September 23, 2016

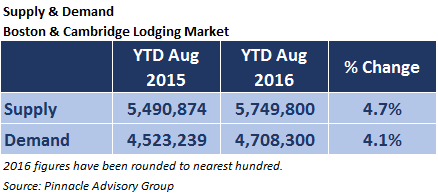

While demand year-to-date through August is up a strong 4.1% in the Boston/Cambridge lodging market, it has not been enough to compensate for the growth in supply which has grown 4.7%.

Driving the supply growth, the aloft and element hotels opened in the Seaport, the Godfrey Hotel opened in Downtown Crossing, and the Hotel Commonwealth completed its expansion, all of which took place in the Q1 2015, the market’s slowest months. On the demand side of the equation, the local lodging market experienced an increase in demand every month of the year, although the pace of demand was somewhat volatile. Specifically, the months of March and May were particularly problematic where demand growth was less than 1.0%.

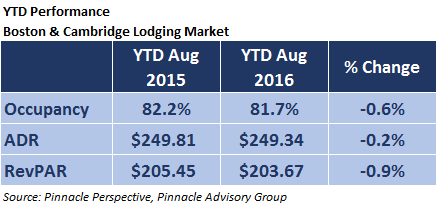

The shortfall in demand relative to supply has resulted in a 0.6% decline in occupancy through August. After a lackluster first quarter, RevPAR was 2.8% below its 2015 level. Corporate transient demand began to slow in the second quarter and was unable to make up for the market’s soft group pace. As this higher rated demand declined, operators were forced to replace it with lower rated leisure demand, and in some cases contract and government demand, resulting in a shift in mix and lower ADRs. Further, AirBnB and other home sharing services have made it difficult to drive rates on peak nights which historically sell out and allow for substantial rate growth. The decline in both occupancy and rate reflect a 0.9% decline in RevPAR through August.

Remaining Four Months of 2016

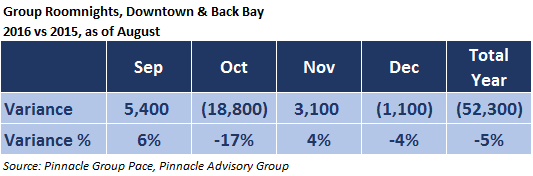

While the group pace for September and November Indicate a welcome improvement over 2015, October is expected to be down almost 19,000 roomnights when compared to the prior year. A decline of this level is similar to those experienced in March and May which contributed to monthly occupancy declines of 4.2 points and 3.7 points, respectively. Transient demand is not expected to pick up in October with the combination of the Jewish Holidays and Columbus Day Weekend negatively impacting mid-week group and corporate demand.

The Red Sox may be one factor which could alleviate some of this decline. With less than two weeks left in Major League Baseball’s regular season, the current five game lead held by the Red Sox is on the mind of many hopeful operators. Hotels in Fenway and Back Bay especially would benefit from an extended season into October, something the Red Sox haven't achieved since 2013 when the team won the World Series and extended their season a full month.

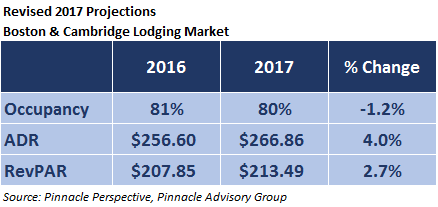

Revised Projections

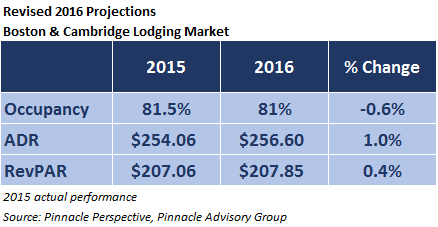

Rachel Roginsky, principal of Pinnacle Advisory Group, presented performance projections for 2016 and 2017 at July’s Massachusetts Lodging Association’s annual Outlook Presentation. Based on updated group booking pace reports, year-to-date performance presented above, and conversations with local operators, Pinnacle’s projections have been revised slightly for the balance of 2016. While one event does not significantly alter annual results, we recognize from prior experience that an extended Red Sox season could be a boost for the lodging market, and potentially help swing year end 2016 RevPAR from nearly flat to up a full point.

Lodging supply will increase 4.6% this year, while demand is projected to increase 3.2%. With these growth rates, occupancy is expected to decline from 81.5% in 2015 to 81% in 2016. Despite market ADR remaining almost unchanged through August, Pinnacle believes operators will be able to drive room rates in September and November allowing for an increase of 1.0% for the year. Pinnacle’s revised RevPAR projection of 0.4% growth in 2016 will represent the market’s seventh consecutive year of RevPAR growth.

Pinnacle has maintained its projections for 2017; forecasting continued decline in occupancy yet rate growth of 4.0%, driving growth in RevPAR of 2.7%.

The Pinnacle Perspective data sample is made up of over approximately 95% of the Boston and Cambridge rooms supply. For more detailed information on the market’s performance please contact Sebastian Colella at 617-722-9916 or scolella@pinnacle-advisory.com