. Hoteliers are increasing their focus on leisure destinations, and Tier 3 & 4 cities, due to the significant potential of domestic tourism.

Hotel Pipeline (2021 – 2026)

*Include only branded supply

Source: HVS Research

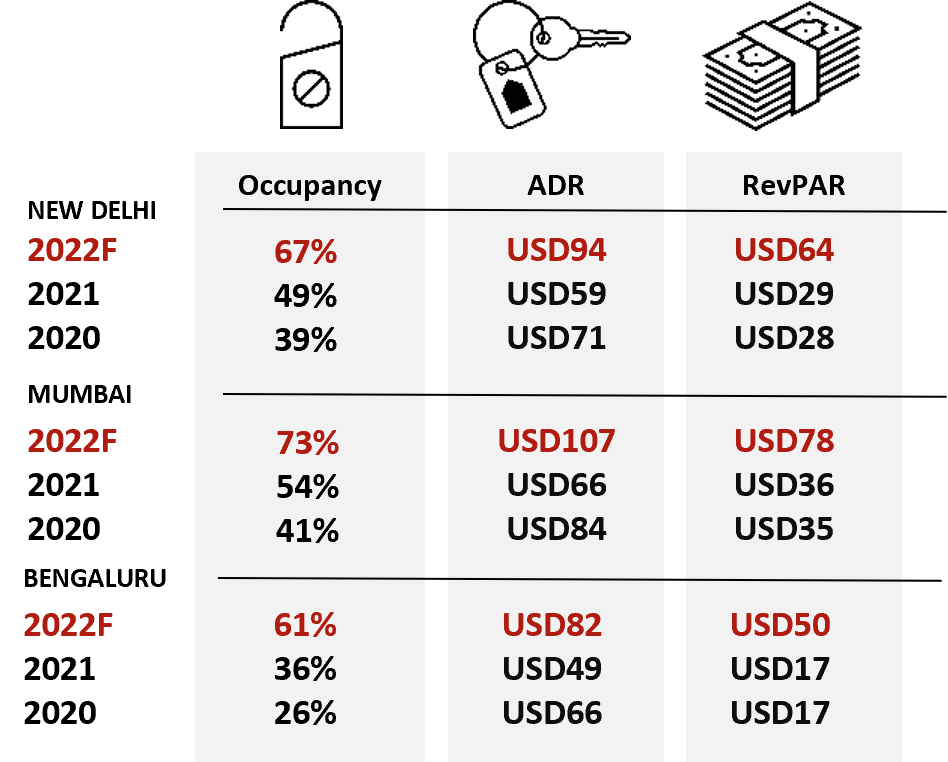

Hotel Performance

Source: HVS Research

With a significant rebound in corporate travel demand, Bengaluru’s hotel occupancy increased by 30 percentage points (pp), while occupancy in Mumbai and New Delhi increased by 25 p.p and 20 p.p, respectively. YTD June 2022 room rates in Mumbai increased by 69%, while room rates in Bengaluru and New Delhi increased by 59% and 58%, respectively.

Transactions

Hotel investments in India did not pick up significantly post-COVID. Although there are signs that investors are assessing hotel assets, buyer interest in India continues to be limited as yields remain stressed and borrowing for the sector has become even more challenging than before. Furthermore, mismatched expectations between buyers and sellers are also impeding transaction activity. Only some small ticket acquisitions were reported during 2021.

Source: HVS Research

*Exchange Rate used USD1 = INR74

Indonesia

Key Points

- Tourism contributed 2.4% to GDP in 2021, down from 5.6% in 2019

- 5.1% Real GDP growth is expected in 2022

- 1.6 million international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 6,088,460

- Active Cases: 16,790

Infrastructure Projects

- USD33 billion Trans-Sumatra Toll Road project with a total length of 2,818 km highway to be completed by 2024

- USD6.8 billion New Jakarta Airport to be completed by 2024

- USD33 billion New Capital project to shift capital from Jakarta to East Kalimantan by 2045

Notable Upcoming Hotel Openings in Bali and Jakarta (2022)

Top 3 Largest Inventory

- New World Bali, 400 keys

- Oakwood Premier Jakarta, 347 keys

- Shangri-La Bali, 339 keys

Notable Transactions

- 415-key Hotel Sofitel Bali Nusa Dua Beach Resort was acquired for IDR2.3 trillion (IDR5.5b/key) in Dec 2021

- 347-key Yogyakarta Marriott was acquired for IDR425 billion (IDR1.2b/key) in Nov 2020

- 317-key Pullman Jakarta Central Park was acquired for IDR944 billion (IDR2.9b/key) in Sep 2020

Demand

In 2021, tourist arrivals contracted by 61% y-o-y as COVID-19 led to strict travel restrictions. Malaysia remained the top source market in 2021, owning a 31% market share. Tourist arrivals are expected to gradually recover in 2022 as the border reopens and international flights resume. The number of international arrivals in Indonesia reached the highest record in May 2022 since the pandemic hit Indonesia. The occurrence indicates that the tourist arrivals are expected to pick up as the pent-up demand is evident in the market performance.

Supply

*Include non-branded hotels

Source: Statistics Indonesia

HVS has noted that there will be 205 additional hotels with approximately 34,493 keys in Indonesia by 2026; 41 hotels with approximately 7,305 keys will be opened by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

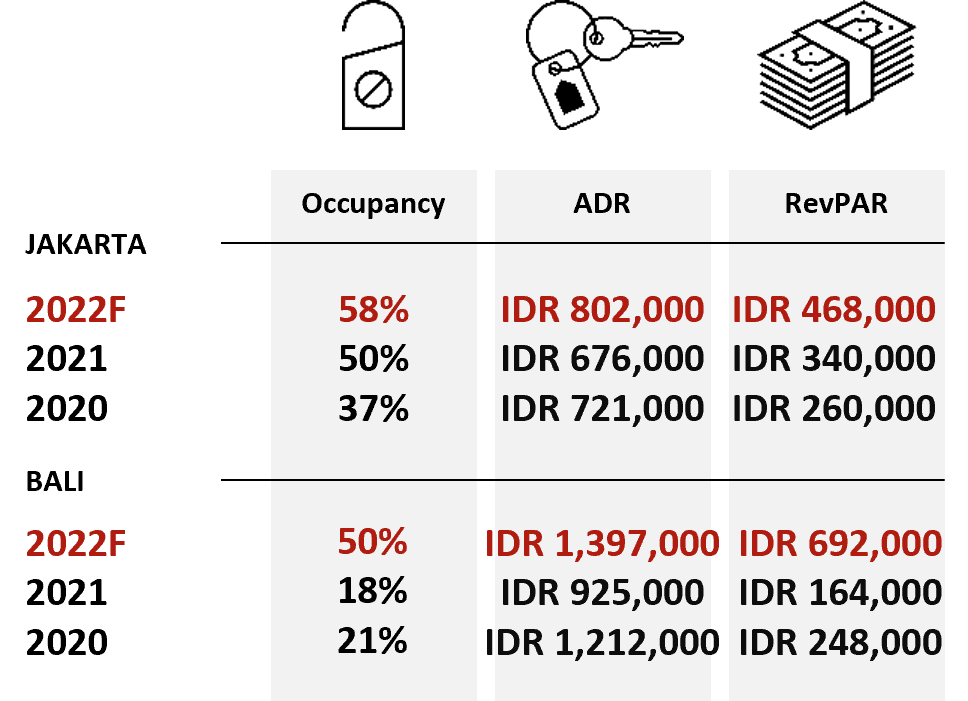

Hotel Performance

Source: HVS Research

As of YTD June 2022, Jakarta has witnessed an increase in occupancy by 7.1 p.p. while ADR has increased by 24.0%, contributing to a 41.9% increase in RevPAR. Bali market demonstrated a strong recovery due to the reopening of the border for international visitors. Occupancy and ADR in Bali have increased by 21.3 p.p. and 32.8%, respectively, resulting in a 249.1% growth in RevPAR.

Transactions

The transaction value peaked in 2018 before recording a downward trend in 2019. Four transactions totaling approximately IDR1.4 trillion were recorded in 2020. One transaction recorded in 2021, the Hotel Sofitel Bali Nusa Dua Beach Resort, was sold for approximately IDR2.3 trillion. There are no other recorded transactions as of YTD June 2022.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research

Japan

Key Points

- Tourism contributes 4.2% to GDP in 2021, down from 7.3% in 2019.

- 2.1% Real GDP growth expected in 2022

- 191 thousand international tourist arrivals recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 9,316,954

- Active Cases: 151,720

Infrastructure Projects

- JPY100 billion expansion of Kansai International Airport in Osaka by 2025

- First phase of the Maglev line by 2027 (Tokyo Shinagawa – Nagoya), 2037 (Nagoya – Shin Osaka)

Notable Upcoming Hotel Openings in Tokyo & Osaka (2022)

Top 3 Largest Inventory

- APA Hotel Roppongi Station East, 693 keys

- La Vista Tokyo Bay, 582 keys

- Via Inn Akasaka, 345 keys

Notable Transactions

- 77% interest in 100-key Hoshinoya Okinawa (Resort) acquired at JPY12.2 billion, reflecting the hotel value at JPY15.8 billion (JPY158m/key) in Jun 2022

- 206-key Ibis Tokyo Shinjuku sold for JPY11.3 billion (JPY55m/key) in Dec 2021

Demand

In 2021, tourist arrivals contracted by 95.4% y-o-y, from 4.1 million in 2020 to 190,900 in 2021. Travel restrictions and country lockdown caused by the pandemic has significantly reduced tourist arrivals. China maintained the largest source market making up 17.5% of total visitors in 2021, and Vietnam was the runner-up at 11.0%. In 2022, Japan has achieved an 81.5% vaccination rate among residents and the COVID-19 recovery rate is as high as 99.6%. Japan’s government has planned to gradually reopen borders to international visitors, travellers on guided tours were allowed to enter Japan from June 2022.

Supply

*Include non-branded hotels

Source: HVS Research

HVS has noted that going forward, there will be 93 additional hotels with approximately 20,173 keys in Japan by 2026; 28 hotels with a total of approximately 5,138 keys will be opened by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

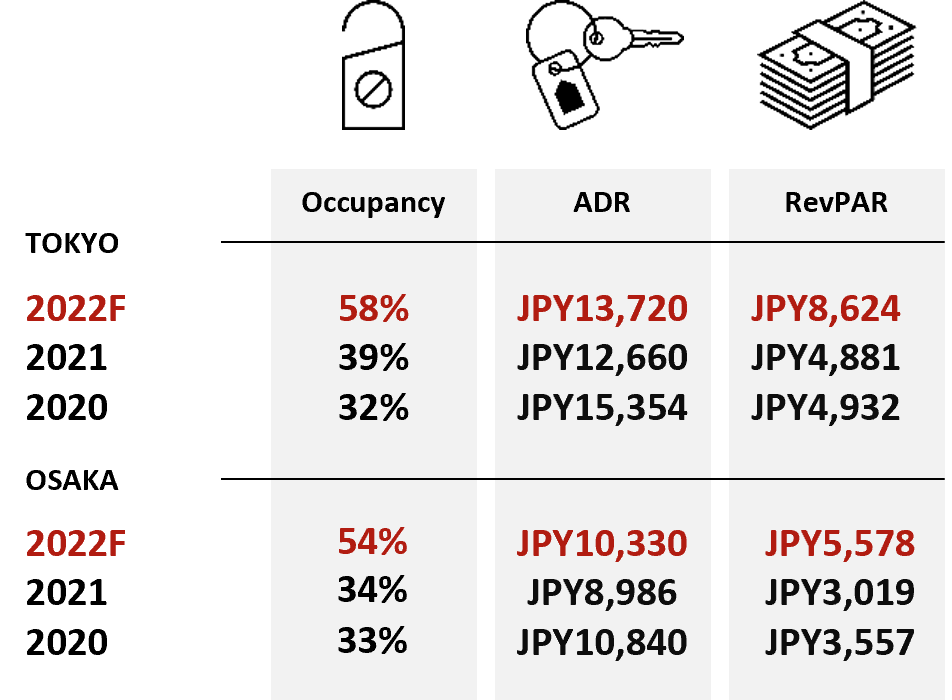

As of YTD June 2022, Tokyo and Osaka recorded a y-o-y increase in occupancy by 23.8 p.p. and 22.7 p.p respectively; ADR has also increased significantly by 11.7% and 14.5% for Tokyo and Osaka, respectively. Therefore, the RevPAR has subsequently increased by 101.2% and 117.6% for both cities.

Transactions

After reaching the peak in 2019 with a transaction volume of JPY318 billion, transactions declined to JPY131 billion in 2020 because of the pandemic. Transactions in Tokyo continued to dominate, which accounts for 20% of total recorded transactions in YTD June 2022. In February 2022, Singapore sovereign fund GIC acquired 15 hotels from Seibu Holdings at JPY143 billion, accounting for 87% of YTD June 2022 total transacted value.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research

Malaysia

Key Points

- Tourism contributes 4.1% to GDP in 2021, down from 11.7% in 2019

- 5.0% Real GDP growth expected in 2022

- 135 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 4,566,055

- Active Cases: 29,434

Infrastructure Projects

- MYR29 billion Pan Borneo Highway by 2028

- MYR31 billion construction of Mass Rapid Transit Line 3 in Kuala Lumpur City by 2030

Notable Upcoming Hotel Openings in Kuala Lumpur and Langkawi (2022)

- Holiday Inn & Suites Cyberjaya, 410 keys

- PARKROYAL Langkawi Resort, 301 keys

- Amari Eco City Kuala Lumpur, 252 keys

Notable Transactions

- 418-key Royale Chulan Bukit Bintang transacted for MYR177 million (MYR 424k/key) in Feb 2021

- 221-key Ambassador Row Hotel Suites by Lanson Place transacted for MYR80 million (MYR360k/key) in Oct 2020

Demand

In the year 2021, the number of visitors to Malaysia registered a 96.9% decline, from 4.33 million visitors in 2020 to 134.7 thousand visitors in 2021. This is largely attributed to the border closures and country lockdown enforced in 2020 and the first half of 2021 due to the coronavirus pandemic. The top three source markets for 2021 are Thailand (44.3%), Singapore (12.1%), and Indonesia (8.2%). In March 2022, Malaysia fully reopened its international border with no quarantine requirement for fully vaccinated travelers.

Supply

*Include non-branded hotels

Source: HVS Research

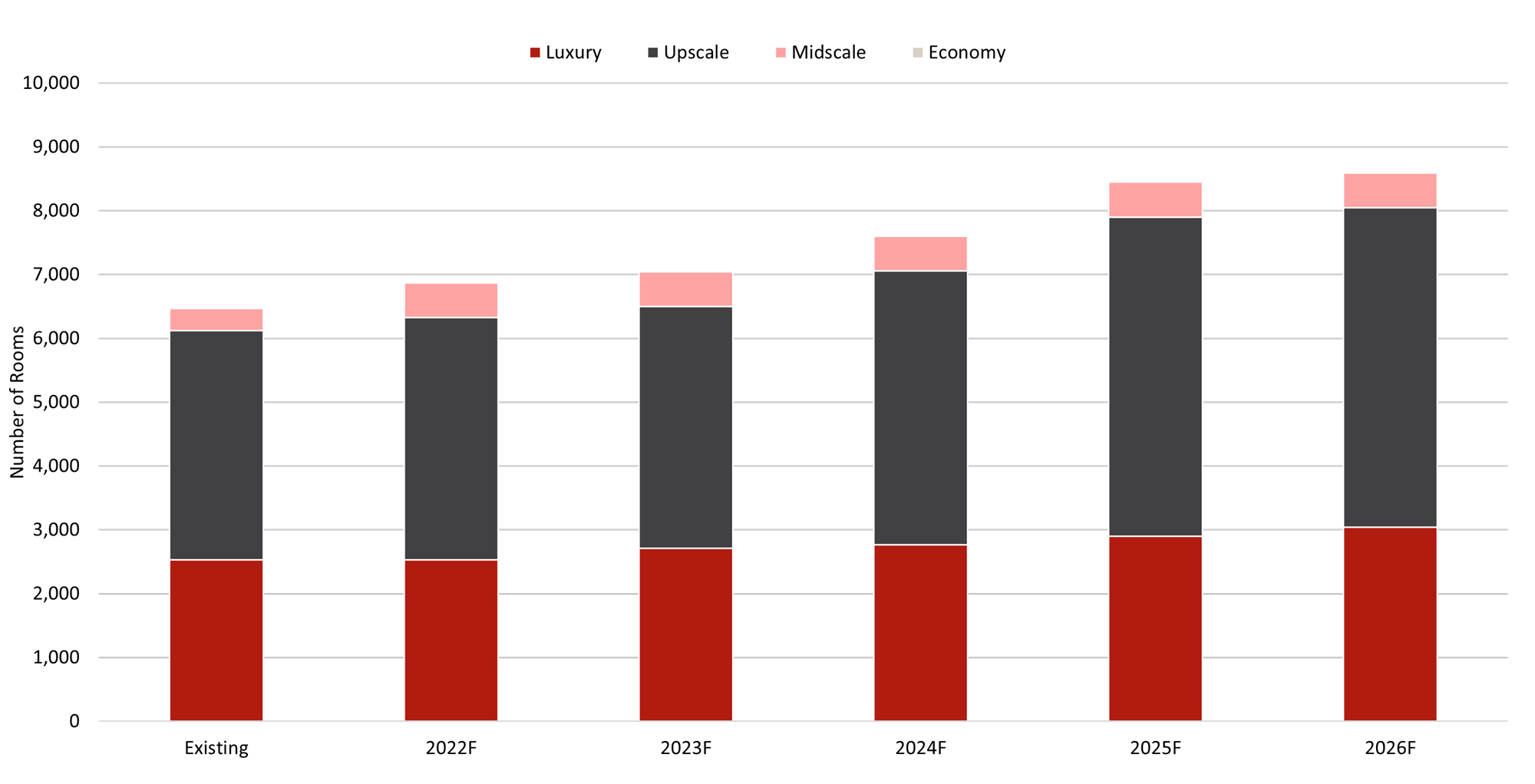

HVS has noted that going forward, there will be 96 additional hotels with approximately 23,098 keys in Malaysia by 2026; 22 properties with a total of approximately 5,770 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

