By Tim Smith, Tshepo Makhudu, & Laura Dutrieux, HVS

Highlights Welcome to the third edition of the African Hotel Valuation Index (HVI). We are thrilled that the number of markets included in the study continues to grow. In the first edition we had 14 cities, that grew to 18 last year and this year it has increased again to 21 cities in 16 different countries. A 50% increase in markets in such a short space of time is indicative of the ever increasing interest in the African hotel market. Moreover, and equally importantly it also illustrates an improved transparency and increase in data across the continent.

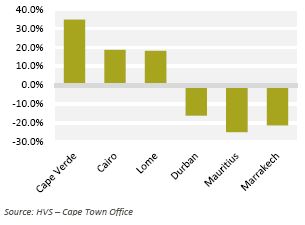

CHART 1: TOP AND BOTTOM THREE – PERCENTAGE CHANGE IN HOTEL VALUE PER ROOM (US$)

It is becoming as important to look at performance in local currency as in US$. Although revenue from abroad will continue to form part of the attraction of hotel operation and investment in Africa, local demand is becoming increasingly important. Many markets are showing a drop in value in US$ this year, in local currency terms, hotels have performed well and had another good year. However, values are reported in US$ to allow some level of comparison between markets, and also because much lending and investment is made in US$.

As with all hotel investment, anywhere in the world, there are many influences outside the control of hotel managers and brands that can impact the trading cycle; currency fluctuations being only one. Unfortunately, again we have to mention terrorism and the threat of terrorism, especially in the North African markets. If there is a silver lining to the cloud of terror over Turkey and parts of Europe, it may be that tourists may be displaced to new markets, including some in Africa. Similarly, with travel advisories being lifted for East Africa the possibility of safari and sun holidays in Kenya and Tanzania will increase for more tourists.

Accessibility and visas remain key issues for both tourists and commercial travelers. However, there is an increase in low cost airlines, and others are expanding and increasing code share agreements. Kenyan Airways and Ethiopian Airlines are continuing to expand and South African Airways, through their various affiliates serve an increasing number of regional cities in southern Africa. Visas remain a challenge and visitors to many African countries will either have a long and costly wait for a visa before they fly or on arrival; either will deter many. However governments are aware of the problem and appear keen to find a solution; the latest being the African Union discussing the possibility of an African Passport. Things do not change quickly in Africa, but every journey starts with a single step…

The other major challenge facing some of the markets included in the HVI continues to be commodity prices. Oil prices have increased in recent months, however the price per barrel remains below $50, adversely affecting economies and demand for hotel rooms.

Despite some short term challenges hoteliers of all sizes continue to expand, it is not just Accor Hotels, Hilton and Rezidor that have substantial pipelines of hotels under development, smaller regional chains including Azalai, City Lodge, Onomo and Protea all continue to expand. The long term climate for hotel development and investment remains sunny and we look forward to growing the HVI into new markets over the next few years.

The Stars of the Show In absolute value terms, the top three markets remain the same as last year; Seychelles, Abuja and Addis Ababa. However more interesting is the change in trends and the growth in values of the markets. Some of those demonstrating the highest growth are still in recovery mode, and building from very low bases. However, others such as Addis Ababa are strong success stories. With several new hotels about to or recently opening in the city, performance may slow slightly for the next couple of years whilst that new supply is absorbed. However, the trend continues to be impressive.

One of the newcomers, Cape Verde, is also showing positive growth. The archipelago is an interesting market with plenty of new rooms entering the playground, yet performance continues to grow. This is clearly a market to watch over the next few years.

Despite the ongoing turmoil in Egypt, these markets continue to improve, although it should be noted values remain less than half that of pre-crisis levels in Cairo.

CHART 2: HOTEL VALUES – PERCENTAGE CHANGE 2010-15 (US$)

Market Overviews Botswana – Gaborone

Botswana is one of Africa’s success stories. Real GDP growth has been around 5% per annum over the past 10 years. After suffering negative growth in 2015, mainly due to the downturn in China and falling commodities prices, the economy is forecast to grow around 3.7% in 2016.

