by J. Carter Allen, Rodney G. Clough

HVS continually tracks the rates of return on the assets that we consult on. In our most recent review, we found that equity yield rates, on average, have been declining, due in part to the expectation of slowing EBITDA Less Replacement Reserve growth. The sample size of available data is also a contributing factor.

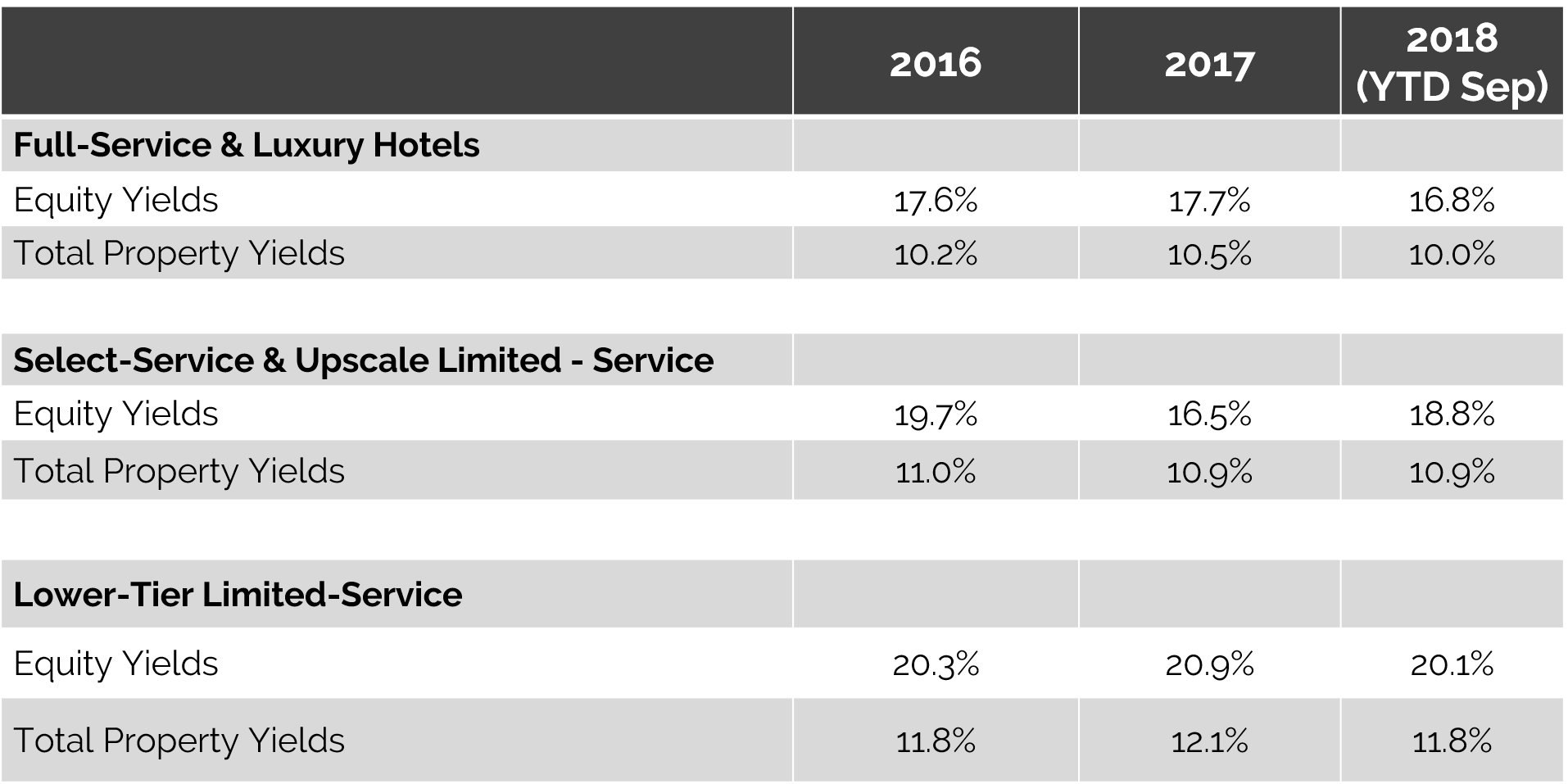

Equity yield rates were notably lower for full-service and luxury hotels, averaging 16.8% for the year-to-date 2018 period (below the 17.7% level recorded for 2017), driven largely by a lower number of total transactions of this asset type, coupled with an increase in full-service sales of iconic assets in highly sought-after coastal markets with high barriers to entry.

Equity yield rates for select-service and upscale, limited-service hotels averaged 18.8% for the year-to-date period ending September 2018, while the average equity rate for lower-tier limited-service hotels was 20.1% for the noted 2018 period. We note that the comparatively greater risk of supply growth within these asset classes contributes to investors’ need for higher hurdle rates on equity investments.

Source: HVS

Total property yields (overall discount rate) similarly declined for full-service and luxury hotels, while holding steady in the other categories. Total property yields are averaging 10.0% thus far in 2018 for the full-service and luxury category. Higher levels of 10.9% for select-service and upscale limited-service hotels, and 11.8% for lower-tier limited-service hotels were recorded. This relationship to equity yields also reflects expectations of increased debt costs for hospitality investments.

Rates of return are calculated using the actual sale prices of the hotels with forecasted cashflows, and inputting market terms for fixed-rate financing on a ten-year hold.