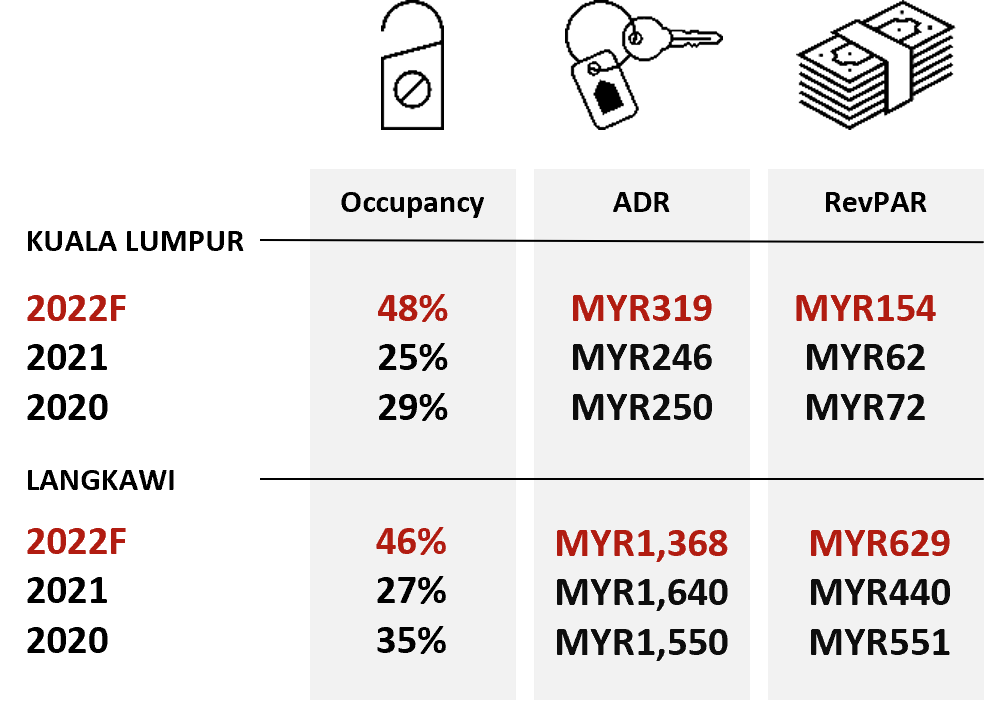

Hotel Performance

Source: HVS Research

As of YTD June 2022, Kuala Lumpur experienced an increase in occupancy of approximately 16.5 p.p., with a 39.9% increase in room rates. Therefore, the RevPAR has increased by 48.4%. Based on HVS estimates, occupancy in Langkawi is expected to increase by 11.0 p.p. in 2022, with the ADR forecasted to grow by 10.0%, resulting in a 43.5% increase in RevPAR.

Transactions

Hotel transactions in Malaysia reached approximately MYR2.7 billion in 2017. However, transaction volume has been on a decline ever since. In 2021, one hotel was transacted at MYR177 million and there were no transactions recorded for the first half of 2022. Over the last five years, Kuala Lumpur accounted for 20 of the 48 recorded transactions.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research

Maldives

Key Points

- Tourism contributed 44.6% to GDP in 2021, down from 52.6% in 2019

- 6.1% Real GDP growth is expected in 2022

- 1.3 million international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 181,586

- Active Cases: 17,594

Infrastructure Projects

- USD14.3 million Meemu Airport development project to provide a new airport in Meemu Atoll by November 2022

- USD500 million Greater Male Connectivity Project to connect Male to three neighboring islands of Villingili, Gulhifahu, and Thilafushi by 2023

Notable Upcoming Resort Openings in the Maldives (2022)

- Amari Kudu Kurathu Maldives, 200 keys

- Avani+Fares Maldives, 200 keys

Notable Transactions

- 45-key Cheval Blanc Randheli transacted at USD217.8 million (USD4.8 m/key) in June 2021

- 80-key Kanuhura Maldives transacted at USD41.5 million (USD519k/key) in May 2021

Demand

In 2021, Maldives recorded more than 1.3 million international tourist arrivals, a 138% increase compared to 2020. Maldives opened its international border and welcomed travellers from July 2020 in the midst of the pandemic. India and Russia were the top two source markets for Maldives in 2021. Although occupancy has yet to reach the pre-pandemic level, the country was able to drive a higher rate as Maldives was one of the first and only countries to open during the pandemic.

Supply

*Include non-branded hotels

Source: Maldives Ministry of Tourism

HVS has noted that there will be 17 additional hotels with approximately 2,124 keys in the Maldives by 2026; two properties with a total of approximately 400 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Resort Performance

Source: HVS Research

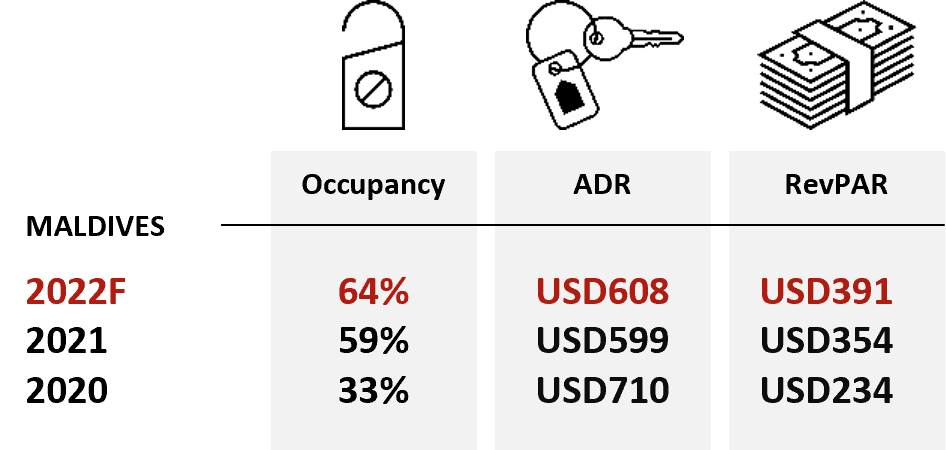

As of YTD June 2022, Maldives saw a 14.2 p.p. y-o-y increase in occupancy while ADR and RevPAR increased by 4.2% and 32.2% y-o-y. This is mainly attributed to the worldwide relatively relaxed COVID-19 quarantine requirements for international travellers. Resorts were able to capture a higher occupancy when compared to last year.

Transactions

From 2017 to YTD June 2022, Maldives has recorded a total transaction value of approximately USD1.2 billion. In June 2021, UAE-based International Holding Company acquired the Cheval Blanc Maldives for USD218 million, the largest acquisition pricing since 2017. In 1H2022, the 77-key W Maldives and 176-key Sheraton Maldives Full Moon Resort & Spa were sold as a portfolio at an undisclosed sum.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

*2022 transaction amount was not disclosed

Source: HVS Research

Myanmar

Key Points

- Tourism contributed 2.1% to GDP in 2021, down from 6.5% in 2019

- 2.8% Real GDP growth is expected in 2022

- 131 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 613,596

- Active Cases: 1,601

Infrastructure Projects

- Opening of the Hanthawaddy International Airport in the Bago Region, which is 77 kilometers north of Yangon. The new airport will have the capacity to handle 12 million visitors, scheduled to open in 2022.

Notable Upcoming Hotel Openings in Myanmar (2022)

- Centra by Centara Hotel Thiri Hpa-An, 77 keys

Notable Transactions

- 50% interest in 32-key The Strand Yangon acquired at USD358k, reflecting the hotel value at USD717k (USD22k/key) in May 2019

- 50% interest in 211-key Inya Lake Hotel acquired at USD2.4 million, reflecting the hotel value at USD4.7 million (USD22k/key) in May 2019

- 50% interest in 85-key Hotel G Yangon acquired at USD953k, reflecting the hotel value at USD1.9 million (USD22k/key) in May 2019

Demand

In 2020 and 2021, Myanmar registered a decline in tourist arrivals registering a y-o-y decline of 79.3% and 85.5% respectively. The government issued its Myanmar Tourism Strategic Recovery Roadmap in 2021 in response to the COVID-19 disrupted tourism. ‘Myanmar Tourism Board’ will be established for coordination of marketing and communication activities, tourism connectivity and accessibility will be improved, and rebuild visitor demand and improve product offerings in Myanmar.

Supply

*Include non-branded hotels

Source: HVS Research

HVS has noted that there will be ten additional hotels with approximately 1,625 keys in Myanmar by 2026; one property with a total of approximately 77 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

As of YTD June 2022, hotel occupancy and the average rate in Myanmar observed a 7.4 p.p. and 5.2% increase respectively. Therefore, the RevPAR in Myanmar has increased by 44.8%. Nevertheless, Myanmar’s hotel performance was adversely impacted by the military coup of Myanmar in February 2021.

Transactions

There is limited information on hotel transactions in Myanmar. In 2019, there were three recorded transactions in Yangon with a total transaction volume of USD3.6 million. In 2020, no hotel transactions were recorded, largely attributed to the coronavirus pandemic. Similarly, in 2021 and 2022, no hotel transactions were recorded and it is expected that foreign direct investment will continue to dwindle due to the military coup in Myanmar. Five hotel development projects that are expected to open within 2021 and 2022 have been deferred.

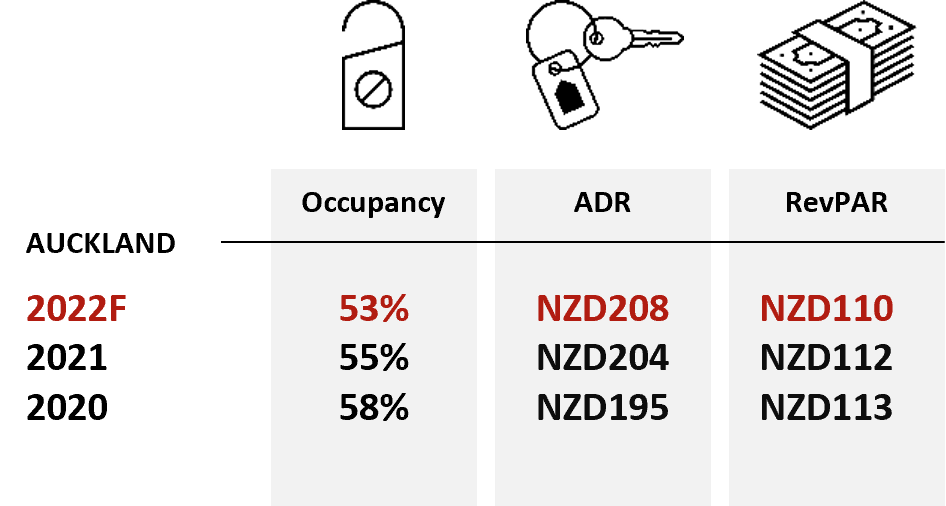

New Zealand

Key Points

- Tourism contributed 9.0% to GDP in 2021, down from 13.7% in 2019

- 2.7% Real GDP growth is expected in 2022

- 207 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 1,345,796

- Active Cases: 41,355

Infrastructure Projects

- NZD3.4 billion City Link Rail in Auckland by 2024

- NZD1.8 billion Auckland Light Rail to link CBD to Auckland Airport by 2024

- NZD1.85 billion East West Link for improved transport connection by 2025

Notable Upcoming Hotel Openings in Auckland (2022)

- SKYCITY Horizon Hotel Auckland (300 keys)

Notable Transactions

- 280-key Rydges Wellington, sold for NZD100 million (NZD357k/key) in Dec 2021

- 82-key Sofitel Queenstown Hotel & Spa sold for NZD60 million (NZD732k/key) in Dec 2020

Demand

Total tourist arrivals amounted to approximately 207,000 in 2021, a 79.2% decrease compared to 2020 due to the prolonged closed borders. Given Australia’s proximity to New Zealand, tourists from Australia remain the top source market, accounting for 78% of total arrivals in 2021. Conversely, arrivals from China, the second-largest source market in 2019, became the sixth largest source market in 2021. To revitalise the tourism industry, the New Zealand Tourism Board established various marketing campaigns and travel deals to encourage domestic tourism. They have also utilised social media marketing to attract and reach out to international tourists. As of YTD May 2022, there were 164,950 total tourist arrivals, a 57.2% increase compared to the same period last year.

Supply

*Include non-branded hotels

Source: HVS Research

HVS has noted that there will be 26 additional hotels with approximately 4,142 keys in New Zealand by 2026; Six properties with a total of approximately 682 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

As of YTD June 2022, Auckland’s occupancy recorded a y-o-y decrease of 16.7 p.p. ADR increased by 4.6%, which resulted in a 23.8% decline in RevPAR. The decrease in RevPAR may be attributed to the prolonged travel restrictions due to COVID-19 that has impacted travel demand in Auckland.

Transactions

In 2019, transaction value in the market generally saw a sharp upward trend. However, in 2020, due to COVID-19, business and economic outlook were uncertain, which contributed to a low transaction volume. New Zealand registered only two transactions in 2020 but increased to ten transactions in 2021, similar to 2018 figures.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research

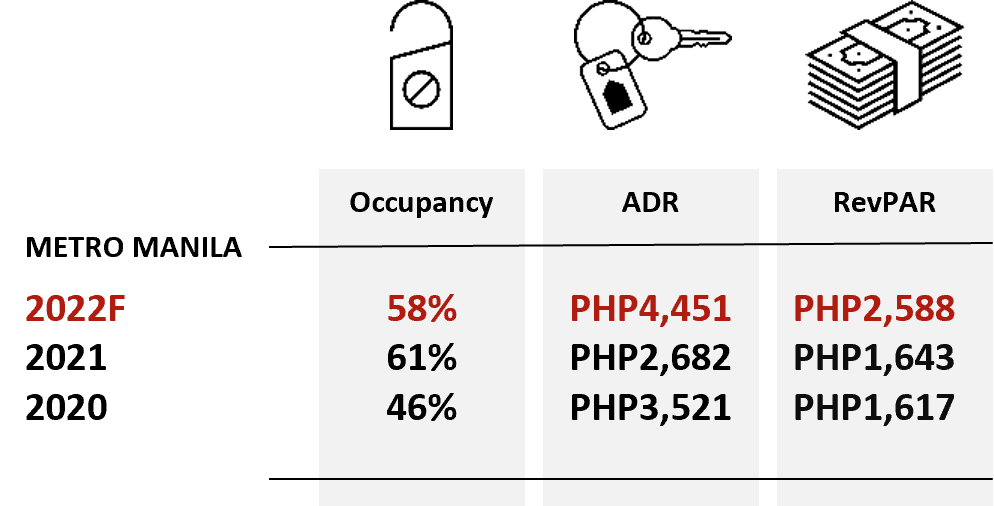

Philippines

Key Points

- Tourism contributes 10.4% to GDP in 2021, down from 22.5% in 2019

- 7.1% Real GDP growth expected in 2022

- 164 thousand international tourist arrivals recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 3,704,407

- Active Cases: 7,870

Infrastructure Projects

- PHP57 billion Clarin Bridge in Bohol Province by 2022

- PHP740 billion Bulacan Airport by 2025, backed by San Miguel Corporation

- PHP357 billion Metro Manila Subway Project by 2025, backed by Japan

Notable Upcoming Hotel Openings in Manila (2022)

Top 3 Largest Inventory

- Quest Cubao, 240 keys

- Somerset Valero Makati, 184 keys

- Novotel Suites Manila At Acqua, 152 keys

Notable Transactions

- 159-key Go Hotels Cubao transacted for PHP411 million (PHP2.6m/key) in Dec 2019

- 370-key New World Manila Bay Hotel transacted for an undisclosed price in Apr 2019

Demand

In 2021, 164,000 international tourist arrivals were recorded in the Philippines, a 90.0% decrease from 2020. This is largely attributed to the border closures enforced in March 2020 due to the coronavirus pandemic. In 2021, the USA remained as the top source market, owning a 24% market share. Japan and China became the second and third top source markets respectively, accounting for 9.2% and 5.9% of the total visitors to the Philippines respectively. The Department of Tourism has released the 2022 recovery plan with PHP3.5 billion allocated to promote the Philippines’ competitive tourism, with the main goal of mitigating the impact of the pandemic on the tourism industry.

Supply

*Include non-branded hotels

Source: HVS Research

HVS has noted that going forward, there will be 65 additional hotels of approximately 13,844 keys in the Philippines by 2026. with 14 hotels and 3,184 rooms opening in 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

As of YTD June 2022, Manila recorded a decrease in occupancy by 2.7 p.p, whereas ADR increased by 61.7% y-o-y. Therefore, RevPAR has increased by 54.0%. The international borders opening and the pent-up demand starting to flow through Manila have helped to increase the room rate.

Transactions

In 2019, we noted two hotel acquisitions by Hong Kong-based International Entertainment Corporation; the 370-key New World Manila Bay Hotel sold for an undisclosed amount, and the 159-key Go Hotels Cubao which was sold for PHP411 million. In 2020, 2021, and YTD June 2022, no transaction was recorded in the Philippines. This is largely attributed to the coronavirus pandemic and terrorism activities within the country.