The Botswana hospitality industry is one sector of the economy continuing to thrive. Marriott has recently announced a new 160 bedroom Protea hotel in the Gaborone CBD. Cresta Hotels has announced the opening of the 83 bedroom Cresta Maun resort in 2017. Much of the economic success is a result of sound macro-economic policies; resulting in the World Bank describing Botswana as “a development success story”. This strong endorsement is assisting the overall demand for hotels for business travelers in Gaborone. In addition Botswana is lucky enough to have two of the outstanding tourist destinations on the continent, Chobe National Park and the Okavango Delta, thus drawing significant numbers of leisure travelers to the country. Combined, business and leisure travelers have resulting in occupancy of 65-70% over the past few years. Such stable performance, despite a growth in ADR (in local currency) demonstrates the health of the market. An improvement in global economies is crucial to further growth in the Gaborone hotel market; higher demand and prices for commodities

and diamonds will lead to increased corporate demand, whilst improved economic confidence at home will encourage more tourists to the country.

Cape Verde Cape Verde’s economy is an exemplary example of a stable political environment and a working democracy. A steady economic growth path has been followed by a rising quality of life for its citizens. This is all despite the country not having an abundance of natural resources, occasional drought and a small agricultural base. Given this success and the ability of the islands to attract European guests for leisure breaks, we felt it was an interesting market to include in the HVI.

Tourism is one of the main contributors to the economy of Cape Verde. Foreign direct investment is active in the country due to high levels of investor confidence arising from a stable political and economic environment and a growing market. The country attracts tourists from Europe, in particular the United Kingdom, Germany and Portugal due to strong national and cultural ties

The hotel industry is a beneficiary of the FDI that the country enjoys. A new Resort Group property is being constructed on Sal Island and will be ready in November 2016. Thereafter they have plans for several other hotels in the main islands, all of which will be branded by international hoteliers.

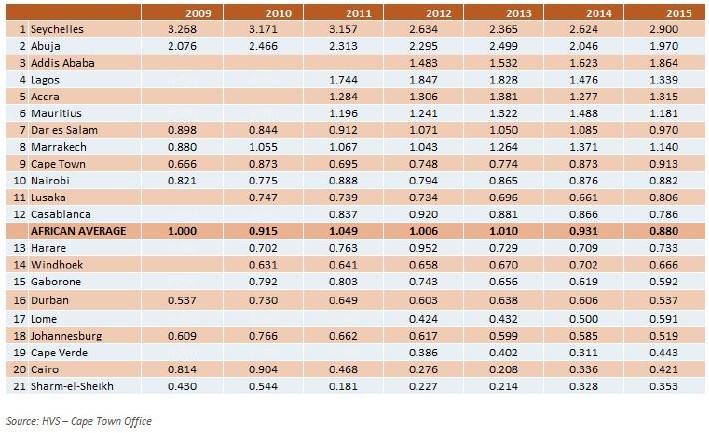

CHART 3: HOTEL VALUATION INDEX 2015

The market is evolving rapidly and as such neither occupancy nor ADR can be seen as stable, yet. However, as both the number of visitors to the islands and hotel supply continue to increase the future for the hotel industry looks positive.

Egypt – Cairo and Sharm el Sheikh Egypt has had more than its fair share of terror-related incidents over the last twelve months. Politically the country still has issues to resolve with marathon court cases against the Muslim Brotherhood featuring prominently in global media. Security concerns are currently exerting a negative impact on the country’s tourism outlook.

The economic landscape of Egypt has been a mixed bag. The biggest news was the announcement of a planned $60 billion infrastructure investment by Saudi Arabia. The economy started to recover in 2014/15, as the government scaled up infrastructure spending and undertook important measures to restore macroeconomic stability. As such the World Bank reported, growth rebounded to 4.2% in 2014/15, double the growth during the previous four years.

In Cairo, occupancy increased to above 50% whilst ADR remained flat. The performance can be attributed to the return of international visitors to Egypt after the political unrest of late 2013 and early 2014. Travel resulting from Eid al-Adha also aided performance in the market. Hotel values still achieved a respectable 18.6% increase in 2015, although remain below the levels in 2011.

Sharm-el-Sheikh has not had the same fortunes as Cairo. Occupancy levels plunged in Sharm El Sheikh in November following the crash of a Russian civilian aeroplane in early November 2015. A subsequent ban on travel and cancellation of flights to the region from Russia and various European countries severely impacted performance in the Rea Sea destination. Despite challenging trading values improved slightly, although Sharm remains in last place on the HVI.

