by Jack Corgel, Ph.D.

A frequently asked question of us at CBRE Hotels’ Americas Research is, “When will the current up-cycle end?” Some inquisitive types go so far as to ask, “How will it end?” At the “end” of the past two up-cycle phases, the peak rapidly dropped into a deep trough precipitated by tragic and disruptive shocks (i.e., 9/11, financial crisis) that made people hesitant to travel. In the absence of catastrophic events, hotel demand usually falls victim to the natural death of the up-cycle. After all, as I have heard some exclaim, this current expansion phase has lasted more than 27 quarters (i.e., Q3 2009 – Q2 2016), so it is likely that a recession is near given that certain past up-cycles were either shorter (i.e., Q1 1975 – Q1 1980) or slightly longer than this recovery (i.e., Q4 1982 – Q3 1990).

Another down-cycle might occur as the result of overbuilding, spreading hotel demand thinly enough to cause financial distress and all the unpleasantness that goes along with it. But in this article, I provide three reasons for believing that excessive supply growth is unlikely to produce financial distress in most hotel markets across the U.S. From my current vantage point, a Goldilocks supply scenario is likely to take place over next few years in most cities: not too many and not too few hotel rooms created.

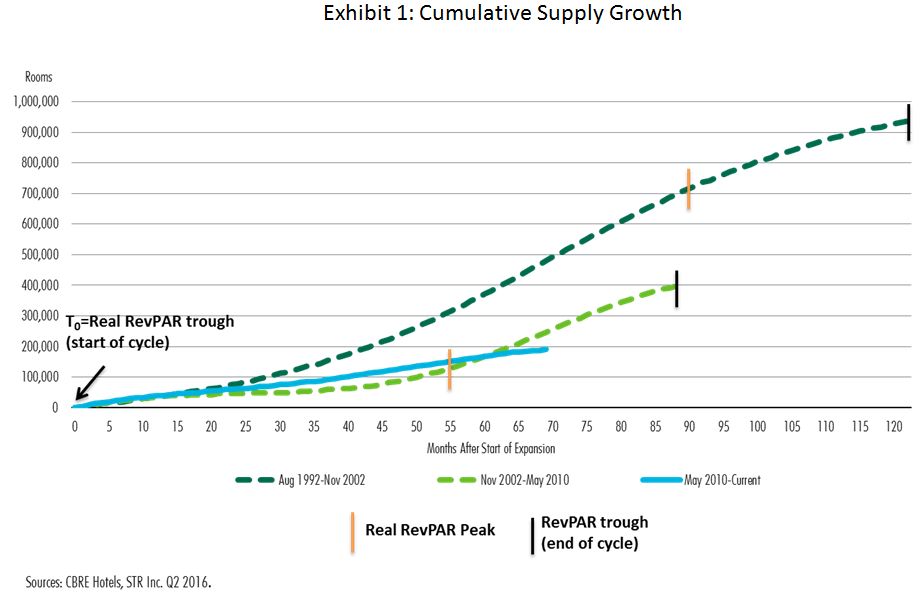

1: Construction Got a Late Start The cash flows from hotels carry the greatest risk relative to other forms of commercial real estate, and construction loans for commercial properties create the most loss potential for lenders. Hence, coming out of our most recent recession, lowlighted by a historically significant banking crisis, it is not surprising that hotel construction projects languished in recent years even in the face of resurgent demand. Exhibit 1 shows supply additions during RevPAR troughs for three recovery periods during the past two decades, including the current cyclical up-phase. Construction was sluggish during the first two years of all three recoveries, but began accelerating by the fourth and sixth years during the 1992-2002 and 2002-2010 recoveries, respectively.  Now, six years since the last trough, only about 200,000 rooms have been added to the U.S. inventory, representing roughly a one-half percent cumulative change. This total is approximately 50,000 rooms less than at the same time during the 2002-2010 recovery and nearly 250,000 rooms less than at the same time during the 1992-2002 recovery. Moreover, during both earlier recoveries, the pace of supply growth quickened after the sixth year to 3% or greater. Our forecasts call for U.S. hotel supply growth to peak at 2.5% (2018) during the current recovery. 2: Frictions Inhibiting future hotel supply growth are two significant frictions—stricter banking regulations and persistently high construction costs. During the first half of 2015, bank regulators (i.e., OCC, FDIC and FRB) introduced a requirement that banks making loans for High Volatility Commercial Real Estate (HVCRE) would need to set aside additional capital that could amount to 150% of that required for other types of lending. Construction loans for income-producing real estate, in which the developer contributes less than 15% of the value, are the main target of the HVCRE regulation. As Bill Tryon of Partner Engineering and Science, Inc. (see references below) points out, “Some lenders are expected to pass this cost along to borrowers, while others may simply focus on more profitable transactions.” These regulations stimulated interest in hotel construction