Singapore

Key Points

- Tourism contributed 3.9% to GDP in 2021, down from 11.0% in 2019

- 3.6% Real GDP growth is expected in 2022

- 330 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 1,444,068

- Active Cases: 101,625

Infrastructure Projects

- Development of the Mandai eco-tourism hub by 2023 and tourism hub in Jurong Lake District by 2026, as well as the Greater Southern Waterfront and Sentosa Island

- Expected completion of the Thomson-East Coast MRT Line by 2024

- Addition of Changi Airport Terminal 5 by 2030

Notable Upcoming Hotel Openings in Singapore (2022)

Top 3 Largest Inventory

- Development on 8 Club Street, 900 keys

- Vibe Singapore Orchard, 256 keys

- Citadines Connect City Centre, 172 keys

Notable Transactions

- 45-key Hotel Soloha transacted for SGD53.4 million (SGD1.2 m/key) in May 2022

- 134-key SO/ Singapore transacted for SGD240 million (SGD1.8 m/key) in Apr 2022

Demand

In 2021, visitor arrivals recorded a y-o-y decrease of 88.0%. Despite the pandemic situation, China remained as the top source market, accounting for 26.7% of visitor arrivals. This is followed by India and Indonesia at 16.5% and 10.1% respectively. YTD June 2022 observed 1.71 million arrivals, a steep recovery of 773.8% increase compared to the same period in 2021. On 22 February 2022, Singapore removed most of its social restrictions; social distancing will not be required and there are no limitations to social gathering group sizes. The international border is fully opened to fully vaccinated travellers from April 2022, with no restriction on countries.

Supply

*Include non-branded hotels

Source: Singapore Tourism Board

HVS has noted that there will be 14 additional hotels with 3,443 keys in Singapore by 2026, and four hotels with 663 keys will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

As of YTD June 2022, Singapore observed a y-o-y decrease in market occupancy by 2.6 p.p. since most hotels have exited the quarantine business in 2022. However as the international border has re-opened, the room rates and RevPAR have increased by 77.3% and 70.6% y-o-y respectively.

Transactions

2019 observed the highest total transacted amount in five years, where ten hotels were transacted for a total of SGD2.56 billion. However, due to the pandemic in 2020, a total of SGD539 million was recorded. In 2021, six hotels were transacted at a total of SGD168 million. In YTD June 2022, transaction amounts picked up with seven hotels being transacted for SGD1.3 billion.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research

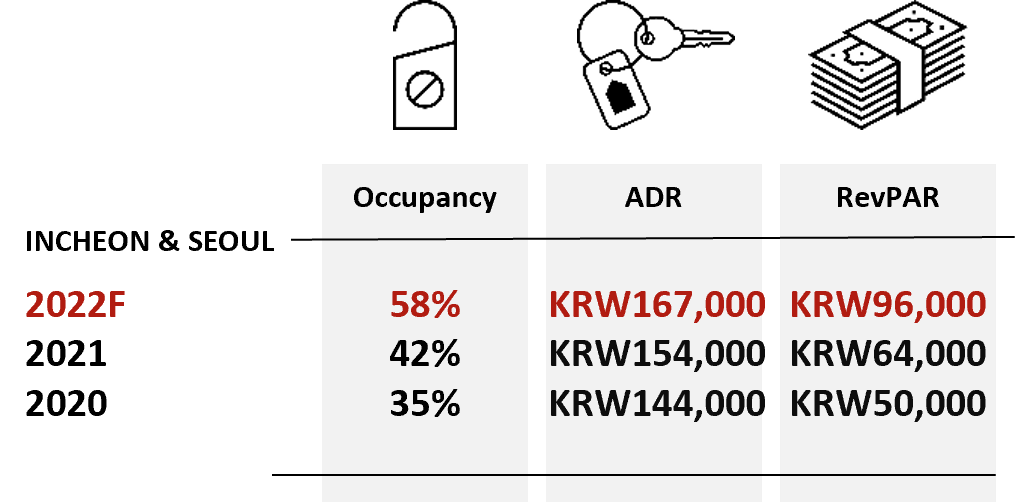

South Korea

Key Points

- Tourism contributed 2.7% to GDP in 2021, decreased from 4.4% in 2019

- 2.7% Real GDP growth is expected in 2022

- 967 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 18,368,857

- Active Cases: 133,871

Infrastructure Projects

- KRW1.3 trillion development on South Korea’s largest commercial data center by 2024 in Incheon Bupyeong-gu

- KRW13.5 trillion construction of major roads and railways including the Seoul-Sejong Expressway by 2024

- KRW4.1 trillion expansion of New Jeju International Airport by 2025

Notable Upcoming Hotel Openings in Seoul and Incheon (2022)

- MOXY Seoul Myeongdong, 209 keys

Notable Transactions

- 57-key Seoul Hilltop Hotel transacted at KRW106 million (KRW1.8 m/key) in Jun 2022

- 119-key Hotel Prima Seoul transacted at KRW409 billion (KRW3.4 m/key) in Mar 2022

- 680-key Millennium Seoul Hilton transacted at KRW1.1 trillion (KRW1.6 m/key) in Feb 2022

Demand

In 2021, international arrivals recorded a 61.6% decrease, from 2.5 million in 2020 to 967,000 in 2021. United States, previously the second top source market, rose to the top source market as China remains its zero Covid policy. United States source market accounts for 21.1% of all international arrivals. This is followed by China and Philippines, which contributed 17.6 % and 12.0%, respectively. The individual state tourism boards have since launched various support initiatives for their tourism recovery. Country-wide, South Korea’s new president has ordered a USD3.7 billion investment in the Arts, Media, and Tourism to attract international demand to visit the country.

Supply

*Include non-branded hotels

Source: HVS Research

HVS has noted that there will be 29 additional hotels with approximately 7,590 keys in South Korea by 2026; seven properties with a total of approximately 2,002 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

Hotel Performance

Source: HVS Research

As of YTD June 2022, hotel occupancy in Seoul and Incheon experienced an increase of 15.6 p.p, room rates increased by 16.0%, and RevPAR increased by 66.3% as the government relaxed all restrictions and reopened its borders to international visitors.

Transactions

South Korea, especially Seoul, registered a high value of investment activity in recent years, reflecting a good robust hotel investment market. After the lowest transaction value registered in 2017 with under KRW1 trillion, transaction value exceeded KRW2 trillion from 2019 onwards and peaked in 2021 with over KRW2.5 trillion.

Source: HVS Research

Taiwan

Key Points

- Tourism is estimated to contribute 2.1% to GDP in 2021, down from 6.0% in 2019

- 4.0% Real GDP growth expected in 2022

- 140 thousand international tourist arrivals were recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 3,767,283

- Active Cases: 1,005,098

Infrastructure Projects

- NTD45 billion Taiwan Taoyuan International Airport Terminal 3 is expected to complete construction by 2026

- NTD61.8 billion High-Speed Railway Extension to Pingtung County by 2029

Notable Upcoming Hotel Openings in Taipei (2023)

Top 3 Largest Inventory

- Hotel Indigo Qingcheng Mountain, 241 keys

- Park Hyatt Taipei, 178 keys

- Ibis Taipei National Taiwan University, 58 keys

Notable Transactions

- 257-key Ambassador Hotel Hsinchu in Hsinchu City was transacted at NTD5.8 billion (NTD22.6m/key) in Mar 2022

- 48-key Lotus Garden Hotel in Taipei was transacted at NTD730 million (NTD15.2m/key) in Nov 2021

Demand

In 2021, Taiwan encountered challenges in its tourism market as COVID-19 resulted in travel restrictions. This caused international arrivals to decline by 89.8%. In 2021, Vietnam was the first top source market for Taiwan, taking up 18% of the total market share, followed by Indonesia and Japan, with 10% and 7% of the total market share, respectively. Taiwan reopened its border to international travellers to incentivise international arrivals in July 2022, allowing business and leisure travellers to enter Taiwan, but quarantine is still required. As of YTD June 2022, there were 139,911 international arrivals, an 81.2% increase from the same period last year due to the government easing the border restriction.

Supply

*Include non-branded hotels

Source: HVS Research

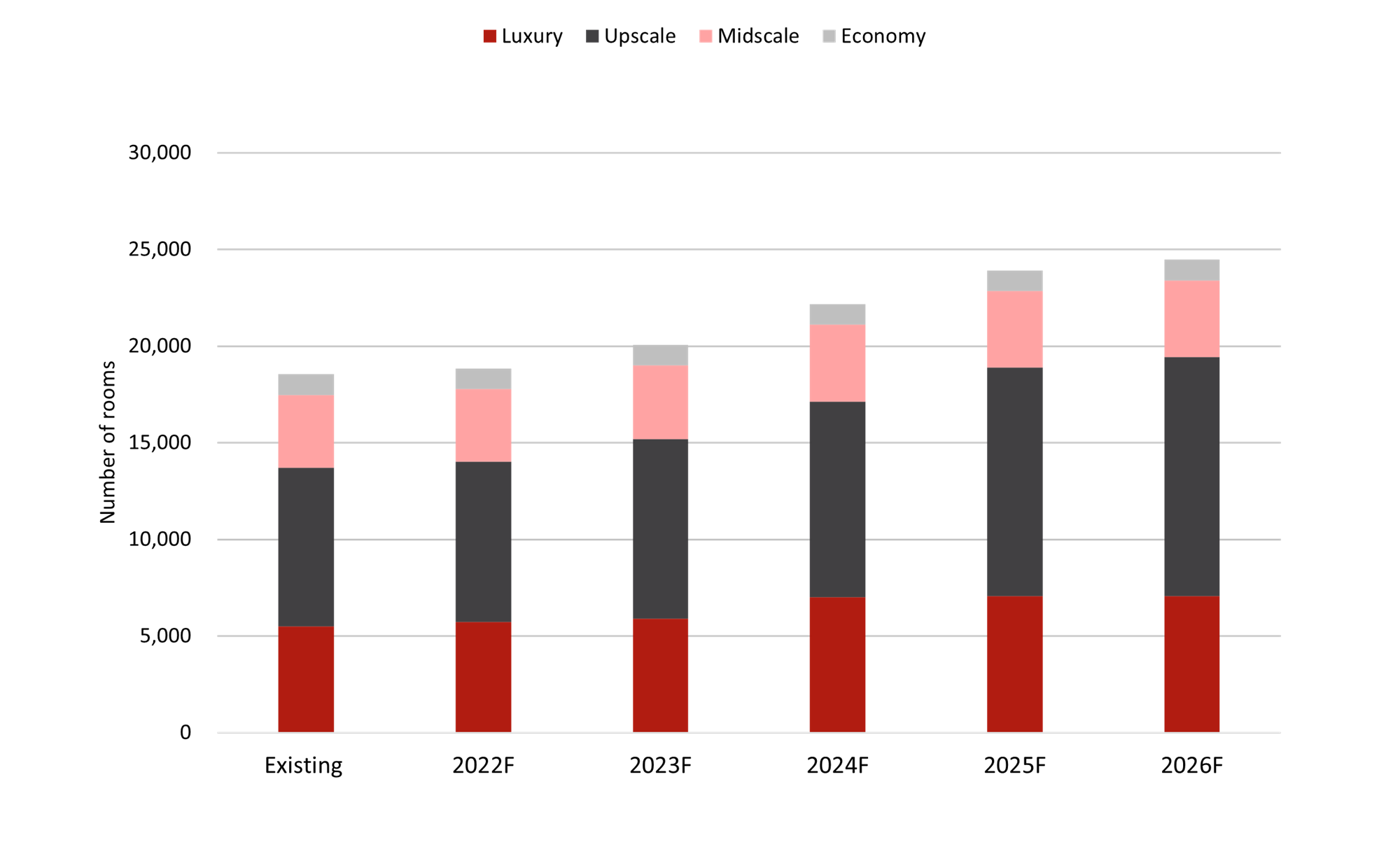

HVS has noted that going forward, there will be 27 additional hotels with approximately 5,930 keys in Taiwan by 2026; two properties with a total of approximately 304 rooms will open by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

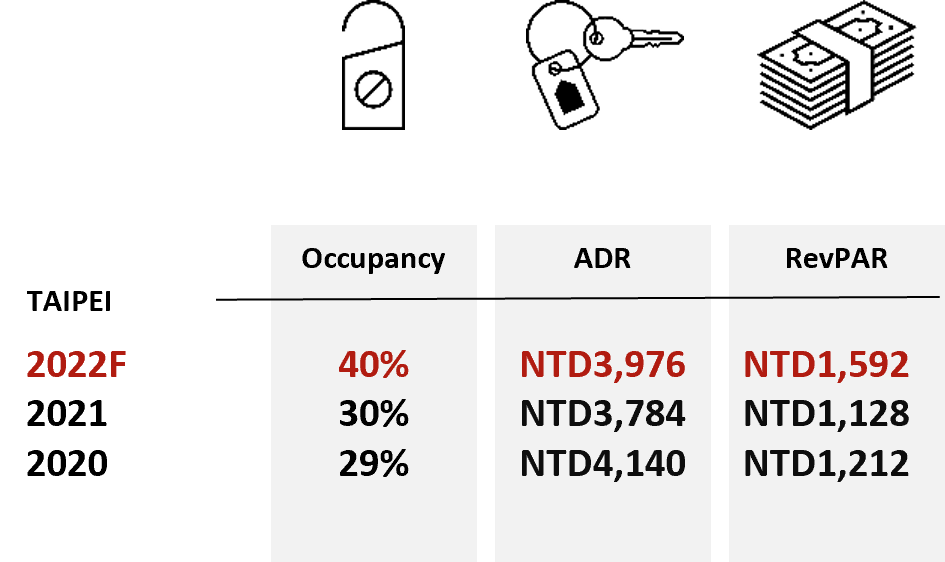

Hotel Performance

Source: HVS Research

As of YTD June 2022, hotel occupancy in Taipei has increased by 5.0 p.p y-o-y. Similarly, ADR increased by 7.3%, which has resulted in an increase in RevPAR by 25.0%. The performance can be attributed to the increase in global travel demand due to Taiwan’s gradual border reopening policy.

Transactions

Transaction value in Taiwan in YTD June 2022 remains relatively stagnant compared to the highest record of NTD36.8 billion in 2020. Investment activities were mainly transacted outside of Taipei, with only three transactions in Taipei in 2021 and none in YTD June 2022.

Source: HVS Research

Thailand

Key Points

- Tourism contributes 5.8% to GDP in 2021, down from 20.3% in 2019

- 2.9% Real GDP growth expected in 2022

- 428 thousand international tourist arrivals recorded in 2021

Highlights

COVID-19 Cases

- Total Cases: 4,522,915

- Active Cases: 23,026

Infrastructure Projects

- THB267 billion high-speed rails from Bangkok to Pattaya expected completion by 2023

- THB94 billion 109km highway from Nakhon Pathom to Cha-am district in Phetchaburi expected completion by 2025

- THB61 billion Suvarnabhumi airport expansion is expected completion by 2030

Notable Upcoming Hotel Openings in Bangkok and Phuket (2022)

Top 3 Largest Inventory

- Chatrium Grand Bangkok, 582 keys

- Wyndham La Vita Phuket, 516 keys

- Wyndham Phuket, 488 keys

Notable Transactions

- 131-key dusitD2 Chiang Mai was acquired at THB435 million, (THB3.3m/key) in Jan 2022

- 180-key Mercure Bangkok Makkasan was acquired at THB575 million, (THB3.2m/key) in Dec 2021

Demand

In YTD May 2022, due to the reopening of international borders, total arrivals increased significantly by 5,042% y-o-y with 2.1 million visitors compared to merely 40,447 visitors YTD May 2021. India became the top source market for Thailand with a total market share of 11.3%, followed by Malaysia and Singapore as second and third source markets accounting for 6.1% and 5.9% respectively. As Thailand’s government offers soft loans of THB5 billion to local hotels to reopen, the tourism market anticipates an increase in both international demand and supply of hotel rooms.