Ethiopia – Addis Ababa With a “double-digit” GDP growth that is now something of an official mantra, Ethiopia has become the fastest growing economy in the continent and is commonly referred to as “the capital of Africa” for its political, diplomatic and commercial significance.

The increasing number of inbound tourists along with the new supply of offices in the market enhances a significant demand for international standard hotels, which remains for the most unsatisfied. In 2015, 1 million travelers could not find accommodation up to their standards in the city and there will be 3 million in 2020 if new hotels are not built, according to Awash International Bank. In addition, the large diplomatic community and the political activity in Addis Ababa will push MICE activity up significantly.

Addis Ababa concentrates 80% of the Ethiopian’s hotel supply much of which is outdated and of poor quality. However, the strong economic fundamentals along with the improvement of the infrastructure attract an increasing number of international hotel groups which will account for 46% of the new supply in the next few years.

Occupancy and rates have been steady in recent years. Addis Ababa experienced occupancy regularly up to 80% and the country has the highest room rate in the continent, according to a survey carried out by STR Global in late 2015.

Hotels’ values in Addis-Ababa have been consistent over recent years, rising steadily. They were approximately twice the value of the African Average in 2015. Given the existing level of unsatisfied demand, the new supply is not likely to affect the long term occupancy, and the new branded hotel will push the average rate up, positively impacting the RevPAR. Therefore, value should be sustainable.

Ghana – Accra The concentration of Ghana's international tourist arrivals still revolves between the nation's capital city Accra, and the mining and agriculture regional destinations. However, there is growing demand for hotels in Ghana's second and third tier markets, with many players taking note of the massive potential.

Stakeholders such as hotel operators, investors, developers and the government sectors are closely following the new investments 'hot spots' of Ghana. Hotel chains such as Hilton, Moevenpick Hotels & Resorts, IBIS Styles, InterContinental Hotels Group, Marriott International, Golden Tulip, as well as Ghana's domestic hotel groups such as Fiesta Hospitality Group and African Regent have indicated their intentions of strengthening the presence of their economy to mid-scale brands in the market.

Overall, Accra’s tourism industry can expect strong long-term potential, bolstered by rising demand for international, domestic and regional travel.

Future additions to the current supply of hotels will continue to exert some pressure on values. With the recent launch of the Kempinski Accra and the Ibis Styles properties values have fallen slightly in US$ terms, although at a slower rate than previous years.

Indian Ocean – Mauritius and Seychelles With blue waters and wonderful climate, Mauritius and the Seychelles (together with the Maldives and Zanzibar) are the dream tourist destinations on the Indian Ocean.

Mauritius registered 1,150,000 tourist arrivals in 2015, which translates into an 11% increase from 2014. South African Airways has further strengthened its routes to Mauritius due to growing demand – both from the continent and internationally.

Mauritius recorded double-digit increases in occupancy although in US$ terms RevPAR was down around 25%, in local currency there was an impressive 12% increase. The long term future for the island is positive with the government growing the economy in different sectors, all of which will need hotel accommodation. In addition increased airlift direct from Europe should sustain demand for the resorts. Announced new hotels include Park Inn by Radisson in Quatre Bornes, the new commercial hub of Mauritius.

Seychelles has seen much political turmoil after it earned its independence from Britain. However, since a political coup d’état took place in the mid 1980s, the country has not looked back.

Seychelles has recently won a tourism attraction award, the Most Scenic Holiday award at the International Travel Expo (ITE). Besides marketing aggressively in the Indian Ocean countries such as India, Dubai, UAE and many others, Seychelles is achieving success in such western countries as Brazil and others in South America.

Hotel trading performance in 2015 was encouraging with stable occupancy and growth in RevPAR. This, despite the islands having to secure new sources of business in recent years and now focusing more on the Asian markets. HNN has shared the encouraging view that “Chinese travelers are arriving in larger numbers; the island enjoys some of the highest room rates in the world; more than 2% of arrivals come via private plane”

The Seychelles hotel industry has seen an increase in hotel values of 4.6% in 2015.