lending by non-bank lenders, however the entry of these firms has not made a sizeable impact. Hotel developers able to meet HVCRE standards or secure debt financing from non-banks were rewarded with low-interest costs. Yet other recovery period construction-related costs remained elevated and continue to increase. CBRE researchers Andrea Cross and Taylor Jacoby (see references below and researchgateway.cbre.com) chronicle the reasons why construction costs have remained high despite the global collapse of commodity prices and single-family homebuilder retrenchment. The findings from this study indicate that increases in construction labor costs have overwritten gains from lower commodity prices, and that multifamily housing construction partially replaced single-family construction as a prime consumer of construction inputs. 3: No Booster Rockets Before most bloggers were born, the Internal Revenue Code allowed commercial real estate investors to depreciate investment in land improvements over a 15-year period, resulting in a straight-line rate of 6.67%. The economic depreciation rate has been estimated in academic studies to lie between 1.5% and 2.0%. By the time Congress dumped water on this fire, construction was surging about as fast as the empty rental spaces and hotel rooms. Overbuilding next occurred in the roaring 2000s with a finance-driven boom in single-family homebuilding. Fingers are still being pointed as to who was responsible, but Government-Sponsored Enterprises (GSEs) certainly played a role. The EB5 program is the only booster rocket from Washington that could affect a hotel building spike. A 2016 Morningstar (see references below) report cites EB5 as one of the main causes for the ballooning supply of hotel rooms in New York during recent years. But the limitations of this program will almost certainly result in EB5 resembling a kid’s water-pressure-propelled rocket rather than an Elon Musk SpaceX design for launching a wave of non-economic hotel development projects. Goldilocks, We Love You! During the modern age of the U.S. hotel market, presumably since STR began reporting detailed monthly data in the late 1980s, there have been periods when too few, too many and just the right number of hotel rooms were added to the market in line with the populist concept known as the Goldilocks Principle. The social costs of too much construction were incurred twice during the past few decades as described above. During the current cyclical phase, the inability of traditional hotel supply growth to keep pace with persistent demand growth created opportunity for disruptors equipped with online platforms to impose private costs on hotel owners and managers. Hence, there is a peaceful harmony associated with the movement toward balance in the number of rooms available and occupied. Our Hotel Horizons® forecasts portend such a balance. During the next two years, supply growth is expected to moderately exceed demand growth in the U.S. hotel market. With occupancies currently running above long-run average, this run-up of supply should bring hotel markets into balance later this decade. Tranquility will reign as long as the bears don’t return home any time soon. References Cross, A. and T. Jacoby. "Why are Construction Costs Rising?” Viewpoint: U.S. Office, CBRE Research, May 2016. Tryon, B. "Five Words Developers Dread: High Volatility Commercial Real Estate.” National Real Estate Investor, August 2015. Snow, B., C. Costich, and E. Dittmer. Ballooning Supply Looms Over $3.68 Billion in CMBS Backed by Manhattan Hotels. Morningstar CMBS Research, May, 2016.

