By Heidi Nielsen, McKenna Luke, and Kirby D. Payne

Foreign Direct Investment in U.S. enterprises has doubled over the past 15 years, a sign of investor confidence in American real estate, including hotels. The NATHIC event also spoke to what moves will set hoteliers ahead in the current market.

Foreign Direct Investment

Money for hotel development and transactions in the U.S., Mexico, and Canada is coming increasingly from overseas. Foreign Direct Investment (FDI), generally defined as an investment entity’s controlling interest in an asset in another country, was the focus of this year’s North American Tourism & Hospitality Investment Conference (NATHIC), held November 4 to 6 at the Fontainebleau Hotel & Resort in Miami Beach. The keynote by Barry Johnson, Chair of the Global FDI Association and Founding Executive Director of SelectUSA, put FDI in perspective for the future of the U.S. hotel industry. FDI “stock” (a measure of FDI, not an actual stock or share), increased from $2.78 million in 2000 to over $5.4 billion in 2014. The reasons range from mitigating risk through investment in the relatively rock-solid U.S. real estate market to supporting global expansions of hotel portfolios. In 2014, however, China outpaced the U.S. in terms of FDI annual inflow for the first time, and Brazil and Singapore emerged as new countries leading FDI investment. NATHIC made it clear that U.S. hotel stakeholders have good reason to stay on top of these trends, as a large portion FDI stock and inflows are invested in the lodging sector.

Money for hotel development and transactions in the U.S., Mexico, and Canada is coming increasingly from overseas. Foreign Direct Investment (FDI), generally defined as an investment entity’s controlling interest in an asset in another country, was the focus of this year’s North American Tourism & Hospitality Investment Conference (NATHIC), held November 4 to 6 at the Fontainebleau Hotel & Resort in Miami Beach. The keynote by Barry Johnson, Chair of the Global FDI Association and Founding Executive Director of SelectUSA, put FDI in perspective for the future of the U.S. hotel industry. FDI “stock” (a measure of FDI, not an actual stock or share), increased from $2.78 million in 2000 to over $5.4 billion in 2014. The reasons range from mitigating risk through investment in the relatively rock-solid U.S. real estate market to supporting global expansions of hotel portfolios. In 2014, however, China outpaced the U.S. in terms of FDI annual inflow for the first time, and Brazil and Singapore emerged as new countries leading FDI investment. NATHIC made it clear that U.S. hotel stakeholders have good reason to stay on top of these trends, as a large portion FDI stock and inflows are invested in the lodging sector.

EB-5 financing, a business investment and immigration program offered by the U.S. government to draw foreign investment for job creation, was a hot-topic discussion at the conference. Although EB-5 may have a reputation as “financing of last resort,” it has found a niche in the hospitality industry due to the number of onsite jobs hotel developments create. Furthermore, EB-5 financing was touted as a cheap source of capital or a bridge to a permanent loan. On the other hand, the long lead time of 12 to 14 months for approval and the holding period of 5 to 7 years can be discouraging for potential equity partners. Additionally, the political and legislative risks associated with this financing method worry some investors. Nevertheless, EB-5 financing is gaining momentum in primary markets for ground-up hotel construction, especially as market participants gain a better understanding of its benefits and potential drawbacks.

Buy, Build, or Sell?

Questions of whether to buy, build, or sell in the current market were posed in fairly concrete terms to conference panelists. Would you sell or hold a full-service hotel with a $4-million bottom line? In which hotel markets do you advise investing $50 million (with the expectation of reaping ROI on par with that over the last three years)? The consensus advice was to study and compare detailed market trends. Investors should consider selling their hotels located in mature markets (one not expected to realize significant growth in population, jobs, and leisure travel), according to Gerry Chase of New Castle Hotels & Resorts. To those interested in new construction, panelists recommended looking outside of the primary markets—essentially to places where demand has yet to peak and that have time left in the current cycle to allow a new property owner to reap the rewards. The high construction costs, longer timelines due to limited construction crews, and the fact that many markets are near the peak were among factors that many panelists considered discouraging for developers of new hotels.

For hotel buyers, the costs of property improvement plans (PIPs) can be a burden. The newly announced prototypes, such as Formula Blue for Holiday Inn Express and the Forever Young Initiative (FYI) for Hampton Inn & Suites, come with a price tag reported to be $20,000 to $30,000 a key. Furthermore, the traditional 4.0% reserve for replacement may not be enough to cover costs of required renovations, leaving many hotels undercapitalized. Panelists noted that the enforcement and costs of increasingly expensive brand standards can be a strong disrupter for deals.

For hotel buyers, the costs of property improvement plans (PIPs) can be a burden. The newly announced prototypes, such as Formula Blue for Holiday Inn Express and the Forever Young Initiative (FYI) for Hampton Inn & Suites, come with a price tag reported to be $20,000 to $30,000 a key. Furthermore, the traditional 4.0% reserve for replacement may not be enough to cover costs of required renovations, leaving many hotels undercapitalized. Panelists noted that the enforcement and costs of increasingly expensive brand standards can be a strong disrupter for deals.

