As 2023 draws to a close, regional HVS leaders across the globe take a look back at how the global hotel industry fared this year and opine on the outlook for next year. While the U.S. experienced muted 2023 RevPAR growth relative to 2022 gains, most other global markets recorded extraordinary RevPAR growth, well above 10%, primarily fueled by strong ADR gains. While transaction activity cooled across the Americas and Europe, the Asia Pacific saw a significant strengthening as this region’s markets moved beyond pandemic-era restrictions.

United States

By Rod Clough, President – Americas

As 2023 ends, we look back on a year where hotel performance held steady, with occupancy closing out the year near 63% (vs. 66% in 2019) and ADR rising just under 5% to roughly $155 USD. Group room nights continued to show substantial growth, helping fill the gap left by some pullback in the domestic leisure segment. While hotel operations were going strong, a different story played out in the transactions market, as the sector experienced a low not seen since 2020. The federal funds rate started 2022 at less than 1% and, by late summer of 2023, topped out at 5.25% to 5.5%; moreover, bank failures early in the year sent shockwaves through the investment community. These factors not only cooled the transactions market but sent an Arctic blast through it. As a result, transaction volume during the year declined by roughly 35% from 2022 levels.

As 2023 ends, we look back on a year where hotel performance held steady, with occupancy closing out the year near 63% (vs. 66% in 2019) and ADR rising just under 5% to roughly $155 USD. Group room nights continued to show substantial growth, helping fill the gap left by some pullback in the domestic leisure segment. While hotel operations were going strong, a different story played out in the transactions market, as the sector experienced a low not seen since 2020. The federal funds rate started 2022 at less than 1% and, by late summer of 2023, topped out at 5.25% to 5.5%; moreover, bank failures early in the year sent shockwaves through the investment community. These factors not only cooled the transactions market but sent an Arctic blast through it. As a result, transaction volume during the year declined by roughly 35% from 2022 levels.

Looking forward to 2024, we expect the year to have a slow start but then gradually accelerate, ultimately landing with a much stronger finish. The U.S. may in fact avoid a recession, with very slow growth in the first two quarters followed by more significant economic growth in the third and fourth. We expect RevPAR to increase in 2024, albeit at a lower rate than that experienced in 2023. We may see a rate cut by the Fed by the summer if the anemic economic growth pattern predicted by many economists takes hold in the first half of the year. The cut may help fuel an additional layer of transaction activity in the hotel industry and other real estate sectors.

More sellers are likely to bring hotels to market in 2024 as debt maturities are reached, PIP delays are exhausted, unavoidable defaults occur, or, conversely, successful post-pandemic business plans are completed. In the case of the latter, owners may become ready to sell high-cash-flowing hotels in order to move onto other opportunities at this point in the cycle. Now is certainly the time to buy. With fewer buyers in the market and financing more difficult to come by, hotels are receiving fewer offers. This less-frenzied environment leads to more normalcy in transacting and a higher likelihood that parties can get to a successful closing that not only satisfies the seller but also leaves the buyer in a position to implement a business plan for real value growth. The cost of debt may be high and may require heightened due diligence, but a refinance down the road coupled with an eventual sale after the implementation of that business plan (selling at a time when cost of debt will likely be lower than today) would likely lead to very favorable returns. We expect a more active year of transactions ahead and a relatively stable hotel operating environment.

Caribbean

By Kristina D’Amico, Managing Director – Caribbean Region

In 2023, the Caribbean has reached an all-time high in the major hotel performance metrics: occupancy, ADR, and RevPAR. RevPAR for most islands experienced double-digit growth when compared to 2019, driven by exponential ADR growth. Air passengers and cruise arrivals are on pace to exceed 2019 levels. While the majority of travelers are still visiting the Dominican Republic, Jamaica, Puerto Rico, and the Bahamas, an increase of airlift and new airlines in the region have allowed for more visitation to some of the smaller islands. In addition to the record performance metrics, there is less demand seasonality than ever before, with previously off-season months now displaying higher than typical occupancy levels. The region also benefited from minimal hurricane disruption during 2023, positively affecting the annual performance.

