By Tim Sauer

HVS prides itself on being a trusted advisor for hotels owners and investors, and we are constantly looking for opportunities to maximize our clients’ cash flows and returns. The following article highlights the basics of cost segregation studies and their potential benefits for our clients. While HVS does not offer this service, we have consulted with cost segregation professionals to maximize its potential benefits in a hospitality context.

The Internal Revenue Code (aka the “IRS Code”) requires that the cost of commercial property be expensed over its designated recovery period. This annual expense, known as depreciation, is a benefit to the owners of commercial properties in that it reduces their taxable income. Generally, commercial real estate is depreciated over 39 years on a straight-line basis. Land is not depreciable and must be shown as a separate non-depreciable asset.

Many owners of commercial real estate set up their depreciation schedules over 39 years, not considering the significant tax savings that might be realized by allocating (or segregating) the property’s cost between its real and personal property components. While failing to properly allocate the property’s cost can be an issue for all commercial real estate types, it can be particularly detrimental for personal-property intensive assets such as hotels.

Introduction to Cost Segregation Services

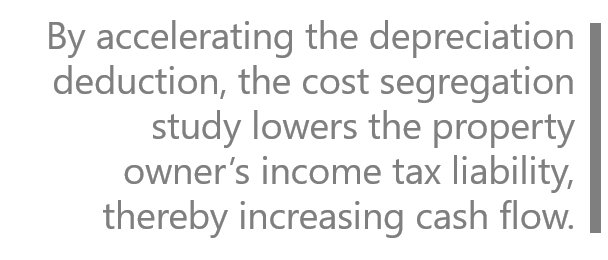

Cost segregation studies are recognized by the IRS as an accepted method of accelerating the depreciation of the property through classifying or reclassifying some of the property’s assets as personal property. By accelerating the depreciation deduction, the c ost segregation study lowers the property owner’s income tax liability, thereby increasing cash flow. Additionally, accelerating the property’s depreciation allows the majority of the benefit to be claimed early in the asset’s life. This savings can be used to shelter income or pay off debt. The savings can also be invested at a significant return to the owner.

ost segregation study lowers the property owner’s income tax liability, thereby increasing cash flow. Additionally, accelerating the property’s depreciation allows the majority of the benefit to be claimed early in the asset’s life. This savings can be used to shelter income or pay off debt. The savings can also be invested at a significant return to the owner.

Through various court cases and rulings, the IRS recognizes that some components of commercial and residential rental property are personal property (Section 1245 property) for the purposes of depreciation. This class of property is depreciated over three, five, or seven years. Hotels, in particular, have a significant amount of property that can be reclassified to shorter depreciable lives of typically five or seven years. These lives are significantly shorter than the 39-year depreciable life of the hotel’s real property (Section 1250 property). Although site improvements are generally classified as real property, there are significant site improvements that are depreciated over 15—not 39—years.

How Cost Segregation Studies Work

For most studies, a cost segregation professional will perform a physical inspection of the property and identify the building components that are eligible to be classified as personal property. In the case of new construction or renovation, a cost segregation professional will often review the contractor invoices as they are submitted, allowing for a more detailed classification of the building’s components. When studies are performed for existing structures (in the case of an acquisition), historical costs are typically not available. Therefore, the inspection will be critical to determining which of the building’s components are eligible to be classified as personal property.

After determining the cost, asset type (real or personal), and proper depreciable life for each of the building’s components, the cost segregation expert will provide the owner with a report that details the findings. This report will include a schedule of assets showing the proper classification of the components, their recovery periods according to the General Depreciation System (GDS), the asset class, and the code section (either 1245 or 1250 property). The property owner’s tax professional then inputs this information into the asset’s depreciation schedule.

There are opportunities to perform cost segregation studies at various stages of the ownership cycle, including new construction, acquisition, and during a renovation or remodel. Even in the event that a property has been owned for many years, a “look-back” study can be performed. Look-back studies examine differences between the depreciation deduction that was actually claimed and the depreciation deduction that should have been claimed had the proper allocation been performed. Properties that are currently booked as solely real property (39-year property) are particularly good candidates for look-back studies. The difference between the depreciation deduction that was actually claimed and what was eligible to be claimed, based upon the cost segregation study, can be taken as a lump-sum depreciation deduction in the current tax year. An amended return is not necessary to claim this deduction. Form 3115, Change of Accounting Method, is filed and submitted along with the current year tax return.