Supply

*Include non-branded hotels

Source: HVS Research

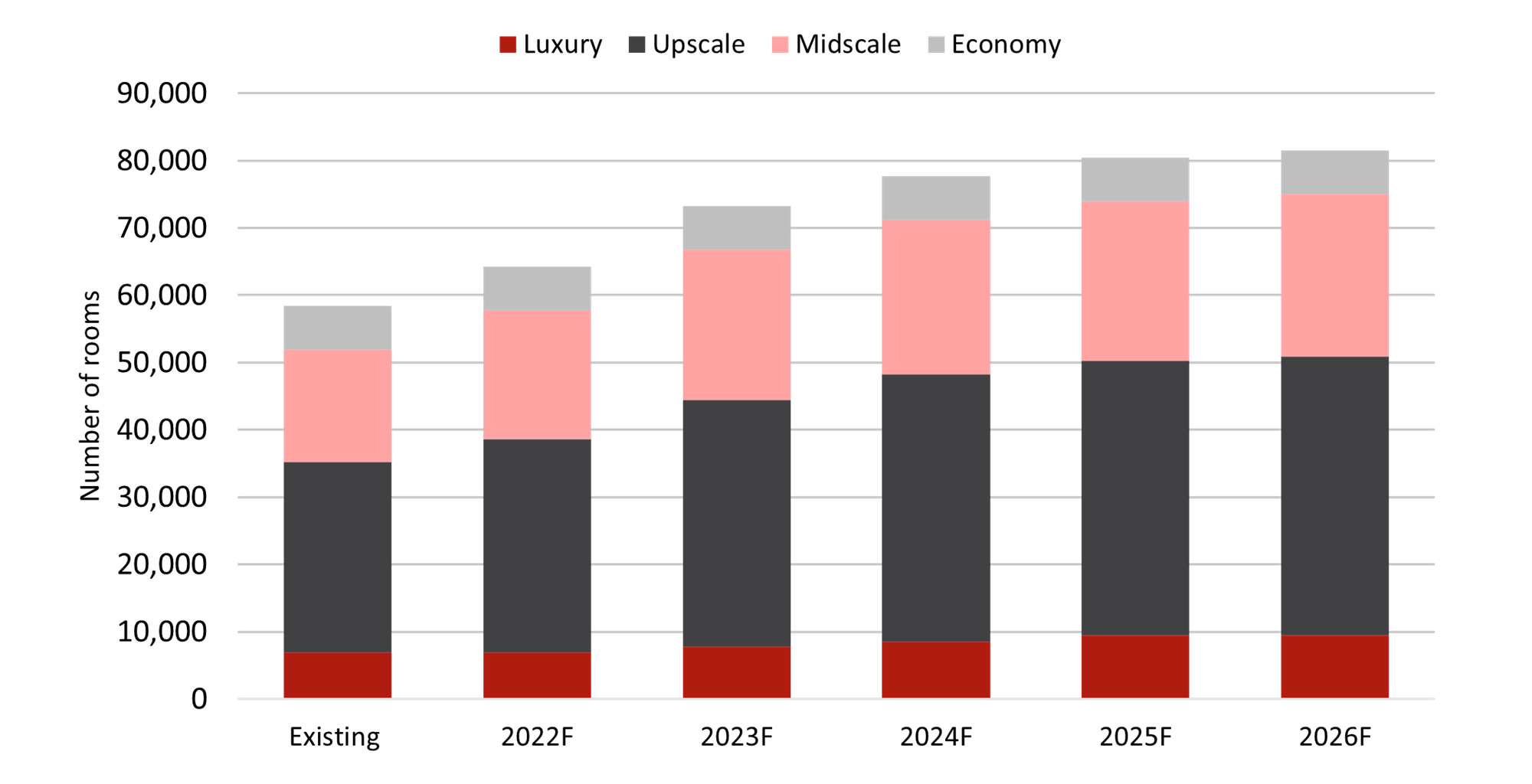

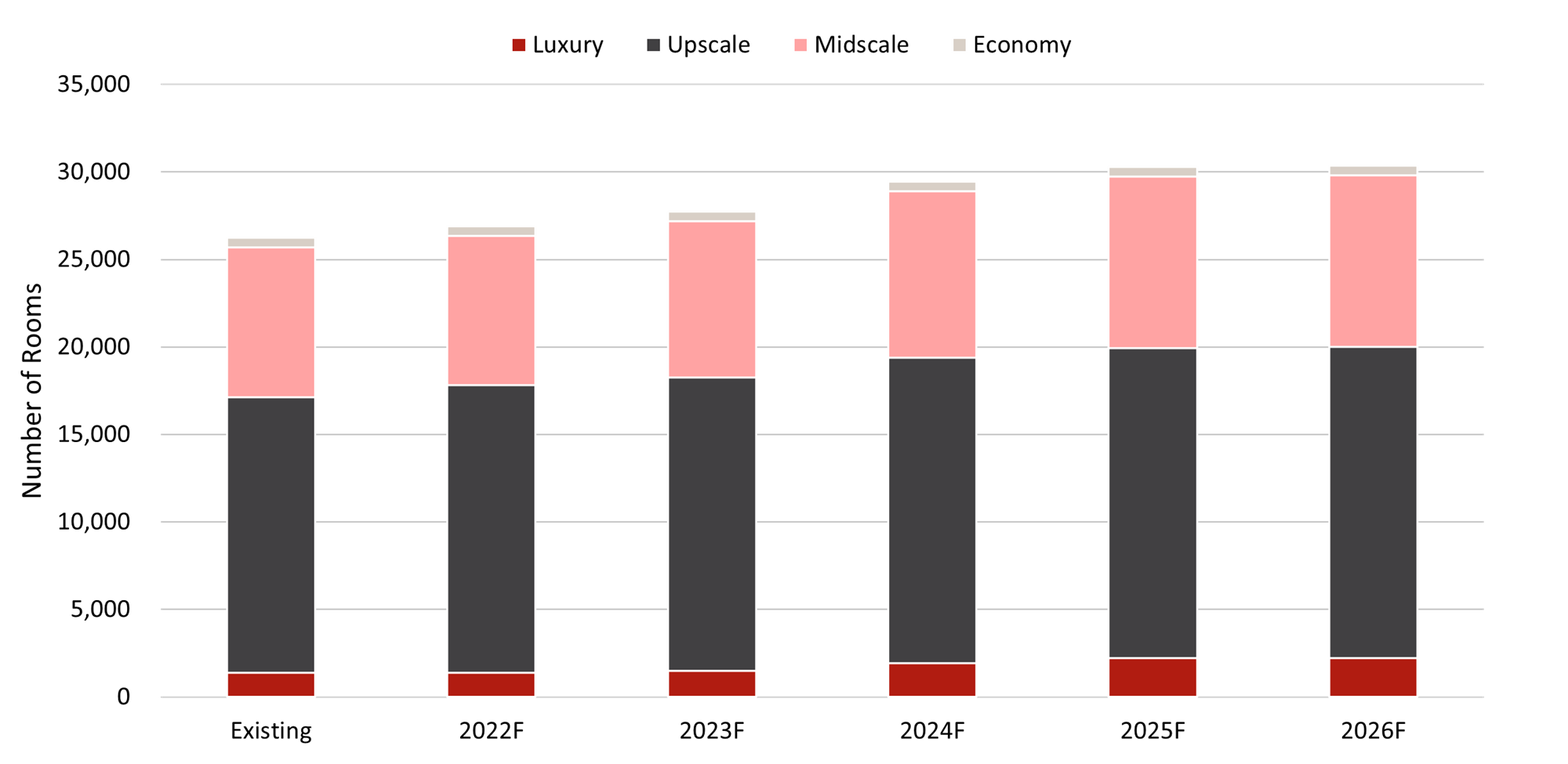

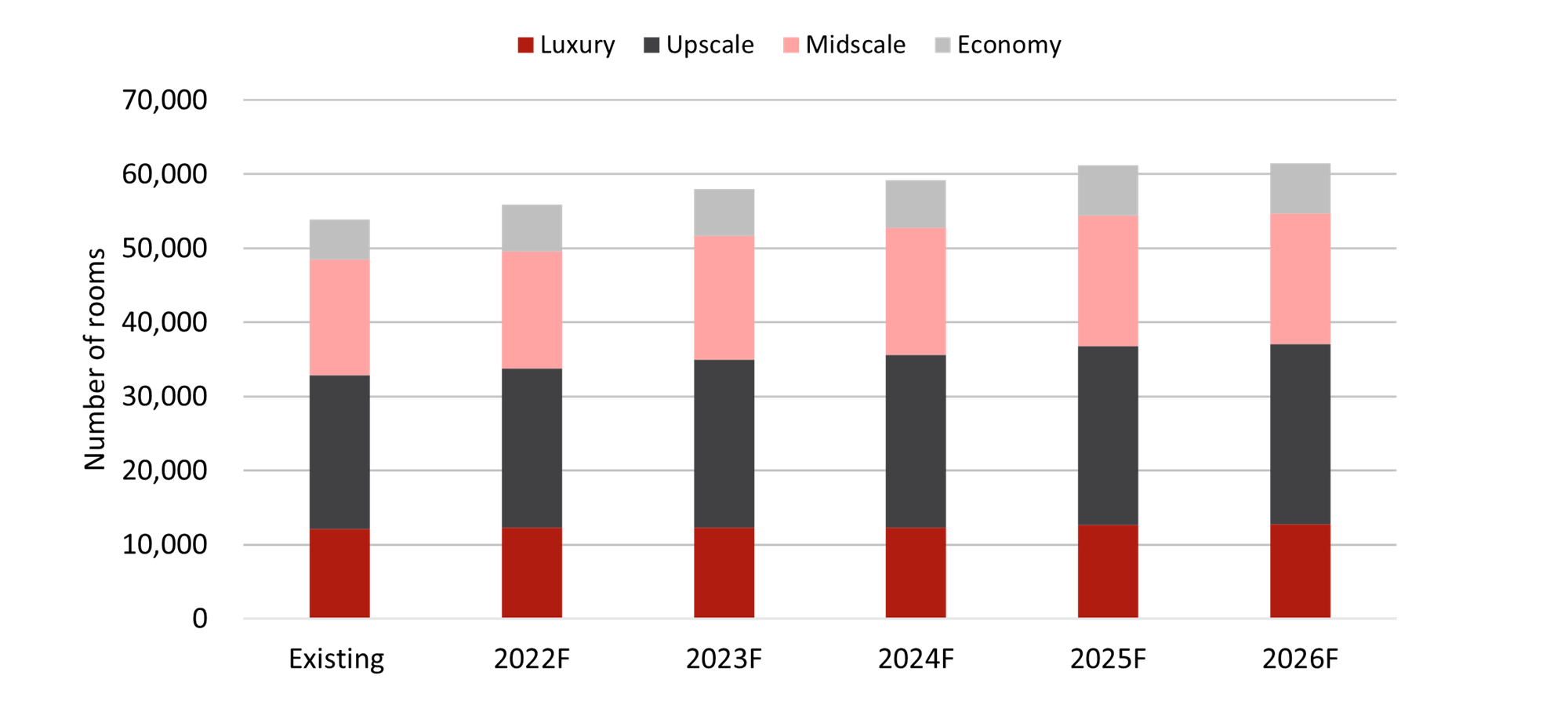

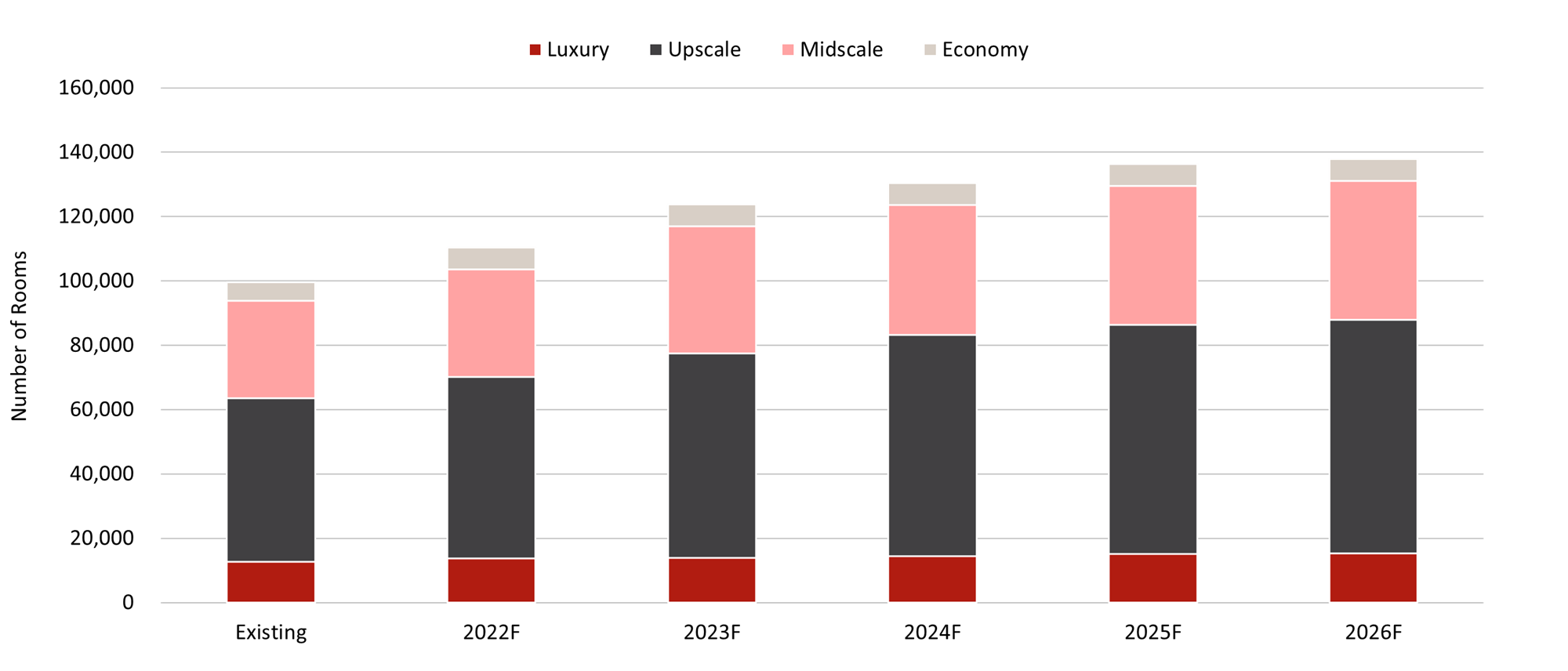

HVS has noted that going forward, there will be 151 additional hotels with approximately 38,289 keys in Thailand by 2026; 43 properties with a total of approximately 10,769 rooms will open by the end of 2022

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

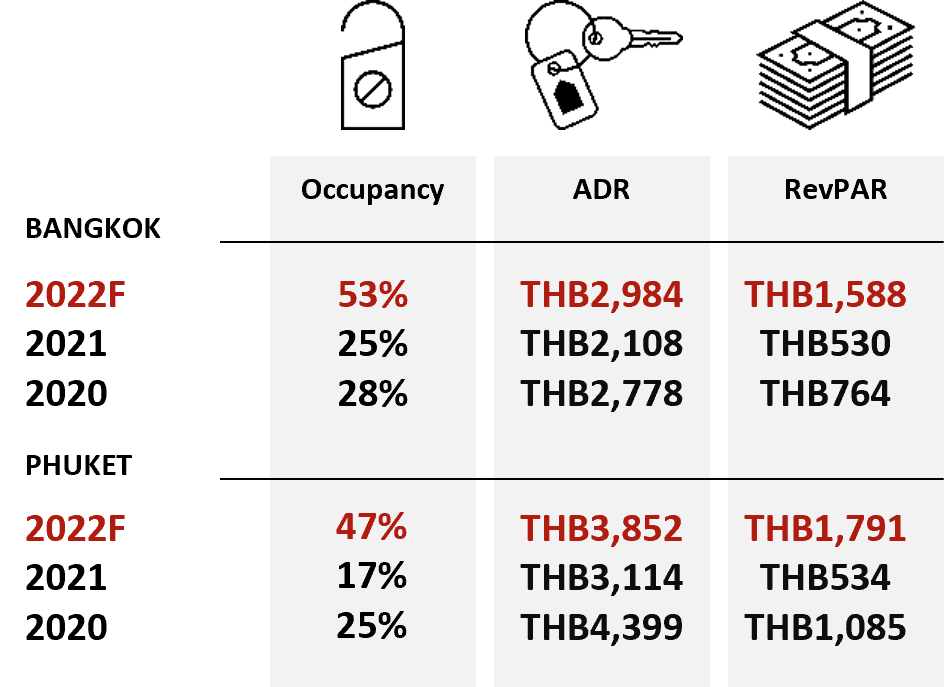

Hotel Performance

Source: HVS Research

In YTD June 2022, both Bangkok and Phuket hotels recorded a y-o-y increase in occupancy rates by 22.5 p.p. and 30.7 p.p, respectively. ADR in both cities also increased significantly by 26.8% and 54.0%, respectively. Therefore, the RevPAR has increased 159.5% and 568.9% for Bangkok and Phuket respectively.

Transactions

There were a total of 67 transactions recorded from 2017 to YTD June 2022. In the first six months of 2022, more than THB7 billion worth of investment activity was recorded, an upward trend from YTD June 2019 and 2020. 2021 recorded the highest transaction volume in five years which include notable transactions such as the Minor Hotel Portfolio and Erawan Hotel Portfolio sale.