In 2023, the Caribbean has reached an all-time high in the major hotel performance metrics: occupancy, ADR, and RevPAR. RevPAR for most islands experienced double-digit growth when compared to 2019, driven by exponential ADR growth. Air passengers and cruise arrivals are on pace to exceed 2019 levels. While the majority of travelers are still visiting the Dominican Republic, Jamaica, Puerto Rico, and the Bahamas, an increase of airlift and new airlines in the region have allowed for more visitation to some of the smaller islands. In addition to the record performance metrics, there is less demand seasonality than ever before, with previously off-season months now displaying higher than typical occupancy levels. The region also benefited from minimal hurricane disruption during 2023, positively affecting the annual performance.

Going forward, despite the record performance metrics and visitation from both air and sea that will be achieved in 2023, the region still has its challenges to work through. Interest in new hotel and resort developments is prevalent as demand continues to outpace supply; however, developers are facing a challenging financing environment to get new projects off the ground and are having to be more creative with their capital stack. In addition, increased insurance costs have proven to be challenging for new development. However, despite these ongoing issues, the Caribbean continues to shine as new air routes continue to be added to the region and cruise ships continue to add new ports of entry. The outlook is favorable for additional ADR and demand growth in 2024, barring any natural disasters.

Canada

By Carrie Russell, Senior Managing Partner – Vancouver, and Monique Rosszell, Senior Managing Partner – Toronto and Montreal

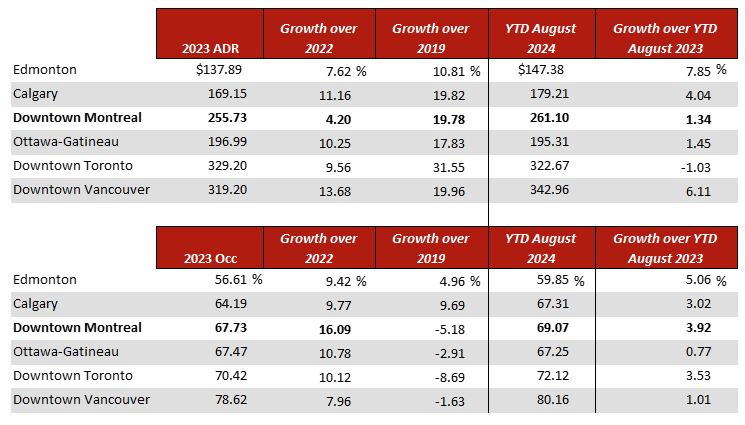

The year 2023 has set new benchmarks for the Canadian hotel industry. After reaching a RevPAR peak in 2022, the market RevPAR is on pace to grow another 15% in 2023, driven by strong growth in both occupancy and ADR. The leisure segment noted the benefit of increased transborder and international visitation, while the domestic market continues to provide a key base of demand. The major metropolitan areas, including Toronto, Montreal, and Vancouver, also drove a large portion of the gains in 2023 as a result of strong meeting and group demand, much of it pent up from prior-year cancellations. These major markets are also seeing an improvement in commercial/corporate demand, especially in the fall. While demand is not back to historical highs, the return of key corporate accounts is beneficial, as a decline in the domestic leisure market is possible given the softening economic conditions and expectation of a recession. Supply growth in Canada has been muted throughout COVID with soaring construction costs. A conservative lending environment and higher interest rates also helped suppress the pace of new development.

The year 2023 has set new benchmarks for the Canadian hotel industry. After reaching a RevPAR peak in 2022, the market RevPAR is on pace to grow another 15% in 2023, driven by strong growth in both occupancy and ADR. The leisure segment noted the benefit of increased transborder and international visitation, while the domestic market continues to provide a key base of demand. The major metropolitan areas, including Toronto, Montreal, and Vancouver, also drove a large portion of the gains in 2023 as a result of strong meeting and group demand, much of it pent up from prior-year cancellations. These major markets are also seeing an improvement in commercial/corporate demand, especially in the fall. While demand is not back to historical highs, the return of key corporate accounts is beneficial, as a decline in the domestic leisure market is possible given the softening economic conditions and expectation of a recession. Supply growth in Canada has been muted throughout COVID with soaring construction costs. A conservative lending environment and higher interest rates also helped suppress the pace of new development.