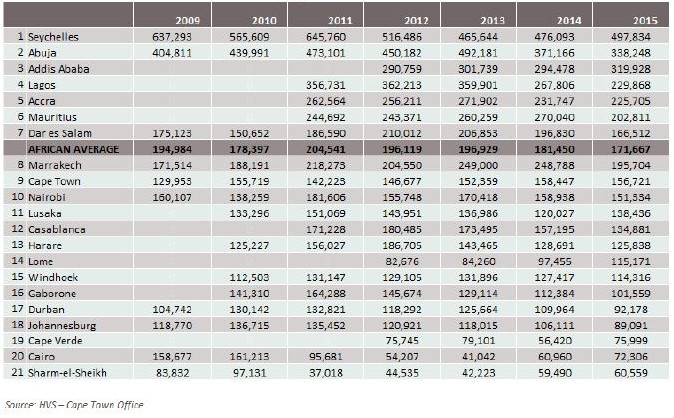

CHART 4: HOTEL VALUES PER ROOM 2009-2015 (US$)

Kenya – Nairobi Although the prospect of presidential elections in 2017 may have a negative effect on hotels’ performance, the visit of the President of the United States, Barack Obama, and his Holiness the Pope last year should lead to an increase in interest for the country.

Nairobi’s hotel market presents a mixed picture. While non-branded hotels are struggling and the market performance is down (overall REVPAR down by 6.2%), the international hotel groups continue to see Kenya as a lucrative market for expansion. 2016 – 2018 will see a massive increase in supply of branded hotels offering international standards.

Concurrently, Kenya’s hotel market offers significant investment opportunities owing to its position of regional hub for leisure tourism, finance, government and commerce. Foreign investment continues to flow into Kenya, the World Travel and Tourism Council forecast a 5.2% growth in capital investment per annum until 2025. The huge increase of new supply results in a fall in RevPAR. As a result, hotels’ values in Nairobi are down 4.8% in 2015. Room supply continues to be a challenge and local demand in Nairobi is now as important as international. As a result, rooms demand is weaker, and that has a negative impact on the overall hotels’ profitability. Increased confidence from international travelers along with the growing supply of international brands should boost hotels’ performance in the market and therefore hotel values.

Morocco – Marrakech and Casablanca Morocco has been one of the better performing political and economic countries in the North African region. According to Trading Economics, Morocco’s GDP grew from a paltry 1.8% in January 2015 to a respectable 4.5% at the end of the year. This stellar performance can be attributed to a stable economic environment and an established tourism industry. The WTTC reported Morocco’s tourism industry contributed 7.7% to the country’s GDP in 2015 and is projected to grow by 4% between 2016 and 2026.

Marrakech had a tough year in 2015 with falls in both occupancy and ADR, resulting in a fall in RevPAR of 21%. France remains a key market for the country as a whole so the increased terrorism in France and general nervousness surrounding North Africa, meant many tourist chose not to travel to the country.

Casablanca on the other hand has also seen a drop in performance, albeit more marginal than for Marrakech. Occupancy fell slightly and ADR was flat in local currency terms.

The 186-room Four Seasons Hotel Casablanca has opened, marking Four Season Hotels and Resorts’ second property in Morocco.

Values in Marrakech and Casablanca fell significantly in 2015 and are only likely to recover once the general security situation improves.

Namibia – Windhoek Namibia's economy is integrally linked to that of South Africa and the rest of Southern Africa. Based on this consideration, the same headwinds that are faced by South Africa will have an impact on the Namibian economy, with low growth prospects being the order of business. Sluggish global demand and low prices for its key commodities exports will continue for the foreseeable future.

The outlook for tourism in Namibia remains bright, as it is boosted by incredible natural attractions. The government is actively involved in supporting and marketing the country to source markets through several international offices. The Department of Environment and Tourism coordinates tourism legislation and is supported by such bodies as Namibian Tourism Board, the Federation of Namibia Tourism Association, Hosea Kutako International Airport, Ministry of Home Affairs and Immigration. Hotel performance in Windhoek broke with a three-year growing trend in 2015 with a drop in occupancy, although it remains well ahead of historic levels. There was an impressive 8% growth in ADR in local currency.

CHART 5: YEAR-ON-YEAR CHANGE IN VALUES PER ROOM BY REGION 2010-15

Hilton Worldwide has announced the signing of a management agreement with Out of Africa Hospitality to open a mid-market Hilton Garden Inn hotel in Windhoek, Namibia. The new property will open adjacent to the existing Hilton Windhoek in 2017.

In US$ hotel values remain strong, although the trend has fallen due to the currency fluctuation.