Source: HVS Research

Vietnam

Key Points

- Tourism contributes 2.6% to GDP in 2021, down from 7.0% in 2019

- 8.2% Real GDP growth expected in 2022

- 3,500 international tourist arrivals recorded in 2021

Highlights

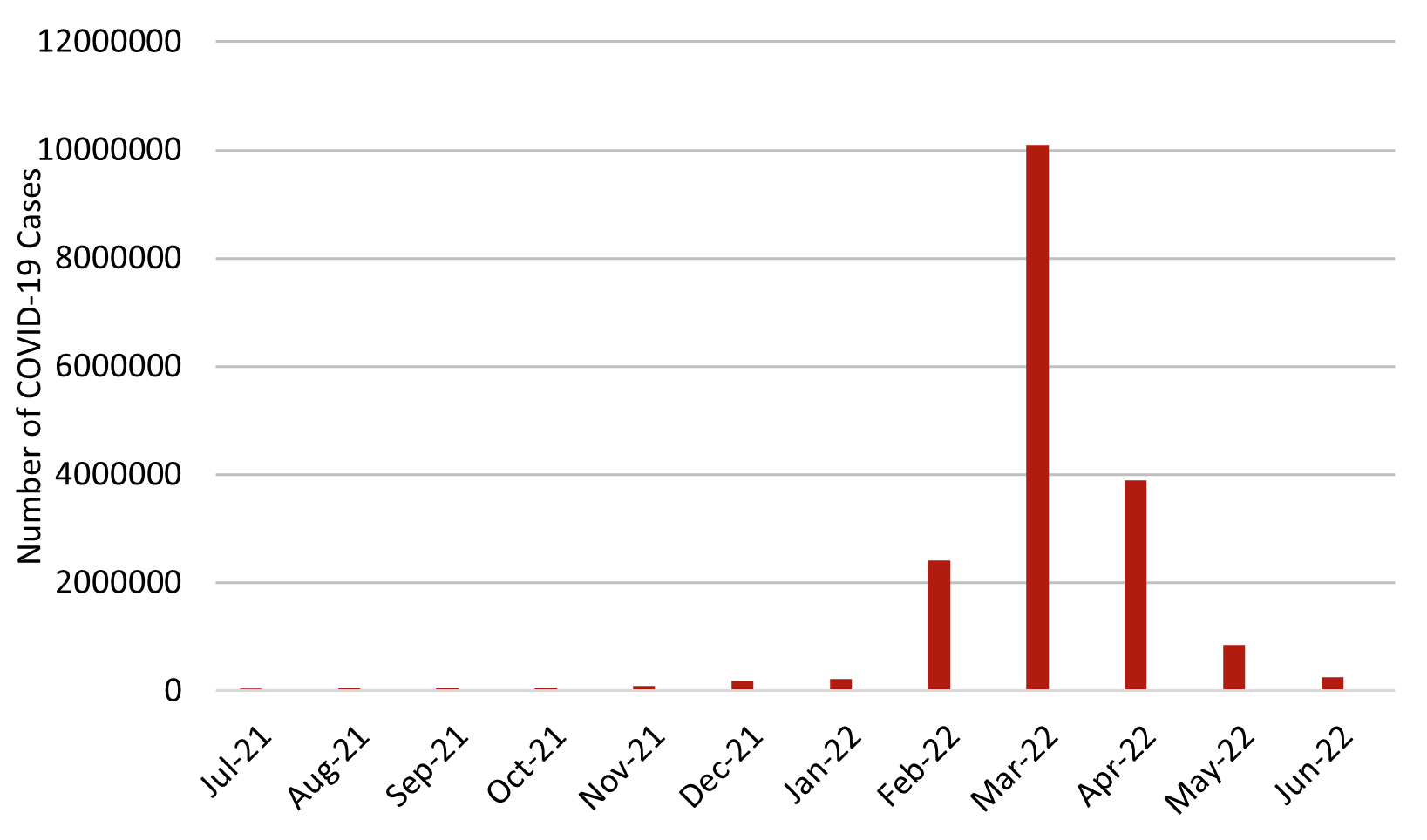

COVID-19 Cases

- Total Cases: 10,746,470

- Active Cases: 1,023,702

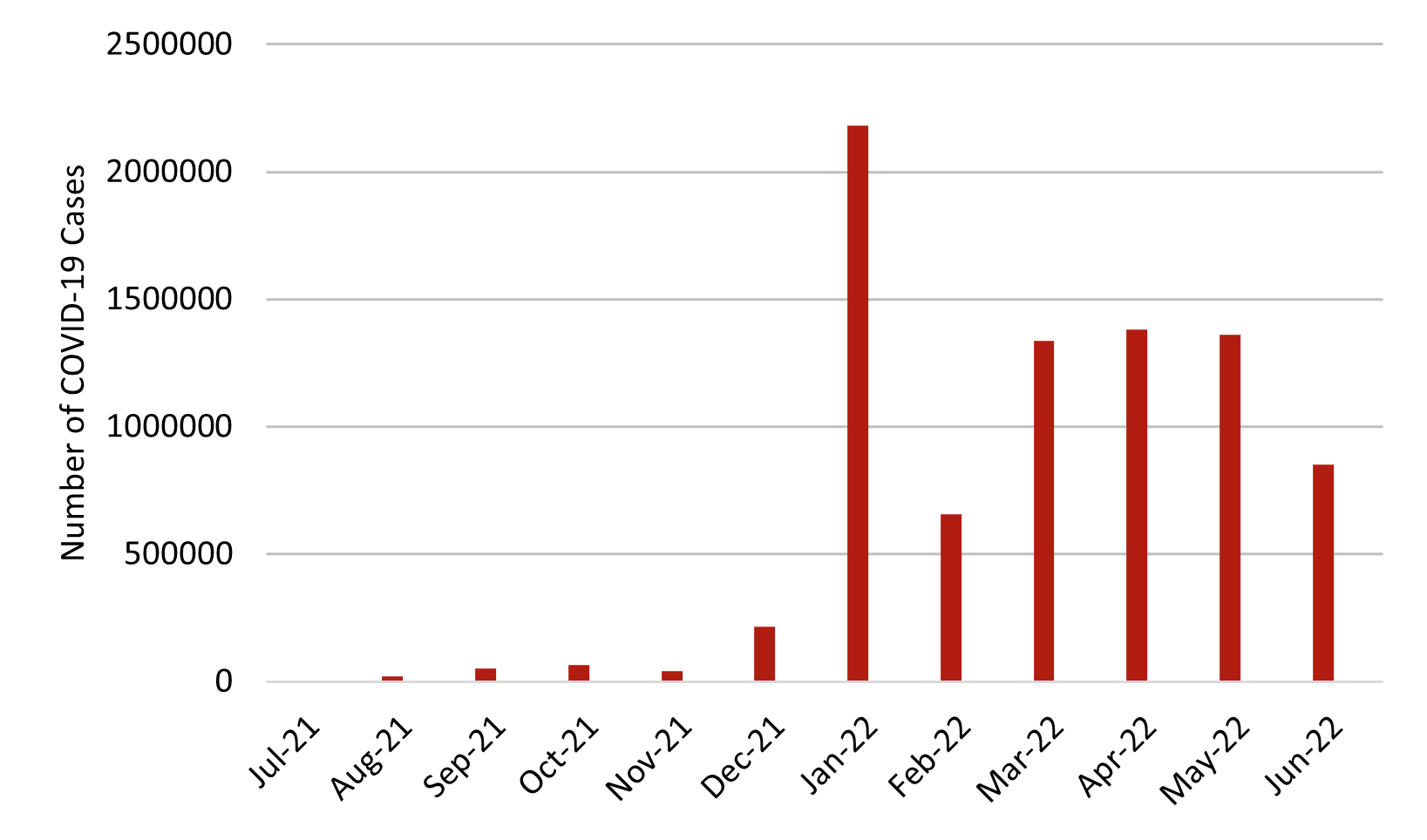

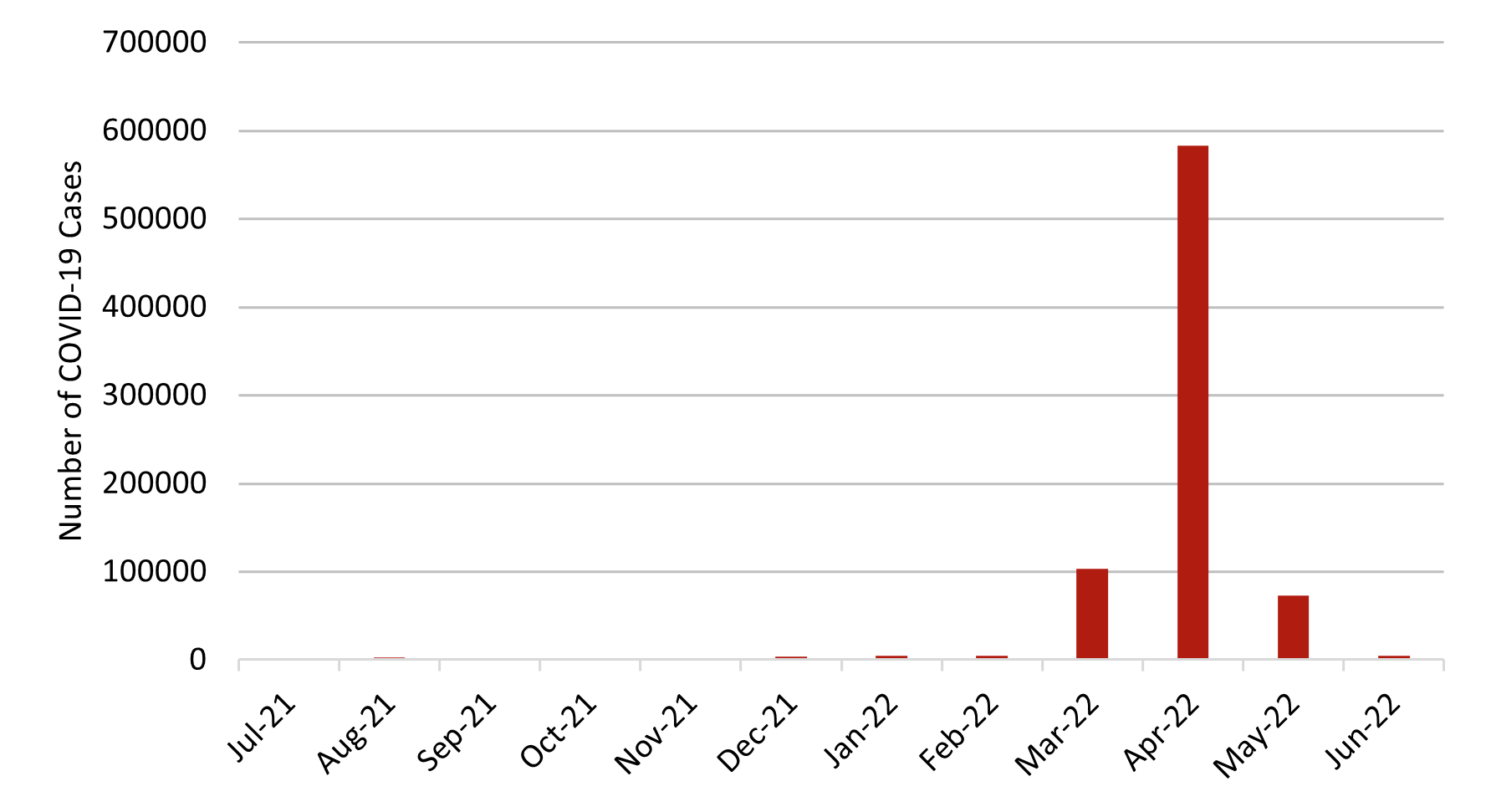

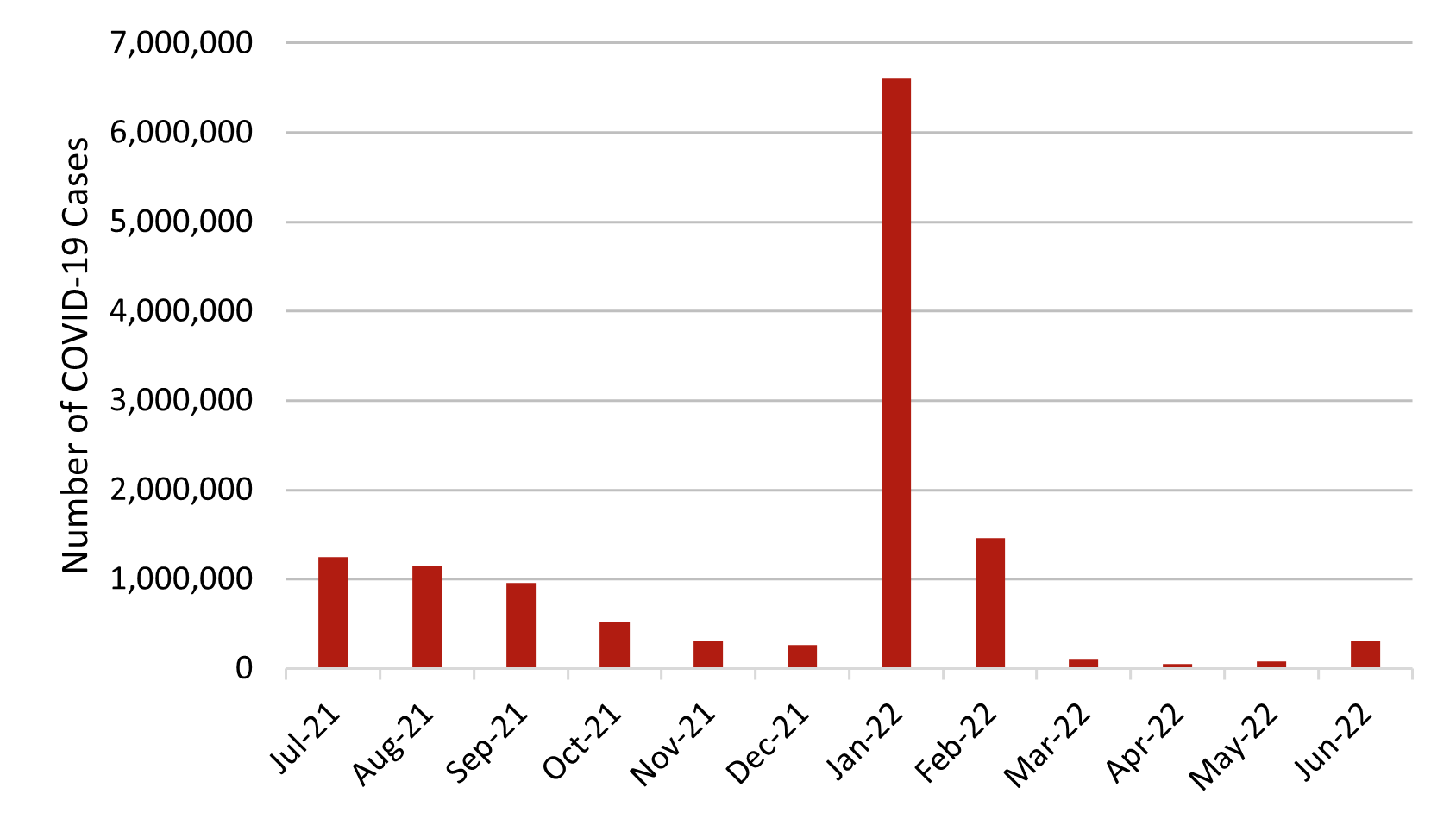

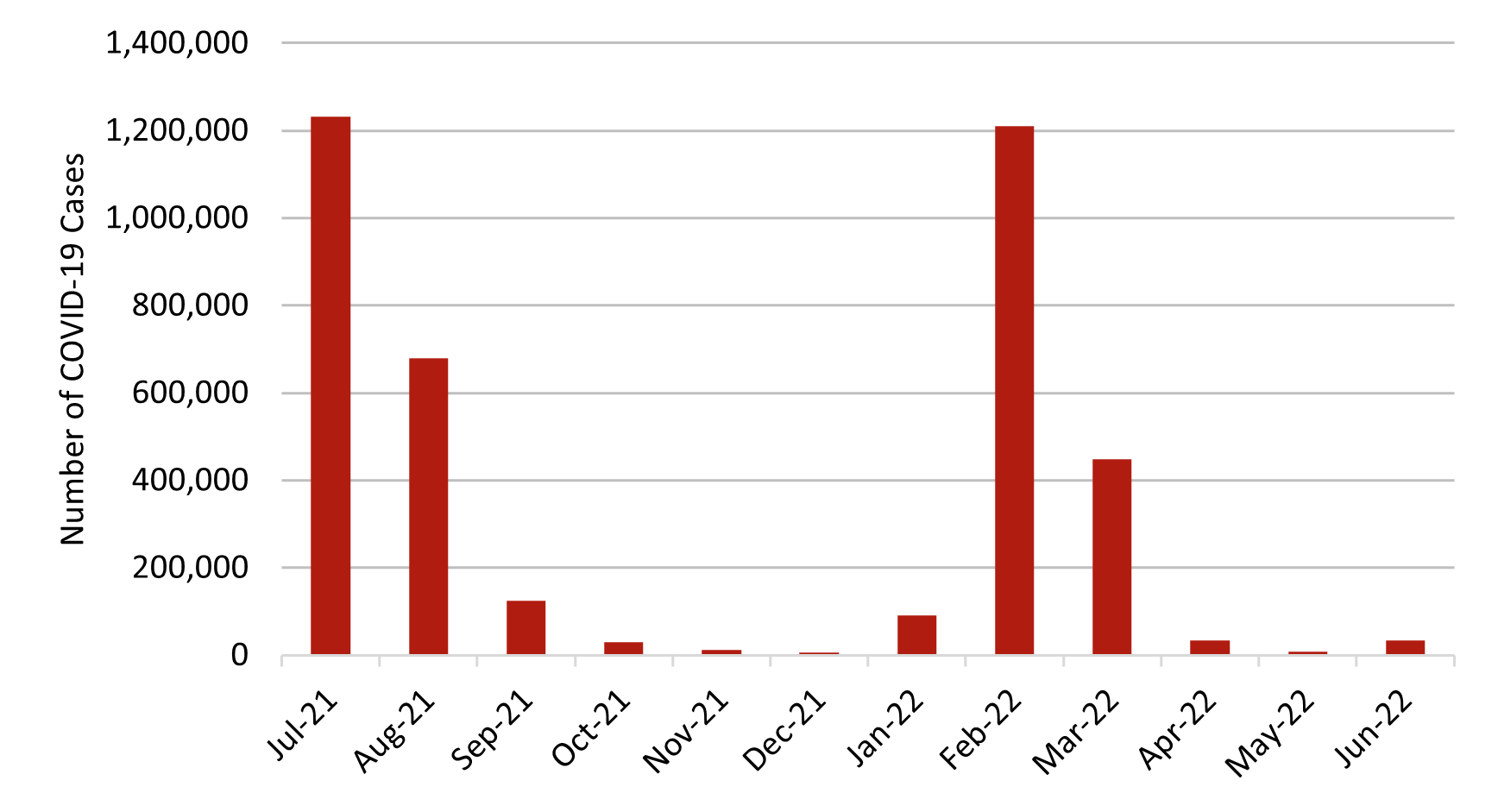

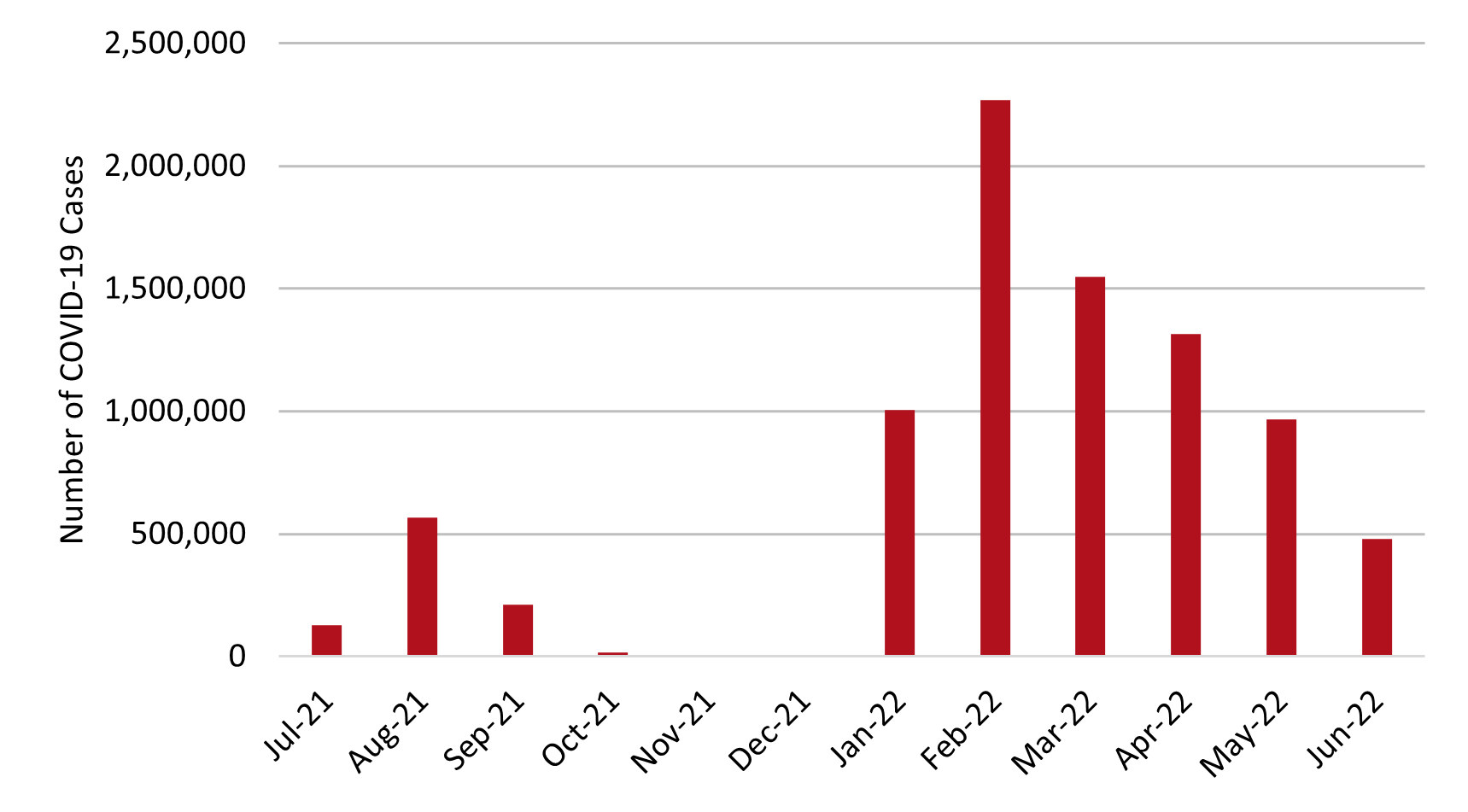

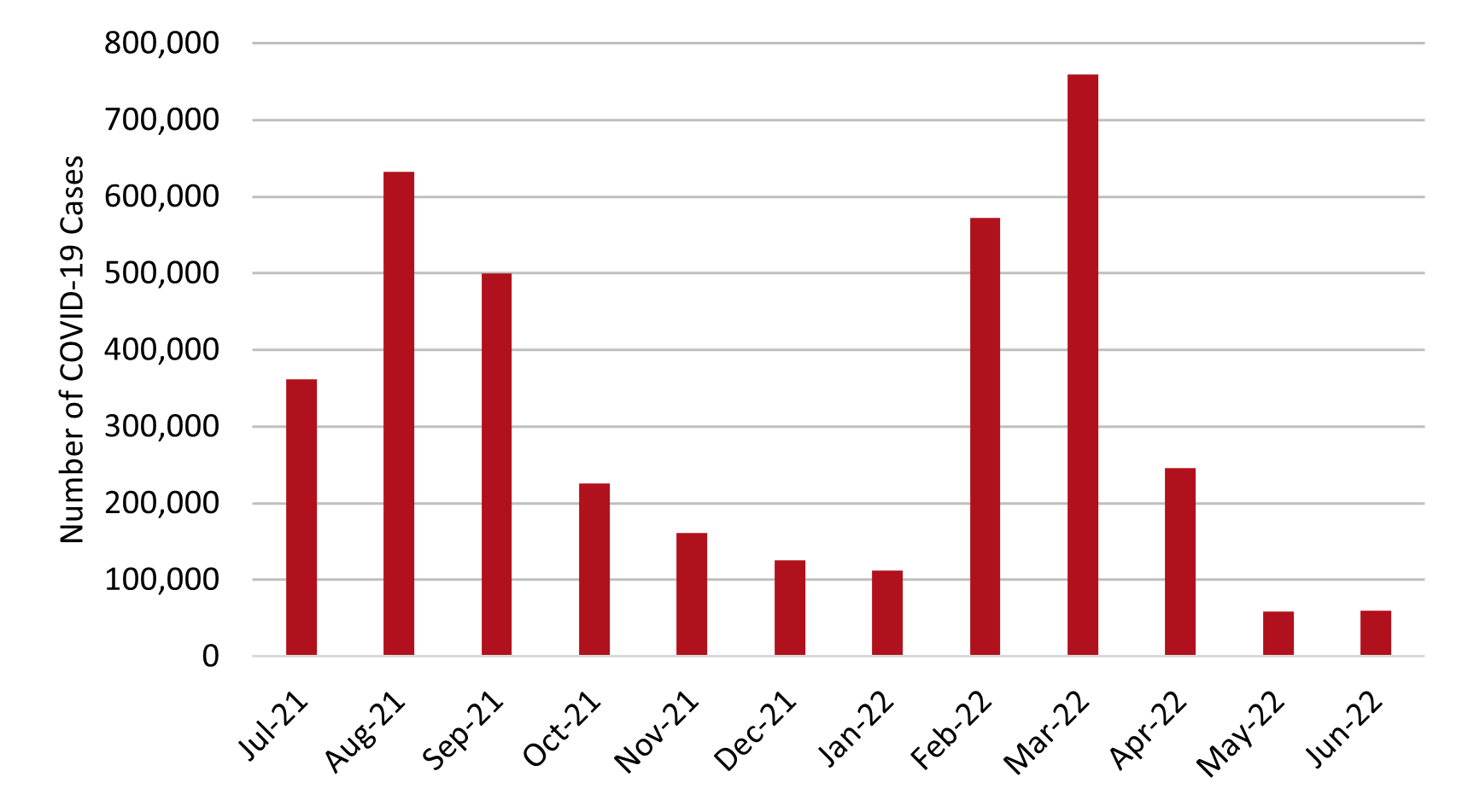

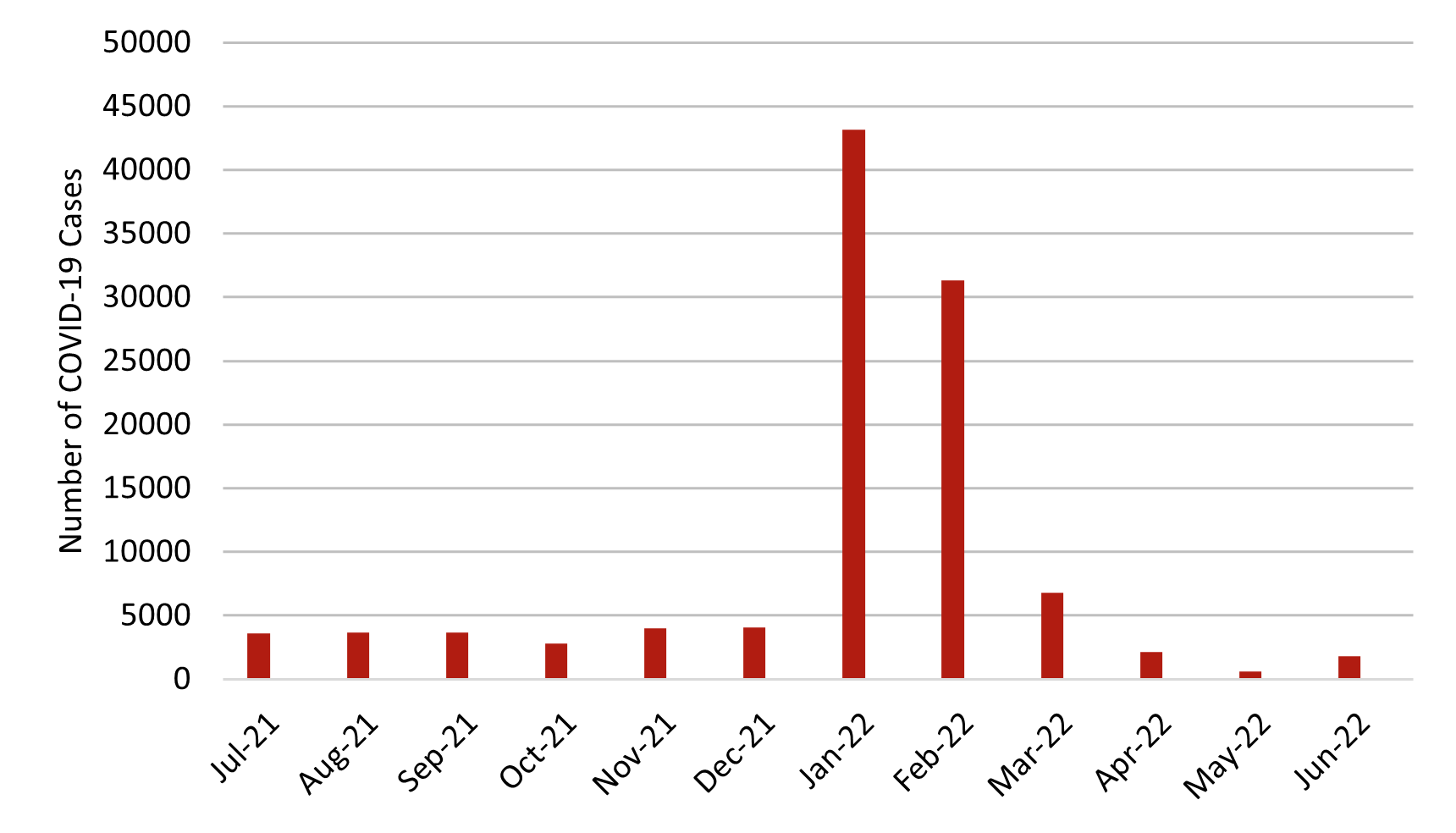

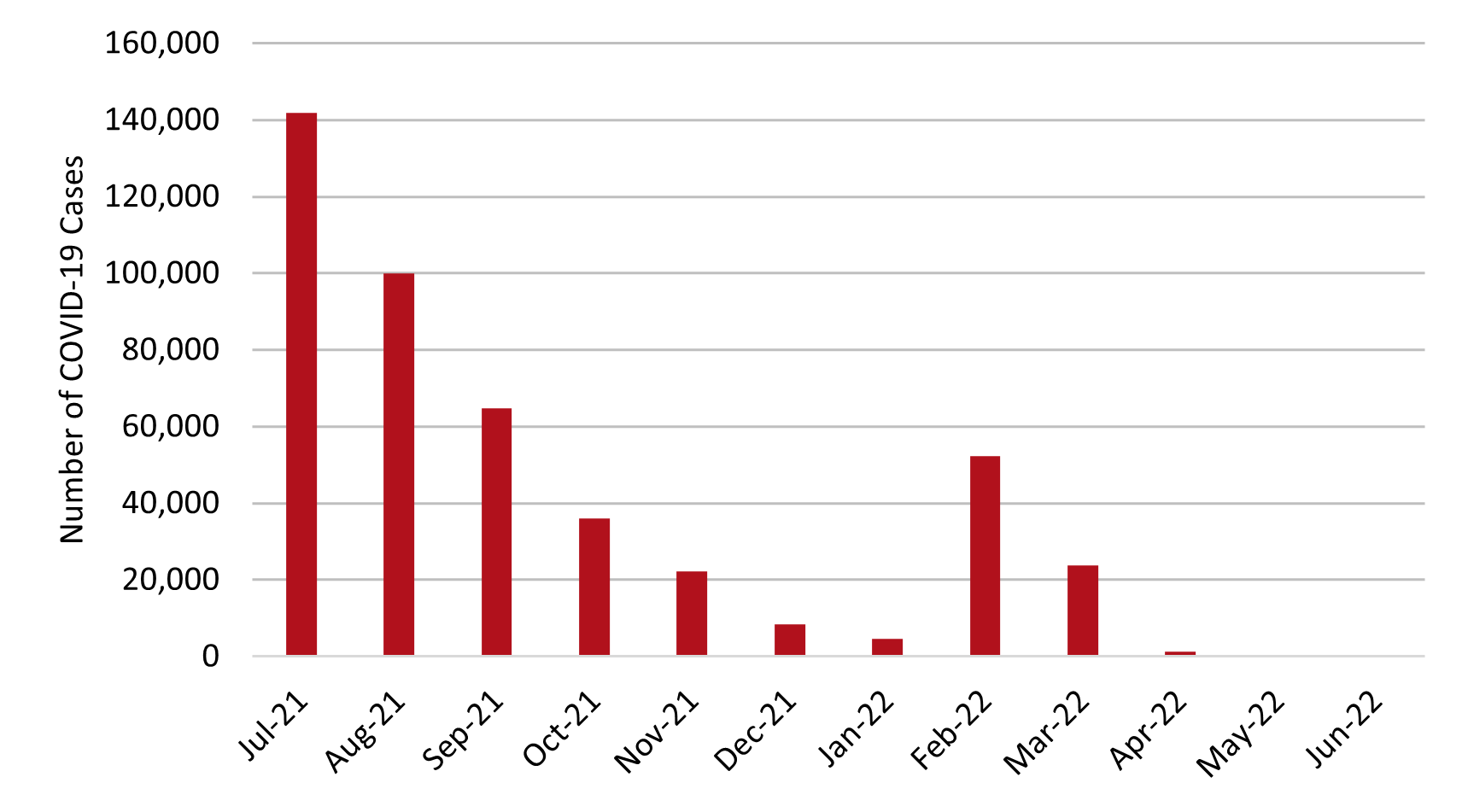

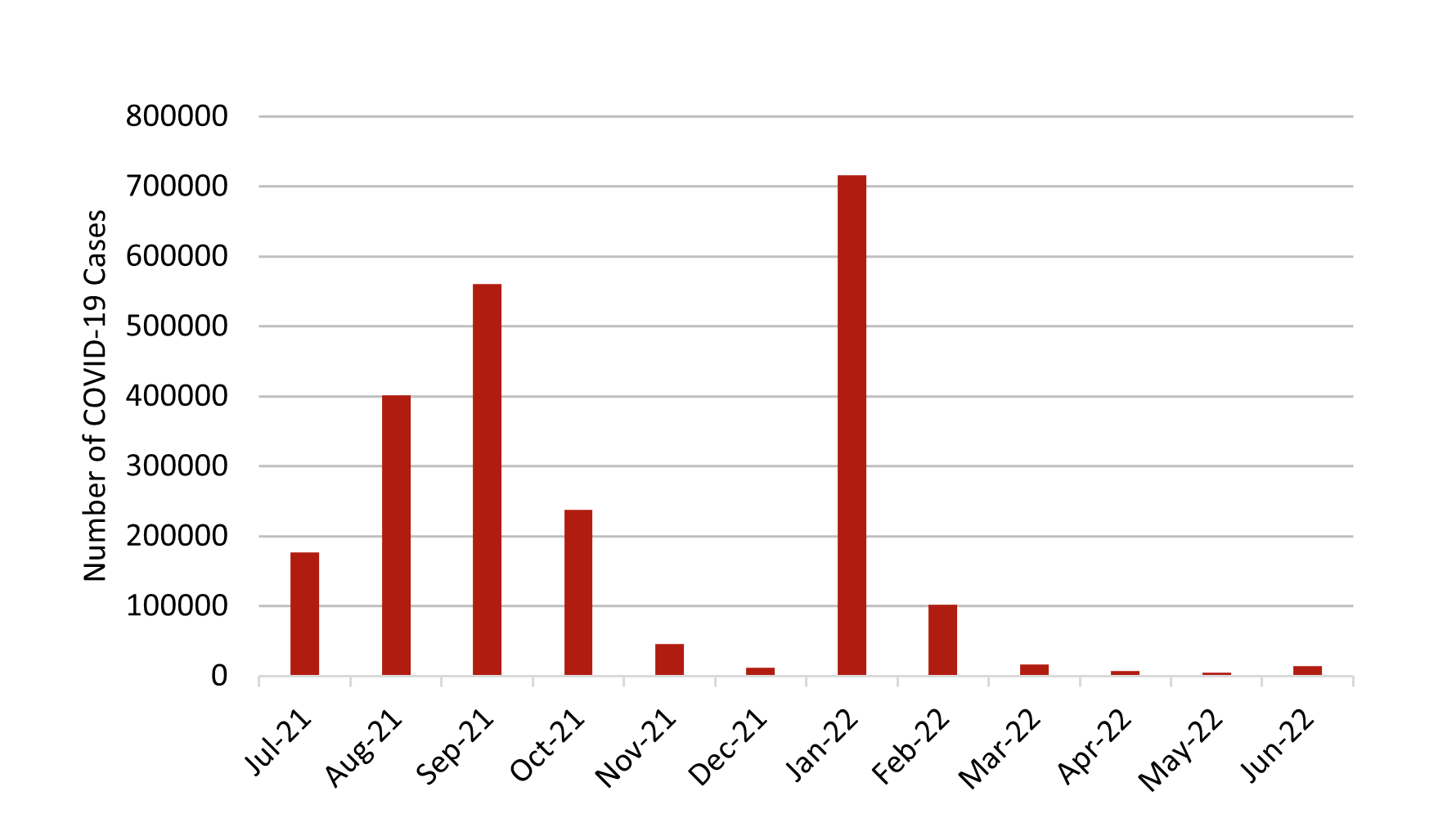

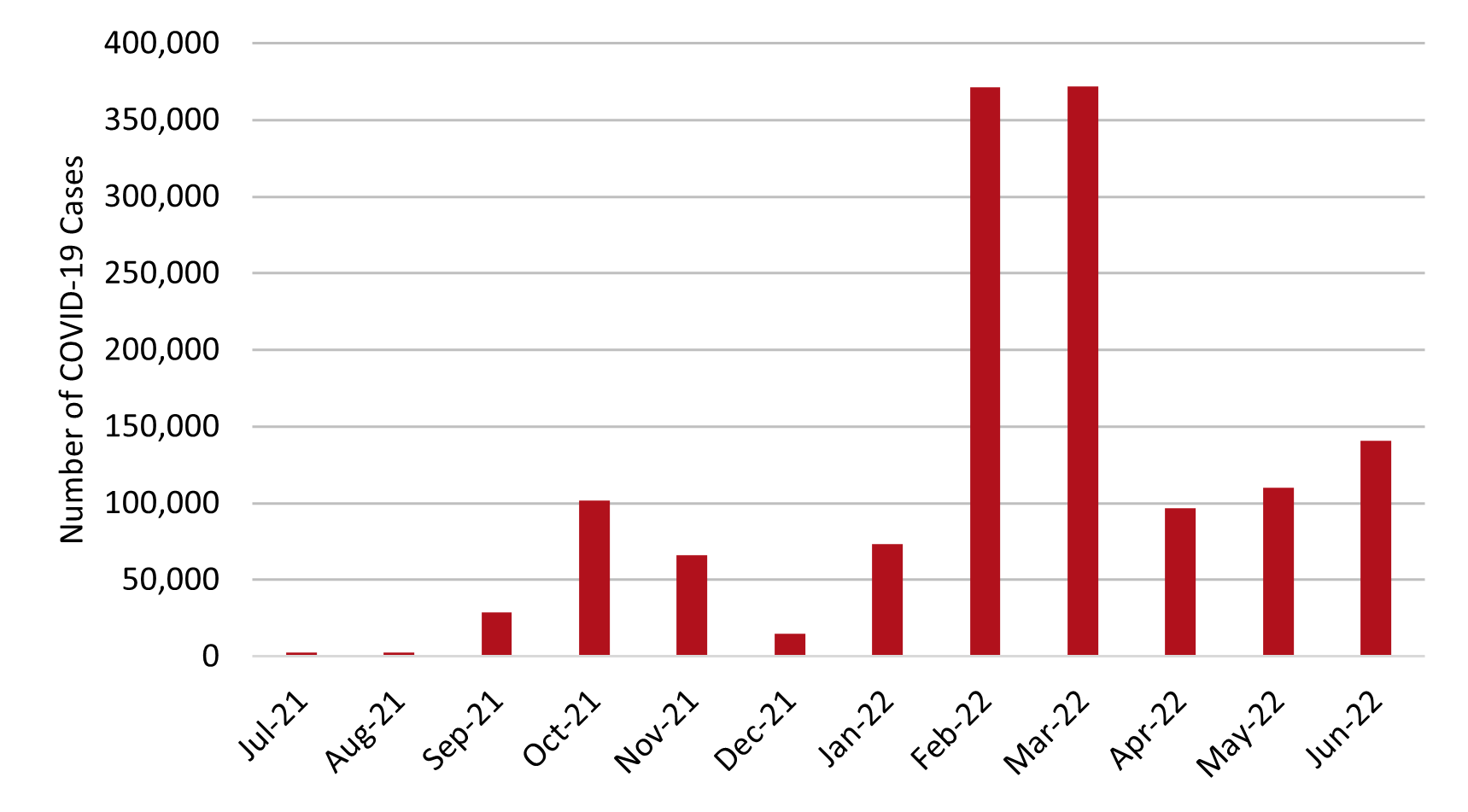

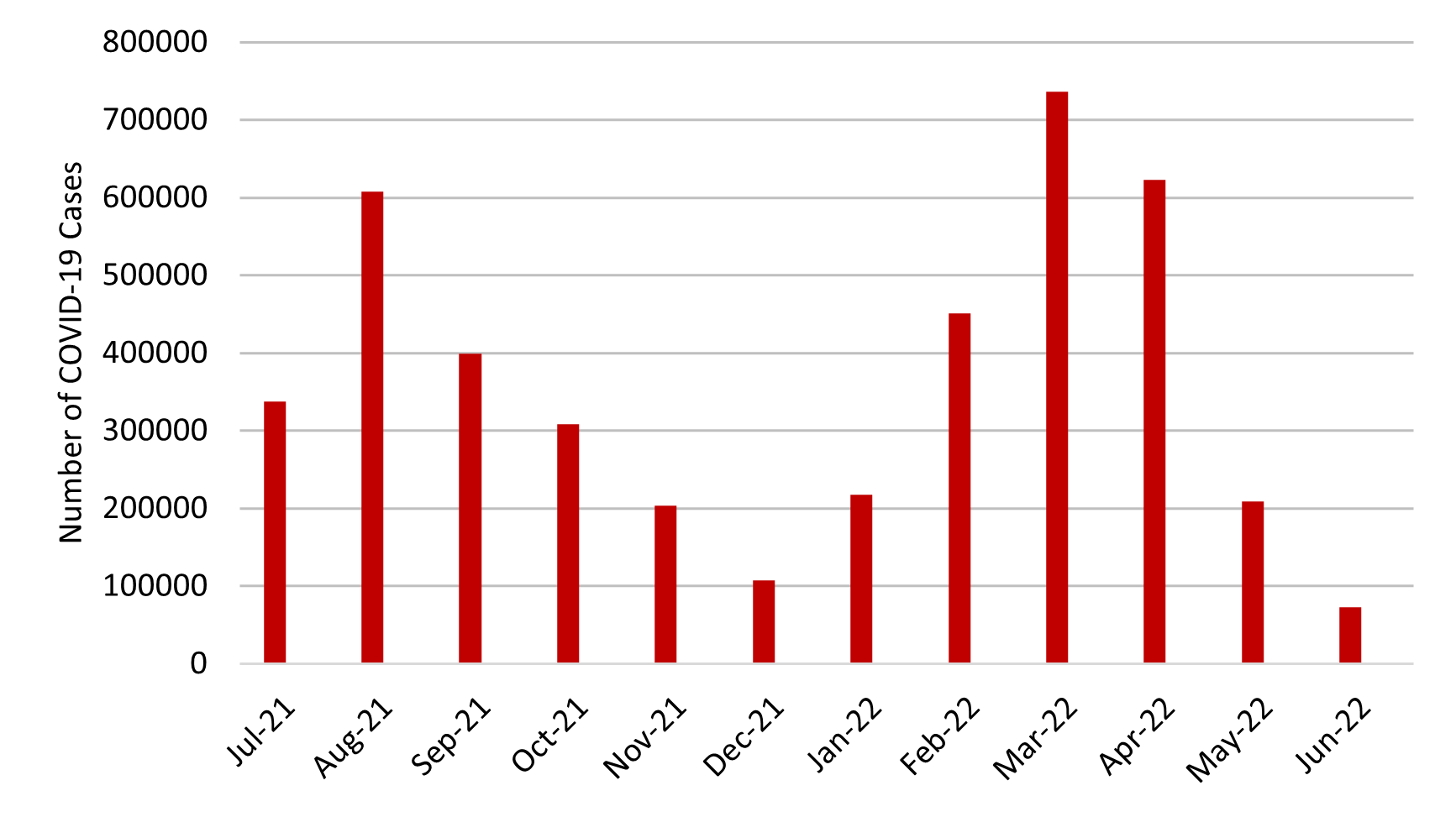