Transaction activity was strong in the first half of 2023, with some notable full-service trades in Toronto and Montreal; however, the pace of activity slowed in Q3. We expect that overall transaction volume will be $1.5 billion CAD for the year, which is slightly below 2022 and the forecasted $2.0 billion CAD in trades.

The outlook for 2024 is cautious. Economic forecasts for the country indicate minimal GDP growth, with an anticipated slowdown in the first half of the year. Inflation is expected to fall back to the target level of 2.5%, and while the interest rate outlook is still uncertain, interest rate hikes appear to have peaked. The interest rate has the potential to decrease modestly beginning in the late spring or early summer. This cloudy economic picture is likely to dampen the domestic leisure travel that has been a large contributor to the strength of the hotel industry in recent years. That said, growth is still anticipated in the inbound international travel segment. Meeting and group demand is stabilizing, with modest growth anticipated, while the commercial segment is expected to see an uptick given that it has not recovered to the same degree as other segments. As a result, we expect RevPAR growth in the range of 2.0% to 4.0%. Supply growth is expected to track at a similar pace to 2023. With the record-setting RevPAR figures in recent years, the tightening of short-term-rental restrictions, and the anticipation of interest rate declines, the pipeline for development is expanding. On the transaction side, several larger deals are expected to close early in 2024, which should result in a comparable volume to 2022 and 2023.

Mexico

By Richard Katzman, Senior Managing Partner – LATAM, and Lorea Arnoldi, Vice President

Mexico’s lodging industry combines robust business and leisure-oriented sectors, along with extensive international and national brand footprints. Indeed, additional brands continue to express interest in growing their pipelines across the country both in resort and urban destinations. Mexico’s economy and hotel industry are structurally and fundamentally sound. However, the 2023 macroeconomic environment faced complex challenges, including high inflation and interest rates, currency fluctuations against the U.S. dollar, and, in certain regions, security concerns. During 2024, presidential and local elections will add another layer of uncertainty.

Mexico’s lodging industry combines robust business and leisure-oriented sectors, along with extensive international and national brand footprints. Indeed, additional brands continue to express interest in growing their pipelines across the country both in resort and urban destinations. Mexico’s economy and hotel industry are structurally and fundamentally sound. However, the 2023 macroeconomic environment faced complex challenges, including high inflation and interest rates, currency fluctuations against the U.S. dollar, and, in certain regions, security concerns. During 2024, presidential and local elections will add another layer of uncertainty.

During the last three decades, the country has experienced a transition from heavy dependency on oil exports to a focus on export manufacturing. Foreign trade has been the underpinning of Mexico’s economic stability in today’s USMCA era (post-NAFTA). In a post-pandemic environment, after the recurring tension of China–U.S. relations, nearshoring opportunities have been a motor for economic growth in states near the U.S. border and in central Mexico. Hotels in industrial cities have been able to increase occupancy and push average rates, with some evaluating PIPs. However, the anticipated favorable impact of demand growth associated with nearshoring is still in its early stages, and the development pipeline in these cities remains limited. A more gradual recovery has been observed in major cities such as Mexico City, Guadalajara, and Monterrey. Demand in 2023 is below the 2019 level; however, average rate has experienced a healthy recovery. Business and group demand both continue to grow; however, the leisure segment has experienced the greatest increase, particularly in Mexico City. The outlook remains favorable given the macroeconomic environment, tempered to some degree by 2024 electoral influences.

Mexican resort destinations such as Cancun-Riviera Maya, Los Cabos, and Puerto Vallarta-Riviera Nayarit have experienced strong occupancy and average rate increases in the past years, a trend that surged during the COVID-19 pandemic. However, demand and rate growth slowed during the summer of 2023. Smaller up-and-coming resort destinations have also benefited from this demand growth, and some will continue to evolve toward consolidation in the years to come, including La Paz, Mazatlán, and the Huatulco-Puerto Escondido corridor. Over the past 15 years, Mexico’s resort industry allowed for steady growth both in the variety of product developed (including traditional European plan and all-inclusive hotels) and in demand levels that have accompanied this market expansion. The industry remains well positioned for future positive performance across locations and market segments, including resort residential. Still, challenges persist in some markets, such as the need for more thorough regional planning, infrastructure improvements, zoning, tourism promotion, and security.