Encouragingly, there are several beacons of opportunity in the current market. Incentive travel, tourism, and group demand are all on the rise. Under-performing properties, historic redevelopments, and select-service hotels in secondary markets were all marked as strong routes to investment. Furthermore, Ravi Patel of Hawkeye Hotels suggested refinancing no matter what to take advantage of lower interest rates.

The Brand Factor

As challengers in the form of independent hotels and services like Airbnb continue to gain ground in the U.S. lodging market, more hoteliers have begun to question the value of operating under the banner of a major hotel brand. When a panel of four experts at NATHIC were asked which brand they would build, two chose the limited-service Hampton Inn, one the limited-service Residence Inn by Marriott, and the last the select-service Hyatt Place. In a debate over the virtues of branded versus independent hotels, a widely recognized brand seems essential when building in a secondary or tertiary market. However, independent lifestyle and boutique hotels built in prime locations can have an advantage in an urban market, where high visibility and demand help boost occupancy and rate potential.

Despite the popularity of the boutique and lifestyle hotels, lenders are concerned about how they will perform during a down cycle. Lenders prefer brand representation as a measure of confidence, as established brands have a record of performance history investors can rely on when projecting future performance; these hotels have the brand loyalty factor to fall back on. With so many new brands coming out yearly under the flags of Marriott, Hilton, Best Western, and other major chains, hoteliers shared concern about making sure a brand is well matched to a market.

Current Trends

Millennials are on everyone’s mind, but are they really changing the hotel landscape? There is currently a divide between generations of hotel customers, according to panelists. While the Baby Boomers are very brand loyal, Millennials tend to be more “brand agnostic.” The exponential advance of new brands reflects the reality that hotel guests are no longer tied to a single brand. It’s not just Millennials, either. Research shows that a more widespread set of travelers is seeking a more unique lodging experience at a better value. Enter Airbnb.

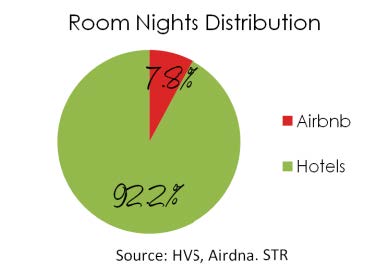

According to Leland Pillsbury, Chairman of Thayer Lodging Group, there were 20,000 rooms booked via Airbnb during the Pope’s visit to New York. He also noted that 6% of Airbnb travel is booked by corporate users. Kirby Payne, President of HVS Hotel Management and Asset Management – Newport, ended the conference on a presentation on the impact of Airbnb, noting that an estimated 7.81% of New York bookings in 2015 were through the service; furthermore, there has been a loss in jobs on the managerial level, as well as the line level at hotels. According to Mr. Payne’s presentation, Airbnb is expected to continue ramping up, with an estimated 21.3% increase in revenue growth forecast between 2015 and 2018. The material in Mr. Payne’s presentation was prepared for the Hotel Association of New York City by HVS.

According to Leland Pillsbury, Chairman of Thayer Lodging Group, there were 20,000 rooms booked via Airbnb during the Pope’s visit to New York. He also noted that 6% of Airbnb travel is booked by corporate users. Kirby Payne, President of HVS Hotel Management and Asset Management – Newport, ended the conference on a presentation on the impact of Airbnb, noting that an estimated 7.81% of New York bookings in 2015 were through the service; furthermore, there has been a loss in jobs on the managerial level, as well as the line level at hotels. According to Mr. Payne’s presentation, Airbnb is expected to continue ramping up, with an estimated 21.3% increase in revenue growth forecast between 2015 and 2018. The material in Mr. Payne’s presentation was prepared for the Hotel Association of New York City by HVS.

Another aspect of the sharing economy emerging in the industry is crowdfunding, a new trend in hotel investing. While crowdfunding is difficult and more time consuming when it comes to hotels, it has offered investors some luxury perks. As more companies look toward this option, crowdfunding is expected to gain momentum over the next several years.

Conclusion

While the NATHIC event focused on the significant amount of foreign investment in North America, it also spoke to new development projects and current trends. Developers and investors need to look at the dynamics of each market individually. While the trends are changing and technology is advancing, hoteliers need to find a balance between the “old school” versus “new school” approach to capturing demand, establishing rates, designing hotels, and choosing whether to buy, build, or sell. There are a lot of deals to be made and a significant amount of new supply in the pipeline, but as construction costs continue to increase, the lending on these deals will be limited. More than ever, well-positioned hotel projects, with the data and analysis to back up projections on value and performance, will stand out.

Excellent “Whitepapers” have been written regarding the investment climate of the three countries that make up North America, with materials sourced from HVS and its associates.

- Download White Paper on USA Tourism Investment Climate

- Download White Paper on Canada Tourism Investment Climate

- Download White Paper on Mexico Tourism Investment Climate

HVS Asset Management – Newport and HVS Hotel Management have been strategic partners of NATHIC with Questex since its inception. NATHIC is one of the HVS Global Conferences (HVS Conferences) and is also part of the International Hotel Investment Forum Event Series (Berlin and others). It is a hospitality investment conference for those interested in investing in North America. Among those already registered are attendees from Latin America (including Mexico), China (including a major company looking for U.S. investment opportunities), and various other countries besides the U.S. and Canada.