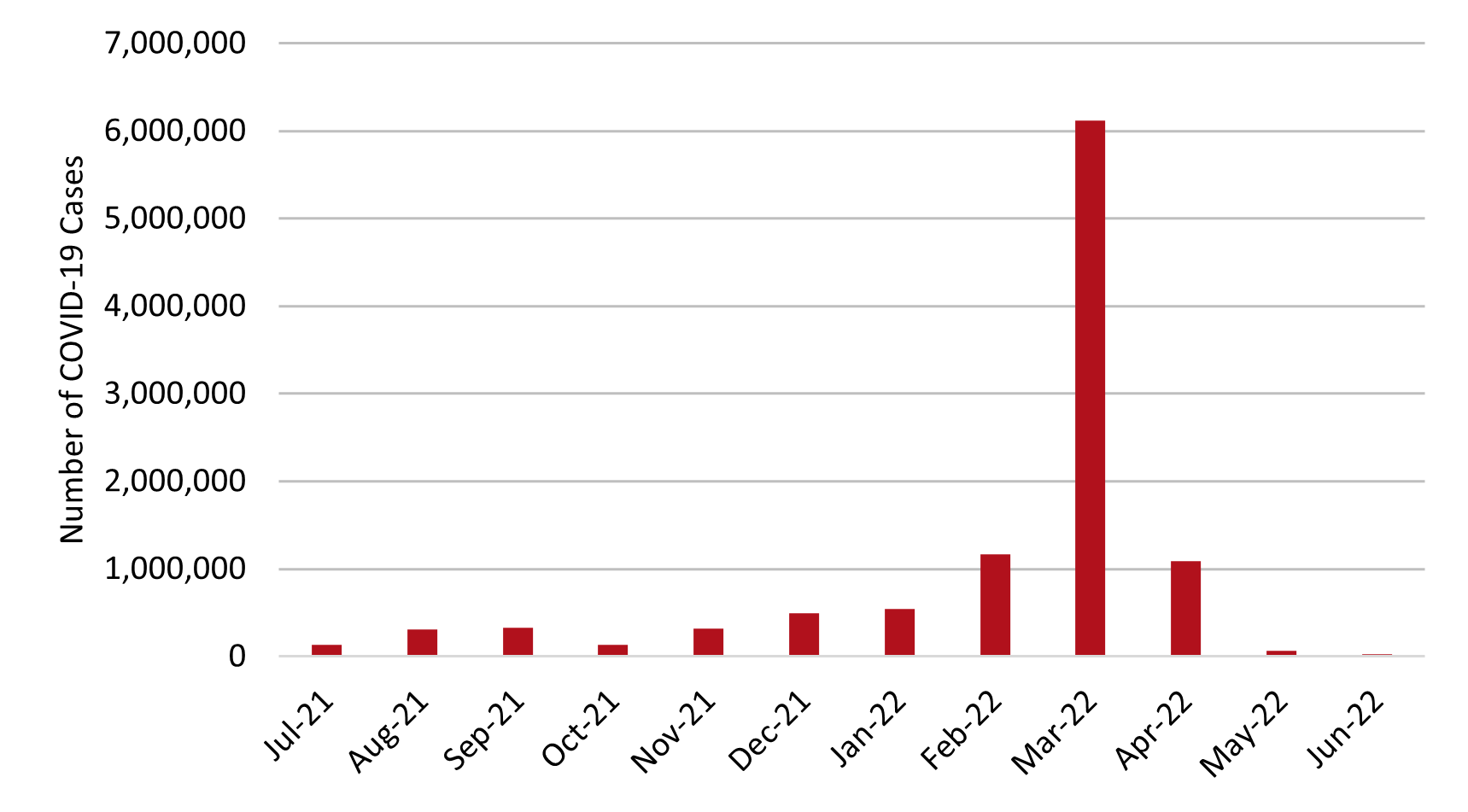

Number of COVID-19 Cases (July 2021 – June 2022)

Source: Our World In Data; data as of 30th June 2022

Infrastructure Projects

- Opening of Metro Lines 1 and 2 in HCMC by 2023 and 2026 respectively

- Constructing the North-South Expressway connecting the country by 2030

- VND365 trillion aviation expansion plan to build new airports and expand the existing airport by 2030, including the new Long Thanh Airport in HCMC

Notable Upcoming Hotel Openings in Hanoi and HCMC (2022)

Top 3 Largest Inventory

- Shama West Hanoi, 240 keys

- dusitD2 Hanoi, 207 keys

- PARKROYAL Hanoi, 126 keys

Notable Transactions

- 70% interest in 90-key Somerset West Lake (Hanoi) acquired at VND0.23 trillion, reflecting hotel value at VND0.33 trillion (VND3.6b/key) in October 2019

- 75% interest in 318-key Intercontinental Hanoi West Lake Hotel acquired at VND2.91 trillion, reflecting hotel value at VND3.89 trillion (VND12.2b/key) in May 2019

Demand

The international tourist arrivals recorded in YTD June 2022 was 413,000 for Vietnam, a massive increase when compared to the full year of 2021 figure. Vietnam opened its international border in March 2022 and gradually eased most of its COVID-19 restrictions, such as suspending medical declarations and COVID-19 testing requirements for foreign arrivals. Vietnam Tourism Advisory Board is currently planning to extend the visa exemption to visitors from countries like the US, India, and Australia to diversify and reduce dependence on particular markets.