South America

By Richard Katzman, Senior Managing Partner – LATAM, and Fernanda L’Hopital, Vice President

After several economic and political disruptions, South American hotel markets began a period of recovery in 2022 that strengthened in 2023. The main drivers included the return of meeting and group travel (surpassing levels achieved in 2019 in several cases), the increase in commercial demand (although remaining below the 2019 levels in most of the markets), and the return of international travel. In markets like Buenos Aires and São Paulo, stronger demand allowed for average daily rate increases in 2023. Other markets, like Lima, Santiago, and Bogotá, that experienced significant growth in supply in recent years also managed to increase their occupancy and rates, but at a more moderate pace. Leisure destinations achieved sound occupancy levels, mainly driven by the return of international travelers and robust domestic and regional demand, which has been favored by currency devaluations in many countries. Across South America, the investment climate remains challenging, with high inflation, limited debt, and a small pool of investors. As such, increases in inventory and the project pipeline have been limited since the start of the COVID-19 pandemic. More recently, local and regional development groups have begun to review potential opportunities.

After several economic and political disruptions, South American hotel markets began a period of recovery in 2022 that strengthened in 2023. The main drivers included the return of meeting and group travel (surpassing levels achieved in 2019 in several cases), the increase in commercial demand (although remaining below the 2019 levels in most of the markets), and the return of international travel. In markets like Buenos Aires and São Paulo, stronger demand allowed for average daily rate increases in 2023. Other markets, like Lima, Santiago, and Bogotá, that experienced significant growth in supply in recent years also managed to increase their occupancy and rates, but at a more moderate pace. Leisure destinations achieved sound occupancy levels, mainly driven by the return of international travelers and robust domestic and regional demand, which has been favored by currency devaluations in many countries. Across South America, the investment climate remains challenging, with high inflation, limited debt, and a small pool of investors. As such, increases in inventory and the project pipeline have been limited since the start of the COVID-19 pandemic. More recently, local and regional development groups have begun to review potential opportunities.

For 2024, the outlook for the larger economies in the region is generally favorable, with the exception of Argentina. Considerable uncertainty is anticipated for this country following a prolonged economic crisis and the recent presidential election that is expected to bring considerable change. In general, economic growth is projected for the region, together with decreases in inflation and interest rates. Local currencies are expected to remain relatively stable. This improvement in economic and investment conditions, together with solid hotel performance results, is anticipated to support a more active development pipeline.

Significant potential remains in the Brazil, Colombia, northern Peru, and Ecuador resort markets, where there are ample opportunities for leisure-oriented developments, from standalone European plan and all-inclusive properties to master-planned developments. Leisure-oriented products associated with natural resources, wellness, lifestyle, and culture also represent an attractive opportunity. In regard to business travel, there are select opportunities for hotel brands to increase their footprints. Countries like Brazil, Argentina, Colombia, Chile, and Peru have several secondary and tertiary cities that are underserved by quality hotel supply. Countries like Ecuador, Uruguay, Bolivia, and Paraguay also present development opportunities on a select basis.

Northern Europe

By Charles Human, President – Europe, and Sophie Perret, Managing Director

In 2023, continued strong RevPAR growth has been met with pressure on operating expenses and higher interest rates, with the latter particularly having a dampening effect on values and transaction activity. Through October, multiple markets (such as Paris, Rome, Brussels, Barcelona, and Bucharest) have seen more than 15% average rate growth this year compared to 2022, and even more markets have recorded more than 25% RevPAR growth. The most growth occurred in Amsterdam, Brussels, Milan, Prague, and Rome. Elsewhere, average rate increases have already started to soften, and we anticipate only modest growth in 2024. Counterbalancing this trend, cost inflation is expected to ease, although utility prices may remain volatile given the current conflict in the Middle East.

In 2023, continued strong RevPAR growth has been met with pressure on operating expenses and higher interest rates, with the latter particularly having a dampening effect on values and transaction activity. Through October, multiple markets (such as Paris, Rome, Brussels, Barcelona, and Bucharest) have seen more than 15% average rate growth this year compared to 2022, and even more markets have recorded more than 25% RevPAR growth. The most growth occurred in Amsterdam, Brussels, Milan, Prague, and Rome. Elsewhere, average rate increases have already started to soften, and we anticipate only modest growth in 2024. Counterbalancing this trend, cost inflation is expected to ease, although utility prices may remain volatile given the current conflict in the Middle East.