Nigeria – Abuja and Lagos Nigeria is one of the countries that were most adversely affected by the commodities and currency crises. The country has not reported a single case of Ebola since the crisis was declared over, however Boko Haram has not yet been brought under complete control

Total international tourist arrivals in 2015 did not exceed 2014 levels, however Nigeria has a larger domestic tourism market. In 2015 Lagos experienced an increase in occupancy compared to 2014 although below historic levels. Unfortunately the change in focus to domestic travelers has resulted in a sharp fall in ADR. STR Global analysts cite Boko Haram conflicts in the country as well as uncertainty during the Nigerian general elections and low oil prices as negative factors contributing to Lagos’ overall performance.

The long term remains positive with Carlson Rezidor announcing the signing of its first Quorvus Collection in Africa: the 5-star, 244-room luxury Emerald Grand Hotel & Spa in Lagos, Nigeria.

Abuja hotels saw an increase in occupancy in 2015 despite the Boko Haram insurgency. Average room rate did not perform as well with a substantial decrease from $325.00 to $275.00. Like Lagos, this is due in large part to the lack of international guests and an increase in local guests. Many new hotels are planned for Abuja over the next five years, which illustrates the confidence in which the market is held for the longer term.

Accordingly, both Lagos and Abuja experienced reduced hotel values, however these reductions were less severe than 2014.

South Africa – Johannesburg, Cape Town and Durban South African Tourism, the marketing wing of the government’s Department of Tourism, continues to perform an important function of keeping the country top of mind when it comes to holidaymakers and business travelers. The Home Affairs Department has eased the new entry visa regulations that had such a negative impact on visitor numbers in 2015. The currency exchange rate has had a positive impact on tourism numbers and these are expected to rise even further. Brexit raises fresh concerns for the tourism market in South Africa, given the large number of British tourists who visit the country. Uncertainty over their economy at home and the weakening of Sterling may deter many from long haul trips.

Johannesburg enjoyed the highest level of occupancy for at least six years and strong ADR performance, with RevPAR growing by 16% in local currency. Unfortunately the performance of the Rand against the US$ masks this strong growth.

Marriott has announced plans to construct a flagship hotel at the Melrose Arch, which is a popular mixed-use development providing a live, work and play environment outside the central business district.

Cape Town saw a small dip in occupancy to 66%, but ADR (in US$) remained steady, despite the weakening of the Rand against the US$. In local currency there was a 30% growth in ADR. This represents four consecutive years of strong performance, proving the oversupply is fully absorbed. This is further illustrated by Tsogo Sun Group starting construction on a 500-room hotel complex comprising three brands in Cape Town. There is a planned development at the Capetonian Hotel in Heerengracht; and the Gorgeous George Hotel and Bar development being constructed in St Georges Mall. All these hotels are located in the central business district.

Durban is the only Commonwealth country city that agreed to play host to the 2022 Commonwealth Games. Preparations have started with the announcement of many commercial projects. Durban hotel performance was more or less in line with that of the other two South African cities we are covering with growth in both occupancy and ADR.

Hotel values in South Africa rose impressively in 2015 in Rand terms, due to a steady increase in revenue per available room. However, in dollar terms the country has not done so well, with a 16% drop in value for Johannesburg and Durban in 2015. Cape Town bucked the trend with only a marginal decrease in US$ terms. This performance is consistent with the currency crisis that was evident throughout all the emerging market economies.

Tanzania – Dar es Salaam Landlocked Uganda has announced it will build a major pipeline to export its oil through Tanzania. This is seen as a major source of confidence in Tanzania’s stability and safety profile. From this major infrastructure investment Tanzania can generate more FDI and capitalise on the benefits of a subsidised route for its own oil.

Dar es Salaam saw a 12% increase in room supply in 2015, unsurprisingly occupancy fell significantly. The 2015 elections will also have affected demand.

However, positively there was a substantial increase in ADR in local currency, pushing RevPAR up almost 7%. A 20% fall in value of the Shilling against the US$ results in a fall in value in the HVI, although it should be noted in local currency terms there was a noticeable increase in value.

