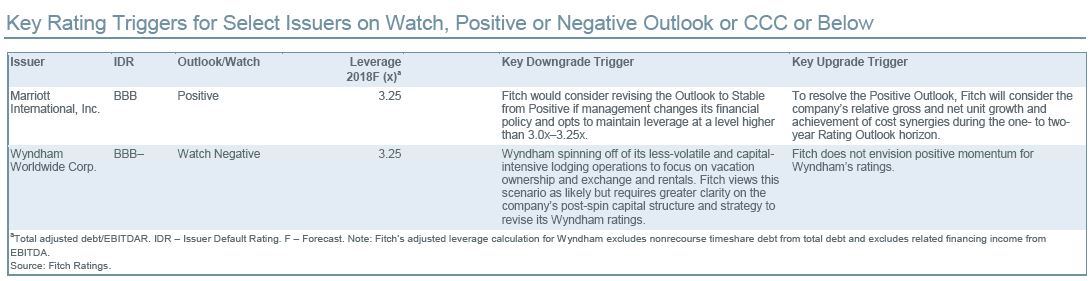

Sector Outlook and Rating Trajectory

Fitch’s Sector Outlook: Stable Fitch Ratings has a stable U.S. lodging sector outlook for 2018, based on expectations for continued, low-single-digit (0%–2%) RevPAR growth. Higher average daily rates (ADR) will drive industry RevPAR; new supply will exceed demand growth, resulting in modest occupancy losses. The larger brand owners will continue to generate outsized unit growth driven by scale economies.

Rating Trajectory: Static Fitch has a Stable Rating Outlook for the lodging sector during 2018, with most issuers managing leverage within their stated target range. Credit protection metrics will likely remain steady as the lodging cycle winds down. Lodging REITs and C-Corps with large owned-hotel portfolios will experience more pressure on margins and FCF as RevPAR growth decelerates. Financial policy will continue as a key rating factor for brand owners.

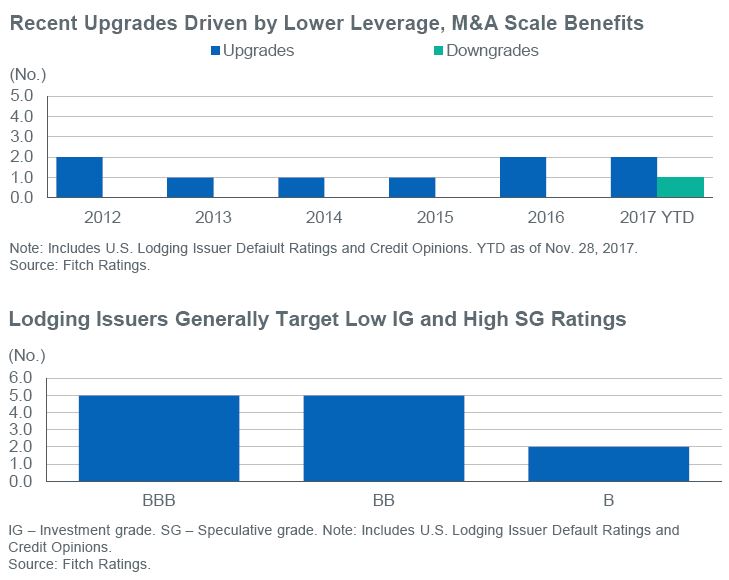

Rating Distribution Weighting: Diversified Scale and diversity are key differentiators between investment- and speculative-grade lodging C-Corps. Most larger, established lodging issuers target low investment-grade (i.e. BBB category) ratings, believing this offers the appropriate balance of flexibility and prudence given the inherent cyclicality of the industry. Smaller lodging REIT credit profiles are constrained by comparatively weak credit metrics and weaker contingent liquidity from secured mortgage debt access in the context of REIT regulatory cash retention constraints.

What to Watch

- Signs that stronger corporate profits and spending are boosting business travel.

- The U.S. dollar and international traveller sentiment towards visiting the U.S.

- Elevated new supply in key urban markets, including New York City.

- M&A event risk, largely between smaller and second-tier operators seeking scale.

- Greater use of contingent liabilities (i.e. guarantees) to attract hotel franchisees.

- Growth in alternative lodging accommodation providers (i.e. Airbnb, Inc.).

Stephen Boyd, CFA, Senior Director “Expect more of the same during 2018 — steady, but uninspiring, low-single-digit RevPAR growth driven entirely by rate increases. Demand could surprise to the upside if improved business sentiment and spending reinvigorates corporate travel.”