Transaction volume across Europe so far this year has totaled around €11 billion, down more than 30% when compared to last year and over 60% when compared to 2019 levels. Most acquisition activity has been focused on Spain and other Southern European markets, and there have been noticeably fewer large portfolio deals. Real estate funds have been hoping to capitalize on situations where debt needs to be refinanced, but to date, any signs of distress or even material reductions in pricing are rare.

Interest rates are widely thought to have peaked, with the hope that cuts may commence during 2024. These reductions are, however, likely to be relatively small, and interest rates will remain above previous ultra-low levels for some time. We expect transaction activity to pick up during 2024, partly as a result of an improving debt market, but also because there will be pressure to sell from owners facing difficulties refinancing over-leveraged situations and from multi-sector investors who are particularly exposed to the troubled office sector and need to create liquidity through hotel sales. A wave of distress is looking increasingly unlikely, however.

Southern Europe

By Ezio Poinelli, Senior Director – Southern Europe, and Demetris Spanos, Managing Director

Southern European countries have experienced a particularly positive year, with Spain, Greece, and Italy having almost or totally recovered to tourist-arrival levels experienced pre-pandemic, while Portugal is already more than 10% higher. ADR increases have been robust and, in some cases, outstanding (especially in the upper segments of the market), with ADR increases for southern European countries’ submarkets ranging from 20–40% over 2019 levels. As a result, hotels enjoyed growing margins and profitability. For Italy in particular, labor costs have not increased in line with the high inflation rate the country is experiencing.

Southern European countries have experienced a particularly positive year, with Spain, Greece, and Italy having almost or totally recovered to tourist-arrival levels experienced pre-pandemic, while Portugal is already more than 10% higher. ADR increases have been robust and, in some cases, outstanding (especially in the upper segments of the market), with ADR increases for southern European countries’ submarkets ranging from 20–40% over 2019 levels. As a result, hotels enjoyed growing margins and profitability. For Italy in particular, labor costs have not increased in line with the high inflation rate the country is experiencing.

Hotels are considered a more dynamic commercial asset class given that they are able to more quickly adjust their operating metrics to match the economic cycle. As a result, investors in this region are particularly keen to invest in this sector at this time. On the other side, increasing interest rates and tighter loan parameters imposed by lenders have led to a lower number of transactions than in 2022. Alternative lenders and full-equity investors are now more active in the southern European market.

Institutional investors and sovereign wealth funds continue to look at South Europe and the Mediterranean as a safe and promising place to invest, undertaking meaningful transactions of portfolios in Spain, luxury assets in Italy, and resorts in Greece. Noteworthy transactions include ADIA’s €1-billion hotel joint venture with Melia; GIC’s investment in a 35% stake in the HIP/Blackstone platform of resorts in the Mediterranean, following the acquisition of a 51% stake in Sani/IKOS resorts in 2022; PIF Saudi Arabia’s 49% investment in Rocco Forte’s hotel group; and Palace Hotels & Resorts’ 100% takeover of Baglioni Hotels & Resorts, among others. Moreover, brand penetration continues to grow, with branded hotel keys representing more than 60% of total supply in Spain, 50% in Portugal, 24% in Greece, and 18% in Italy.

The outlook for 2024 remains positive. Southern Europe is looking forward to the gradual return of the Chinese market, and U.S. demand appears to be solid and has replaced demand from Russia in many destinations. Thus, inbound demand is expected to grow, especially for resort destinations, while domestic demand could potentially face some issues. Business travel will probably continue to a full recovery, while the segment may experience a slight ADR correction in some destinations.

Repositioning or conversions of existing assets will continue, as they are less affected by the challenging lending environment and increasing construction costs. New (greenfield) developments are expected mainly in countries like Portugal, the Balkans, and the Greek islands, where governments have implemented favorable measures for sustainable developments. Conversely, repositionings and conversions will characterize the markets with higher barriers to entry and greater bureaucracy, like Italy, along with more mature markets, like Spain.