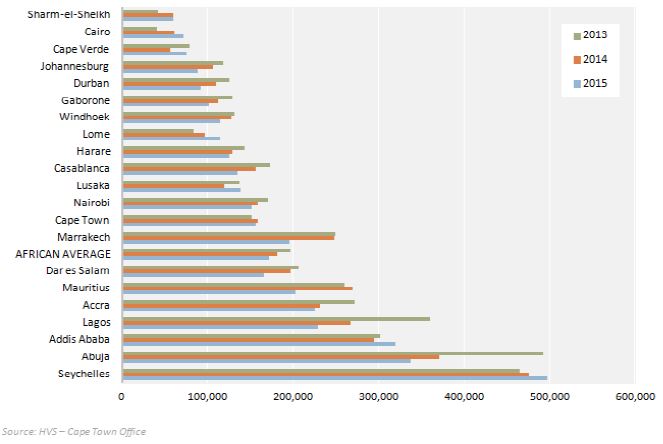

CHART 6: HOTEL VALUES PER ROOM 2011-15

Togo – Lome 327,000 visitors from far and wide enjoyed the wonders of Lome in 2013. With tourism contributing 3.1% to the GDP of the country, the tourism market remains underdeveloped. Most of the major infrastructures are inadequate and the roads’ network is deficient in the capital.

Togo has a limited and uneven hotel supply. In 2012, rated hotels represented 900 rooms and 6 units in Lome. Accor Hotels and Carlson Rezidor are the only international brands operating in the city. In addition to the international chains, Group Onomo and Grupo Prefaco opened 2 hotels in Lome in 2014. Most of the

hotels in Togo are state owned, although it’s now changing as the government wants to sell them to private investors. The government does not invest in any refurbishment or renovations, and does not have any hospitality expertise, leaving the properties outdated and under-performing. The on-going process of decentralization should encourage private investors and boost the premium travel accommodation supply in the country.

However, behind this layer of negativity, Lome has a real potential to grow its tourism activity. The level of occupancy had been stable since 2011, showing a rebound in 2015. ADR and REVPAR have been significantly up reaching a peak of +18.2% in REVPAR last year, boosted by the newly opened international hotels attracting demand from international travelers. Hotel values have thus experienced positive and encouraging trends, with double-digit growth over the two last years.

Investors are increasingly considering Togo for investment. The inflow of Foreign Direct Investment increased by 61% in 2013 and 49% in 2014.

Despite overall positive trends, Lome still needs to address key challenges to be able to develop. In addition to the poor infrastructure, hotels in Lome tend to be overpriced, compared to the product offering and airline fares are dissuasive for travelers.

Zambia – Lusaka The copper mining industry in Zambia has impacted the economy of Zambia in the same way other emerging markets whose economies are supported by commodities. As an alternative strategy at maintaining economic growth, Zambian authorities are looking at the tourism industry. Initiatives such as the Zim-Zam UniVisa and the eVisa are targeted at increasing tourist arrival figures by simplifying movement across African countries

The Zambian Investment Agency expressed optimism that the country was able to capture the targeted 1 million tourist arrivals in 2015. According to the Zambia Tourism Board (ZTB), Zambia received more than 946,000 tourists in 2014, Zambia Airports Corporation Limited reported 1.36 million arrivals in 2012, with international visitors accounting for 1.14 million, illustrating current levels are significantly below historic numbers. The Chinese are still regarded as a prime source of tourists into Zambia and will continue to be targeted.

Performance of hotels in Lusaka was relatively stable in 2015 with a marginal increase in occupancy and a small drop in room rate. As a result hotel values in Lusaka fell only slightly in 2015 (-2.6%), compared to a massive drop in 2014 (-12.4%). Companies clearly view this as a short term problem as Hilton Worldwide has announced the development of a brand new Hilton Garden Inn which is targeted to open in 2017 and Quantum Global purchased the Intercontinental Hotel Lusaka from Kingdom Hotel Investments.

Zimbabwe – Harare Known as “a world of wonders” in Southern Africa, Zimbabwe welcomes more than two million tourists a year,

Although tourism contributes 10.4% to the GDP of the country, the tourism market remains underdeveloped. Most of the major infrastructures are outdated and roads need to be upgraded. Political unrest and violent strikes shake the country and many Zimbabweans have left their homeland.

Hotel supply has not grown for the past five years and is mostly made of local unbranded properties that struggle to adapt to the needs of international tourists. Harare lacks international hotel brands which would bring quality and expertise to the current tourism landscape.