Stephen Boyd, CFA, Senior Director “Expect more of the same during 2018 — steady, but uninspiring, low-single-digit RevPAR growth driven entirely by rate increases. Demand could surprise to the upside if improved business sentiment and spending reinvigorates corporate travel.”

Sector Forecast

Leverage Trend: Falling U.S. lodging sector leverage will be stable to down slightly through 2019. Larger brand operators, such as Marriott and more recently Hilton Worldwide Holdings Inc., will adjust share repurchases accordingly to sustain policy leverage levels. Select smaller, speculative-grade lodging C-Corps will continue to reduce leverage through debt repayments and EBITDA growth. Hotel REIT leverage could fall further as issuers adopt and maintain countercyclical postures. M&A event risk is a key wildcard that could boost leverage profiles for the companies involved.

Cash Flow Generation: Neutral Low- to mid-single-digit RevPAR growth during 2018 will temper cash flow growth. Most lodging C-Corps have capital-light business models, primarily generating income from recurring hotel management and franchise fees, and to a lesser extent brand license revenues. New unit openings are another source of cash flow growth that should support mid-single-digit operator cash flow growth. Hotel REITs generally need 2%–3% RevPAR growth to hold cash flows constant. This assumes expense growth is held to 3%–4%, which is optimistic given recent trends in labor costs, property taxes and insurance premiums.

Liquidity Position: Adequate U.S. lodging companies generally have healthy liquidity profiles, underpinned by strong FCF (before share repurchases), undrawn revolver capacity and modest debt maturities during the next one to two years. Higher-rated hotel REITs maintain contingent liquidity via their pool of unencumbered hotels.

Potential Disruption to Sector: Alternative Accommodations (i.e. Airbnb) Airbnb is a meaningful, but manageable competitive threat to hotels, particularly around select large, leisure-oriented group events, despite differences in hotel service and amenity levels and fire/life/safety concerns and ongoing regulatory challenges. Airbnb listings increase effective lodging supply and act as a release valve for compression nights — periods of high occupancy where hotels enjoy strong pricing power. Airbnb could exacerbate lodging industry downturns if listings are likely to spike during recessions, as weak labor markets prompt some individuals to find alternative income sources. Some Airbnb stays represent incremental lodging demand, and staying in someone else’s home will not appeal to all travelers. But it is a viable alternative, particularly for budget leisure travelers. Business travelers are less likely to use Airbnb due to consistency issues and safety concerns.

Sector Fundamentals

Expect Low-Single-Digit RevPAR Growth Fitch expects U.S. RevPAR to be flat to up 2% during 2018, mostly due to ADR growth. Global operators may benefit from stronger (~3%–5%) RevPAR growth in select (primarily European and Asian) international markets. Full-service hotels will outperform select service due to lower supply growth. Leisure demand will show the greatest relative strength, followed by association and corporate group business. Corporate transient demand will trail, based on flat occupancy and 1%–2% growth in corporate negotiated rates. Government per diems (5% of industry demand) are up 3%–4% next year. Industry supply growth is manageable, near its 2% average, but RevPAR will remain under pressure in oversupplied markets, such as New York City.

Corporate Demand Remains the Wildcard Fitch expects corporate transient demand — the highest-rated and most-profitable business for many hotels — to trail the industry average growth rate during 2018. Corporate transient demand has historically correlated to the private nonresidential fixed investment (PNFI) subcomponent of U.S. GDP. Corporate transient demand has unexpectedly (and inexplicably) deviated from its traditional positive correlation to PNFI in recent years. However, positive signals from U.S. equity prices, business confidence and spending surveys and consensus PNFI estimates suggest upside risk for corporate transient demand next year.

Winners Defined by Size and Scale U.S. hotel franchisees and owners are showing a clear preference for aligning with the largest brands that have the largest customer loyalty reward systems. Marriott-branded rooms comprised 27.9% of the U.S. hotel development pipeline at Oct. 31, 2017, according to STR Global. This is well above the company’s 14.8% share of existing U.S. room supply. Comparable measures for Hilton, the industry’s second-largest player, were 23.9% and 12.0%.

Elevated Event Risk for Smaller Issuers Smaller hotel brand owners and operators are flexing their balance sheets to support room system growth and remain competitive amid industry consolidation and increasing competition from alternative accommodation providers. This could weaken the credit profiles of smaller lodging C-Corp issuers by increasing leverage and adding more volatile owned and leased assets and contingent obligations in the form of off-balance-sheet performance and loan guarantees. Fitch expects additional lodging C-Corp consolidation as companies seek to add scale and brand diversity to compete with Marriott and Hilton.