Refinancing needs, capital expenditure requirements due to the EU’s ESG policies, and generational changes could push some owners in markets largely dominated by family ownership to sell their assets, creating interesting opportunities for new investors. The gap between asking and bidding prices is also expected to gradually reduce.

Africa

By Hala Matar Choufany, President – HVS Middle East, Africa, and South Asia

As of September 2023, Africa’s hotel performance reveals a blend of positive growth and challenges, with diverse key performance indicators (KPIs) underscoring the dynamic nature of the hospitality industry on the continent. During the year, different regions in Africa exhibited varied trends in hotel performance. Highlighting regional disparities, some areas experienced significant growth and increased international arrivals, while others encountered ongoing challenges. Notably, popular destinations like Addis Ababa, Kigali, Cape Town, Nairobi, Lagos, and Sharm El Sheikh surpassed 2019 occupancy levels, signaling full recovery and sustained interest in accommodations.

As of September 2023, Africa’s hotel performance reveals a blend of positive growth and challenges, with diverse key performance indicators (KPIs) underscoring the dynamic nature of the hospitality industry on the continent. During the year, different regions in Africa exhibited varied trends in hotel performance. Highlighting regional disparities, some areas experienced significant growth and increased international arrivals, while others encountered ongoing challenges. Notably, popular destinations like Addis Ababa, Kigali, Cape Town, Nairobi, Lagos, and Sharm El Sheikh surpassed 2019 occupancy levels, signaling full recovery and sustained interest in accommodations.

The year-to-date (YTD) September 2023 consolidated occupancy for Africa reached 55%, compared to 57% for the same period in 2019. On the other hand, the YTD average rate for the continent improved by 35% from 2019 levels, reaching $139 USD. Morocco, Mauritius, Dakar, and Kampala boast higher rates than most cities, excluding the Seychelles, which commands a strong average rate. Additionally, certain emerging markets within Africa, such as Rwanda, Nairobi, and Morocco, exhibit promising growth in both hotel development and tourism-related activities.

Middle East

By Hala Matar Choufany, President – HVS Middle East, Africa, and South Asia

In 2023, the Middle East (especially the GCC countries) has shown robust growth in tourism and hotel performance, surpassing 2019 occupancy levels. The region leads in average rates, marking a 35% increase in YTD September 2023 compared to the same period in 2019. All cities in UAE and KSA as well as Muscat have experienced significant growth in accommodated room nights throughout 2023, supported by strong air connectivity and substantial government and private investments in the hospitality sector. Despite challenges like rising construction costs and higher interest rates, the UAE and KSA continue to prioritize tourism as a fundamental contributor to economic growth. The positive tourism indicators affirm the sustained expansion.

In 2023, the Middle East (especially the GCC countries) has shown robust growth in tourism and hotel performance, surpassing 2019 occupancy levels. The region leads in average rates, marking a 35% increase in YTD September 2023 compared to the same period in 2019. All cities in UAE and KSA as well as Muscat have experienced significant growth in accommodated room nights throughout 2023, supported by strong air connectivity and substantial government and private investments in the hospitality sector. Despite challenges like rising construction costs and higher interest rates, the UAE and KSA continue to prioritize tourism as a fundamental contributor to economic growth. The positive tourism indicators affirm the sustained expansion.

The UAE currently operates around 208,000 hotel rooms at a 70% occupancy rate, with plans to add 45,000 more rooms, suggesting an increase of 10 million accommodated room nights. In Saudi Arabia, substantial investment in tourism resulted in strong growth in 2022, with solid figures continuing through September 2023. However, the hotel development pipeline, comprising around 350 hotels (150,000 rooms), may face delays due to increased construction costs and higher interest rates. Doha and Kuwait are expected to grow the most slowly, while other markets in KSA and UAE are anticipated to benefit from rising demand, albeit with slower average rate growth.

India

By Mandeep Lamba, President – South Asia, and Dipti Mohan, Associate Vice President & Head of Research – South Asia

In 2023, India continued its ascent on the global stage, building on its status as the world’s fifth-largest economy that was achieved the previous year. The country seized the spotlight, surpassing China as the most populous country, hosting over 200 meetings during its G20 presidency, and achieving a historic milestone by successfully landing Chandrayaan-3 on the moon’s unexplored south pole, the first country ever to do so.