However, the country has a real potential to grow its tourism activity. The level of occupancy has been increasing since 2014, proving a rebound in demand from international tourists. While ADR and REVPAR are down, owing to the competitiveness of bordering countries, the picture may change quickly. Indeed, global hospitality brands have started showing interest in the nation. Carlson Rezidor recently announced the opening of a Radisson Blu Hotel in Harare in 2019, and it will certainly encourage competitive brands to enter the market.

Investors are increasingly considering Zimbabwe for investment. Capital investments are expected to rise by 4.8% per year over the next ten years. China is being a precious ally: President Xi Jinping confirmed multi-billion investments in energy and infrastructure and the cancellation of US$40 million in debt in exchange of the yuan becoming Zimbabwe’s international currency. This should push the number of business tourists from China in need for a hotel room.

The government will need to tackle significant challenges in the next few years to be able to take advantage of this increasing demand, get the ADR back to previous level and boost hotels’ values on the market.

Outlook The World Travel and Tourism Council reported the direct contribution of travel and tourism to the South African economy in 2014 was 3% of GDP and is expected to grow 4.6% per annum to 2025. In other African countries it is substantially more. Governments are realizing the importance of hotels and associated industries to the economy and are starting to assist in the evolution of the industry. With government support on flights, visas and currency controls the hotel industry is well placed to grow well above inflation and exceed returns from other real estate sectors. There is demand from brands and operators and both tourists and commercial travelers continue to travel to the continent. In addition as economies develop, demand will continue to grow from local and regional guests; providing demand year round for operators.

There will come a time shortly that demand for hotel staff exceeds supply, given the sheer number of new hotels opening, so thought should be given to training and attracting new staff, at all levels, across the industry. Hotels are one of the few industries that requires such a wide variety of skills and abilities; they provide a significant opportunity to increase employment in an area. This alone justifies strong government support.

Challenges will continue to be thrown at the industry, and based on historic performance the industry will overcome these hurdles and continue to grow. Regional economic unions such as ECOWAS and SADC are becoming more important as economies grow; by working together regional countries can increase demand for hotels. Combined with the African Union, and most importantly a realization and desire to grow and work together the future of demand for hotels in the continent looks positive. There will continue to be short term issues to overcome, but with an underlying trend of positive trading and demand the performance of hotels in the medium to longer term should be impressive.

Understanding the HVI The HVI is a hotel valuation benchmark developed by HVS. It monitors annual percentage changes in the values of typically four-star and five-star hotels in 21 major African cities. Additionally, our index allows us to rank each market relative to an African average (see Chart 3). The HVI also reports the average value per room, in US dollars, for each market (Chart 4). All data presented are in US dollars.

The methodology employed in producing the HVI is based upon actual operating data from a representative sample of four-star and five-star hotels. Operating data from the STR Global Survey were used to supplement our sample of hotels in some of the markets. The data are then aggregated to produce a pro forma performance for a typical 200-room hotel in each city. Using our experience of real-life hotel financing structures gained from valuing hundreds of hotels each year, we have determined valuation parameters for each market that reflect both short-term and longer-term sustainable financing models (loan to value ratios, real interest rates and equity return expectations). These market-specific valuation and capitalisation parameters are applied to the net operating income for a typical upscale hotel in each city. In determining the valuation parameters relevant to each of the 21 cities included in the African HVI, we have also taken into account evidence of actual hotel transactions and the expectations of investors with regard to future changes in supply, market performance and return requirements. Investor appetite for each city at the end of 2015 is therefore reflected in the capitalisation rates used.

The HVI assumes a date of value of 31 December 2015. Values are based on recent market performance, but the capitalisation rates reflect the expected future trends in performance, competitive environment, cost of debt and cost of equity. As our opinion of value remains an opinion of Market Value, when analysing transactions and in assessing the opinions of value we have attempted to remove all aspects of distress. The parameters adopted assume a reasonable level of debt and investor sentiment. Conversely, the values reported may not therefore bear comparison with actual transactions completed in the marketplace. However, this is the best approach to retain the integrity of the HVI as a rolling annual index over the longer term.

The HVI allows comparisons of values across markets and over time by using the 2009 average African value of US$194,984 per available room (PAR) as a base (2009=1.000). Each city’s PAR value is then indexed relative to this base. For example, in 2013 the index for Seychelles was 2.671 (US$521,781/US$195,368), which means that the value of a hotel in Seychelles in 2013 was a little more than twice that of the African average in 2009