Example of How a Cost Segregation Study Saved a Hotel Owner Money

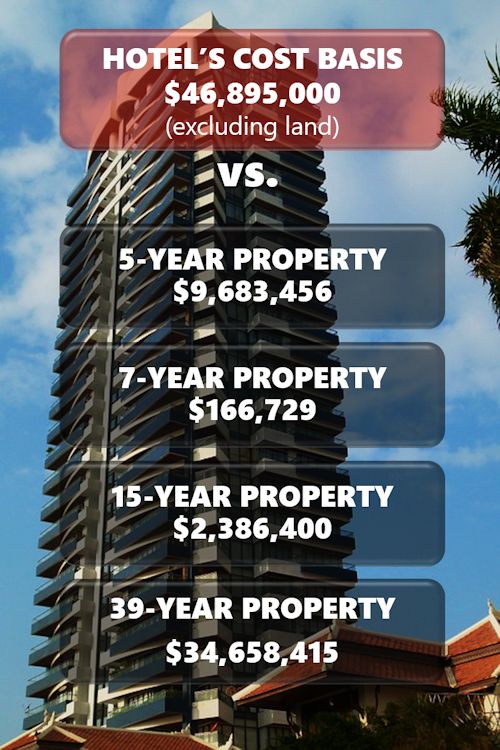

Tim Cody, a cost segregation expert based out of St. Louis, has been performing cost segregation studies for ten years. Mr. Cody provided the following example from a cost segregation study he performed for a hotel with 210 guestrooms, a business center, a fitness center, a pool, and a conference room. The hotel’s cost basis of $46,895,000 (excluding land), which was originally classified as 39-year property, was reclassified as follows:

The estimated savings for the property owner was $765,000 in the first year and $2,362,000 over the life of the property. This savings is based on the owner’s specific reinvestment rate and effective tax rate; actual savings will vary depending on each owner’s tax rate and investment criteria.

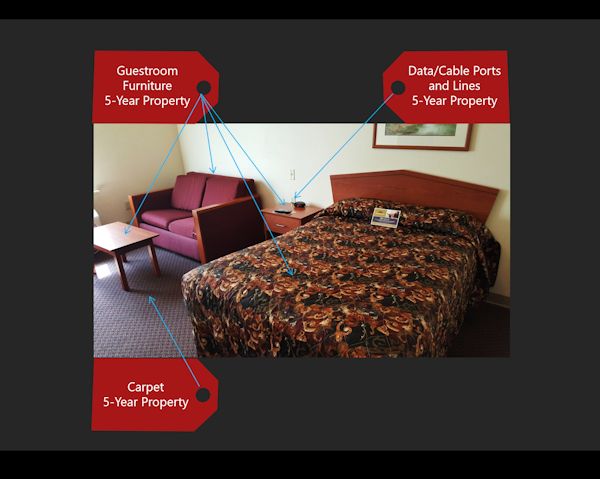

Additionally, HVS provided Mr. Cody with a photograph (see below) of a portion of a hotel guestroom so he could indicate potential reclassification opportunities.

Conclusion

Cost segregation studies have the potential to provide financial benefits to hotel owners—benefits that may have been overlooked. Hotel owners are encouraged to contact their tax professional for more detailed information. HVS is also happy to refer hotel owners to qualified cost segregation professionals. Contact Tim Sauer, MAI, at (314) 922-6734 or tsauer@hvs.com.

While HVS does not perform cost segregation studies, our engineering and architectural division (HVS Design) is frequently engaged to allocate costs for a variety of other purposes. For example, HVS Design is engaged by clients constructing or renovating hotels to segregate the personal and real property costs for permitting fee or property tax purposes. Additionally, HVS Design is able to segregate project costs to determine the project’s eligibility for various tax credits, such as energy or Brownfield tax credits. HVS Design also segregates costs for projects with multiple funding sources to delineate which costs should be paid by the various parties in joint ventures, condominiums, or other similar split-responsibility contracts.