Now, six years since the last trough, only about 200,000 rooms have been added to the U.S. inventory, representing roughly a one-half percent cumulative change. This total is approximately 50,000 rooms less than at the same time during the 2002-2010 recovery and nearly 250,000 rooms less than at the same time during the 1992-2002 recovery. Moreover, during both earlier recoveries, the pace of supply growth quickened after the sixth year to 3% or greater. Our forecasts call for U.S. hotel supply growth to peak at 2.5% (2018) during the current recovery. 2: Frictions Inhibiting future hotel supply growth are two significant frictions—stricter banking regulations and persistently high construction costs. During the first half of 2015, bank regulators (i.e., OCC, FDIC and FRB) introduced a requirement that banks making loans for High Volatility Commercial Real Estate (HVCRE) would need to set aside additional capital that could amount to 150% of that required for other types of lending. Construction loans for income-producing real estate, in which the developer contributes less than 15% of the value, are the main target of the HVCRE regulation. As Bill Tryon of Partner Engineering and Science, Inc. (see references below) points out, “Some lenders are expected to pass this cost along to borrowers, while others may simply focus on more profitable transactions.” These regulations stimulated interest in hotel construction lending by non-bank lenders, however the entry of these firms has not made a sizeable impact. Hotel developers able to meet HVCRE standards or secure debt financing from non-banks were rewarded with low-interest costs. Yet other recovery period construction-related costs remained elevated and continue to increase. CBRE researchers Andrea Cross and Taylor Jacoby (see references below and researchgateway.cbre.com) chronicle the reasons why construction costs have remained high despite the global collapse of commodity prices and single-family homebuilder retrenchment. The findings from this study indicate that increases in construction labor costs have overwritten gains from lower commodity prices, and that multifamily housing construction partially replaced single-family construction as a prime consumer of construction inputs. 3: No Booster Rockets Before most bloggers were born, the Internal Revenue Code allowed commercial real estate investors to depreciate investment in land improvements over a 15-year period, resulting in a straight-line rate of 6.67%. The economic depreciation rate has been estimated in academic studies to lie between 1.5% and 2.0%. By the time Congress dumped water on this fire, construction was surging about as fast as the empty rental spaces and hotel rooms. Overbuilding next occurred in the roaring 2000s with a finance-driven boom in single-family homebuilding. Fingers are still being pointed as to who was responsible, but Government-Sponsored Enterprises (GSEs) certainly played a role. The EB5 program is the only booster rocket from Washington that could affect a hotel building spike. A 2016 Morningstar (see references below) report cites EB5 as one of the main causes for the ballooning supply of hotel rooms in New York during recent years. But the limitations of this program will almost certainly result in EB5 resembling a kid’s water-pressure-propelled rocket rather than an Elon Musk SpaceX design for launching a wave of non-economic hotel development projects. Goldilocks, We Love You! During the modern age of the U.S. hotel market, presumably since STR began reporting detailed monthly data in the late 1980s, there have been periods when too few, too many and just the right number of hotel rooms were added to the market in line with the populist concept known as the Goldilocks Principle. The social costs of too much construction were incurred twice during the past few decades as described above. During the current cyclical phase, the inability of traditional hotel supply growth to keep pace with persistent demand growth created opportunity for disruptors equipped with online platforms to impose private costs on hotel owners and managers. Hence, there is a peaceful harmony associated with the movement toward balance in the number of rooms available and occupied. Our Hotel Horizons® forecasts portend such a balance. During the next two years, supply growth is expected to moderately exceed demand growth in the U.S. hotel market. With occupancies currently running above long-run average, this run-up of supply should bring hotel markets into balance later this decade. Tranquility will reign as long as the bears don’t return home any time soon. References Cross, A. and T. Jacoby. "Why are Construction Costs Rising?” Viewpoint: U.S. Office, CBRE Research, May 2016. Tryon, B. "Five Words Developers Dread: High Volatility Commercial Real Estate.” National Real Estate Investor, August 2015. Snow, B., C. Costich, and E. Dittmer. Ballooning Supply Looms Over $3.68 Billion in CMBS Backed by Manhattan Hotels. Morningstar CMBS Research, May, 2016.