Supply

*Include non-branded hotel

Source: HVS Research

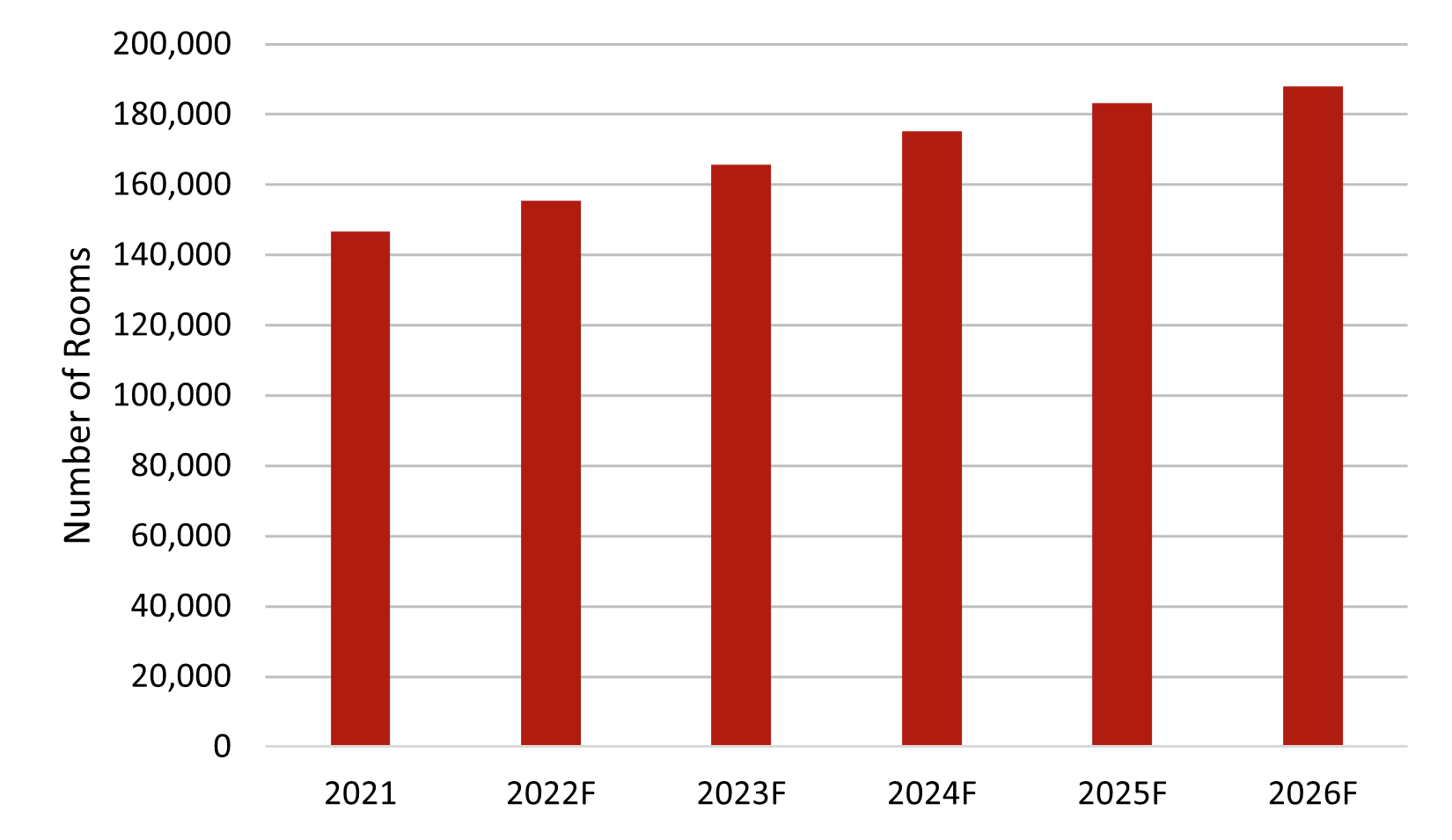

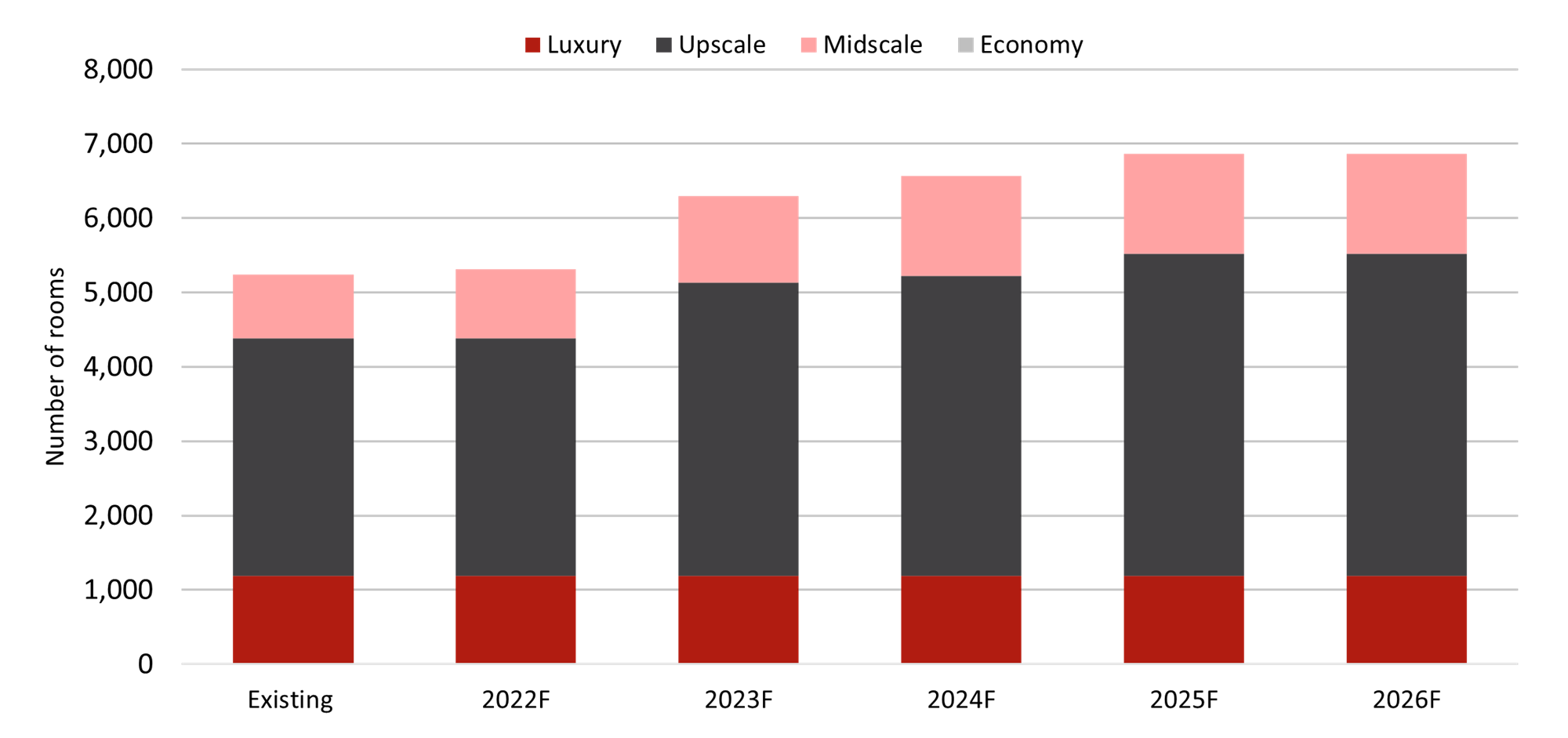

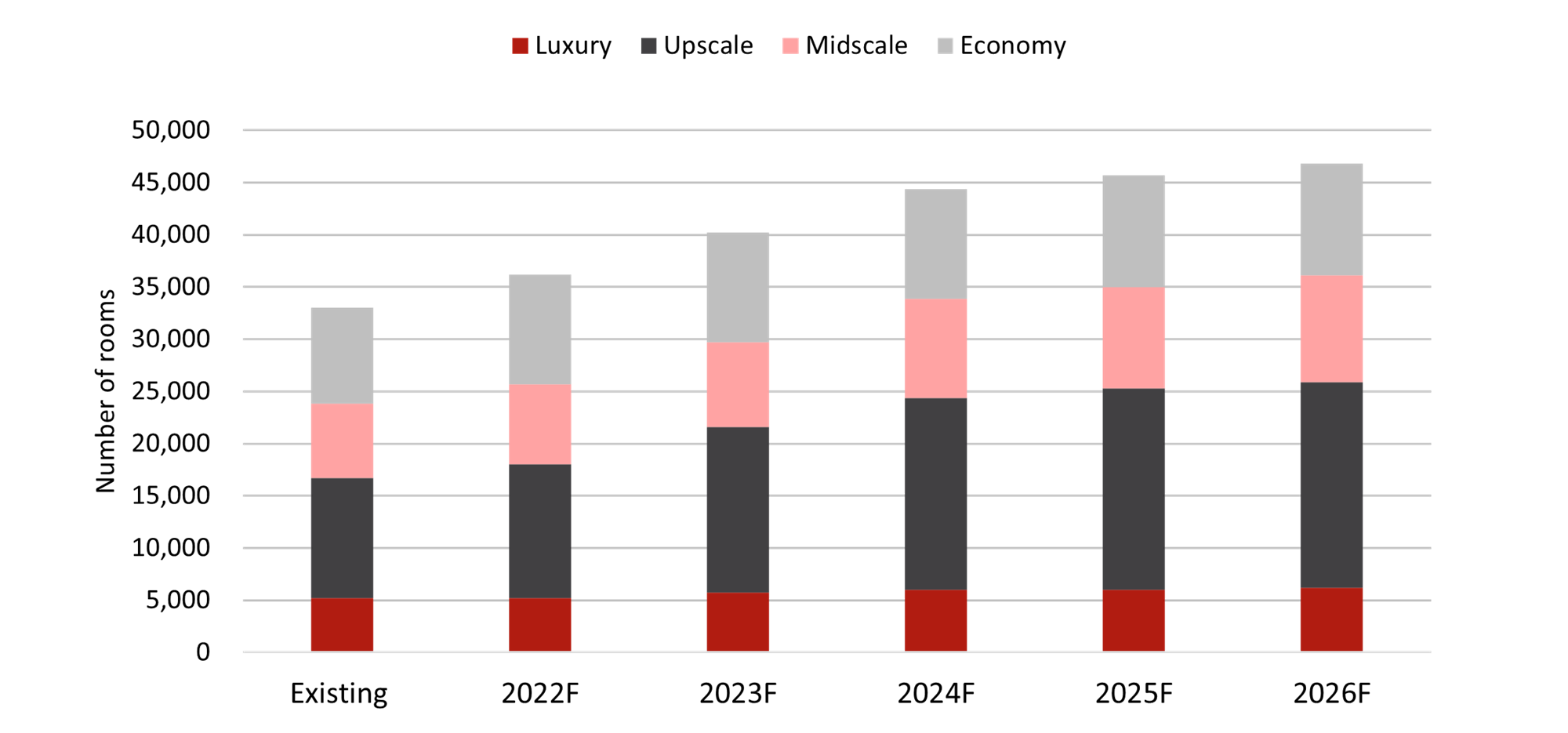

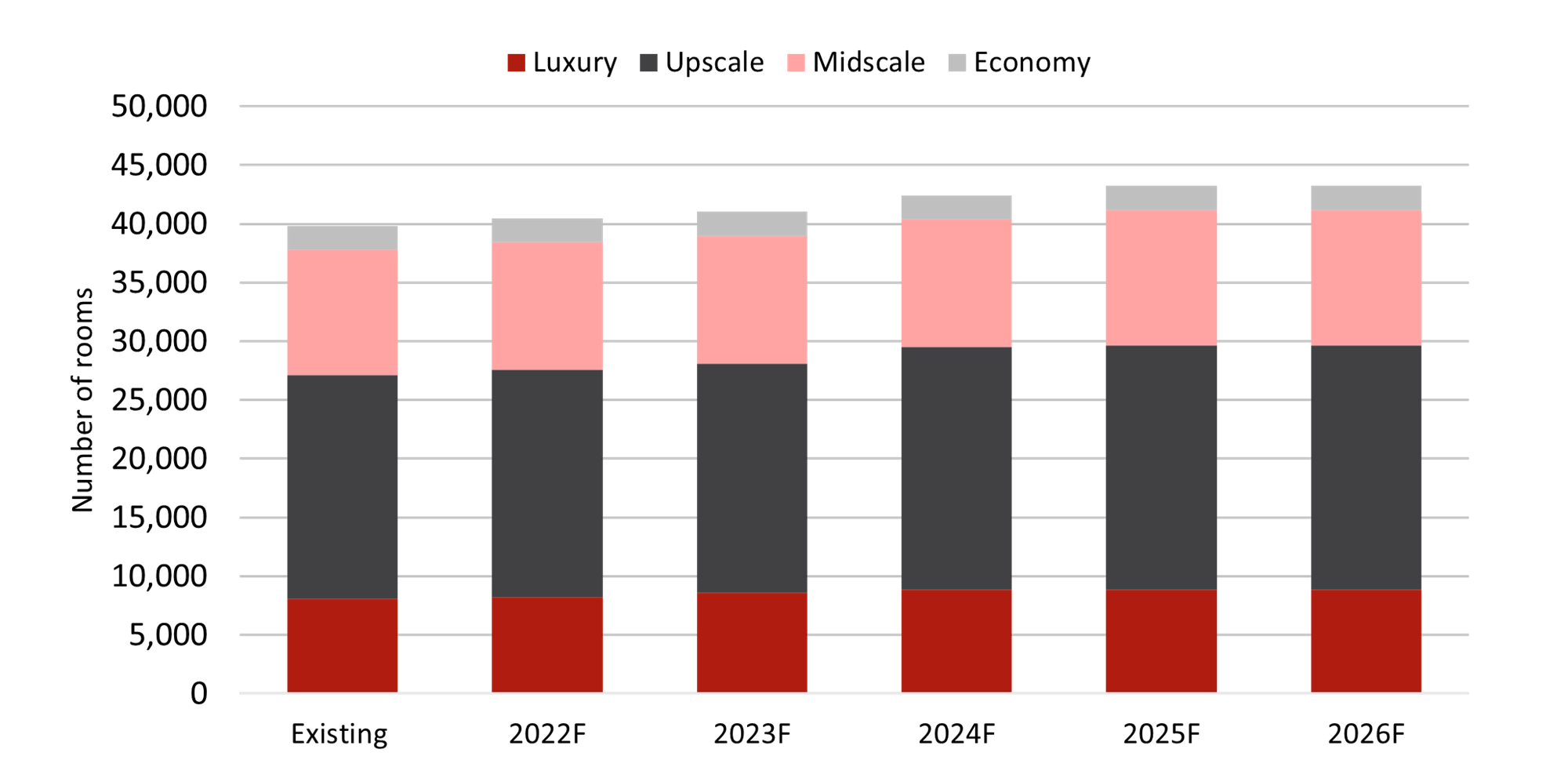

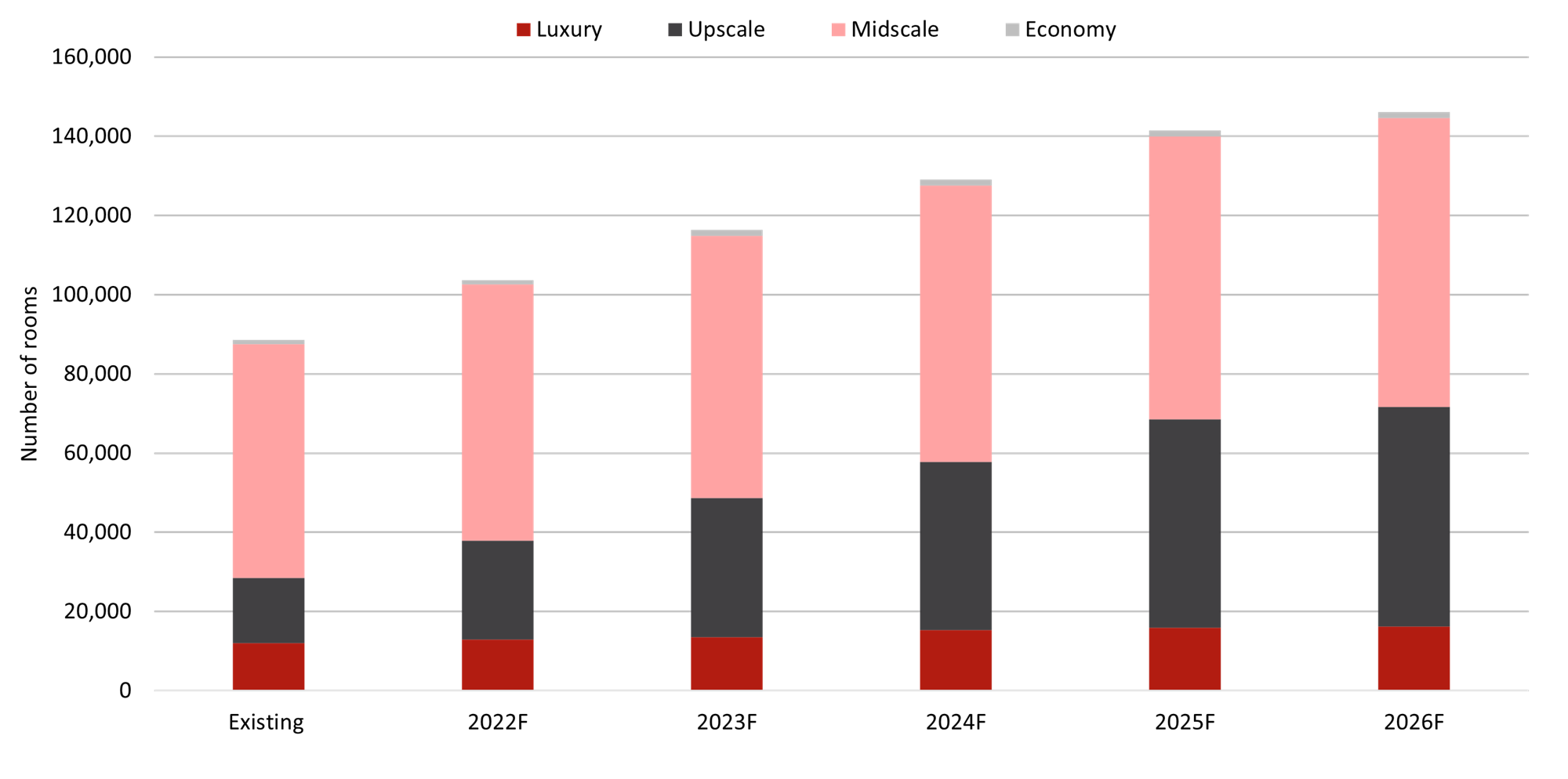

HVS has noted that going forward, there will be 159 additional hotels with approximately 57,547 keys in Vietnam by 2026; 25 hotels with approximately 15,121 keys will be opened by the end of 2022.

Hotel Pipeline (2022 – 2026)

*Exclude non-branded hotels

Source: HVS Research

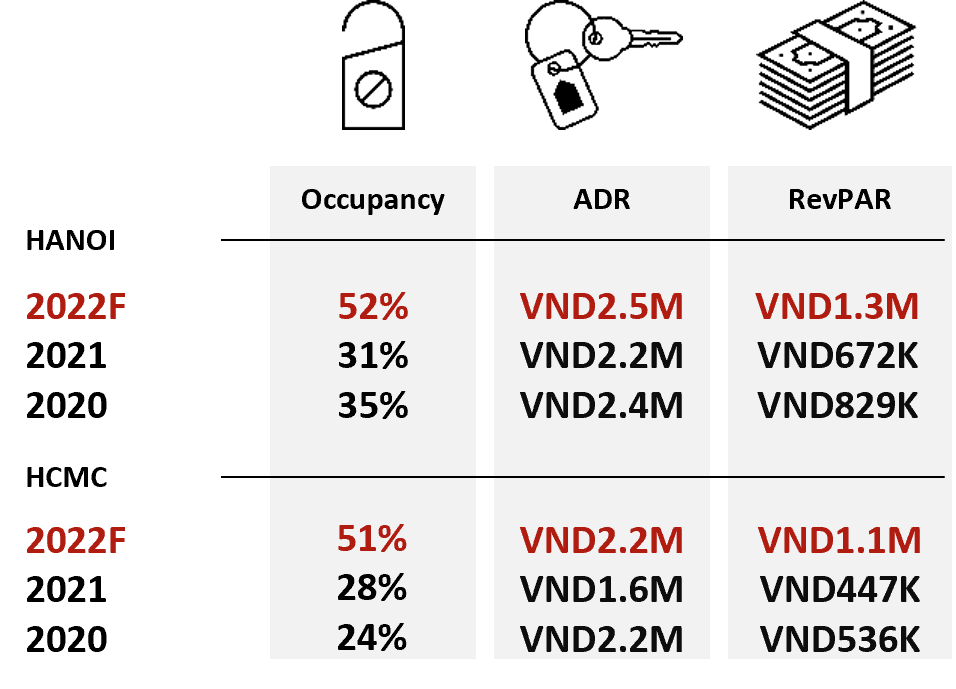

Hotel Performance

Source: HVS Research

As of YTD June 2022, occupancy in Hanoi and HCMC increased by 6.4 p.p and 12.4 pp respectively. Similarly, ADR increased by 4.8% and 14.1% for Hanoi and HCMC respectively, therefore RevPAR has also increased by 25.7% and 69.8% respectively. The opening of the international border has helped to improve RevPAR for both cities.

Transactions

From 2017 to YTD June 2022, the majority of the transaction activity occurred in Hanoi, accounting for 75% of the transactions. Transactions in other cities include Capri by Fraser Ho Chi Minh and Somerset Central TD located in Hai Phong. There was no transaction recorded in Vietnam in YTD June 2022.

Transaction Value Recorded by Year (2017 – YTD Jun 2022)

Source: HVS Research