In 2023, India continued its ascent on the global stage, building on its status as the world’s fifth-largest economy that was achieved the previous year. The country seized the spotlight, surpassing China as the most populous country, hosting over 200 meetings during its G20 presidency, and achieving a historic milestone by successfully landing Chandrayaan-3 on the moon’s unexplored south pole, the first country ever to do so.

Moreover, fueled by favorable demographics, robust domestic demand, and increased investments, India’s economic resilience persisted amidst global challenges. These factors positively influenced the tourism and hospitality sectors, with the nationwide hotel occupancy rate breaching 70% in February, a first since the pandemic. Despite a gradual decline in “revenge travel,” leisure demand remained strong, with even inbound tourism showing promising signs of recovery. Simultaneously, the MICE and corporate travel segments have been rebounding, even in the face of the hybrid work culture, popularity of online meetings, and higher airfares. As a result, we estimate the Indian hotel industry to conclude the year with an occupancy rate of 63–65%, marking a five-percentage-point increase from 2022, and average rates ranging from INR 7,200 to INR 7,400, reflecting a year-over-year increase of 20%. This will result in a RevPAR of INR 4,600–4,800, indicating a substantial 30% growth from the previous year.

Looking ahead to 2024, we anticipate sustained accelerated growth in the Indian hotel industry, despite ongoing global headwinds and the upcoming general elections. Growth in niche tourism segments, including religious and spiritual tourism, cruise tourism, and medical tourism, coupled with the government’s renewed commitment to the industry and sustained focus on infrastructure development, augur well for the sector’s enduring growth. Moreover, state-of-the-art convention centers such as Bharat Mandapam, Jio World Convention Centre, and Yashobhoomi Convention Center are expected to enhance India’s standing in the global MICE tourism market. As a result, we expect the nationwide hotel occupancy rate to reach pre-pandemic levels of 66% in 2024, with average rates anticipated to near INR 8,000 (32–34% above the pre-pandemic level) for the year.

Asia Pacific

By Hok Yean Chee, President – Asia Pacific

Overall hotel performance across the Asia Pacific markets has continued a recovery in 2023, as most markets removed the last of their health and travel protocols in the first half of the year. This includes the much-anticipated end of travel restrictions for China, such as the removal of quarantine requirements, the resumption of outbound group travel to various countries and issuing of foreign tourist visas, and the removal of pre-departure COVID-19 antigen test requirements. Most markets experienced a full recovery of domestic travel, followed by international travel. This trend was clearly reflected by the strong growth in Chinese outbound international flight bookings during the national public holidays in Q2 and Q3. The top five markets for growth in hotel performance were Beijing, Taipei, Shanghai, Bali, and Tokyo, while Maldives and Langkawi were more static markets. Looking forward to 2024, hotel performance in Asia Pacific is expected to improve.

Overall hotel performance across the Asia Pacific markets has continued a recovery in 2023, as most markets removed the last of their health and travel protocols in the first half of the year. This includes the much-anticipated end of travel restrictions for China, such as the removal of quarantine requirements, the resumption of outbound group travel to various countries and issuing of foreign tourist visas, and the removal of pre-departure COVID-19 antigen test requirements. Most markets experienced a full recovery of domestic travel, followed by international travel. This trend was clearly reflected by the strong growth in Chinese outbound international flight bookings during the national public holidays in Q2 and Q3. The top five markets for growth in hotel performance were Beijing, Taipei, Shanghai, Bali, and Tokyo, while Maldives and Langkawi were more static markets. Looking forward to 2024, hotel performance in Asia Pacific is expected to improve.

In 2022, transaction activity in the Asia Pacific remained steady, with a 4% increase in transaction volume, reaching approximately $13.3 billion USD of hospitality assets sold. While some larger markets may have experienced slower transaction volumes in the past fiscal year, most notably South Korea and China, other markets are making gains, including Australia and Japan. In particular, Japan’s transaction volumes doubled in the last four quarters as compared to the preceding period, registering an increase of $909 million USD. Both countries registered increases in the past fiscal year (3Q 2022 to 2Q 2023) in transactions of over $1 billion USD. The recovery of the Asia Pacific hotel industry has been encouraging in 2023, but investors are still very cautious, citing high interest rates, lingering inflation, and uncertainty in the global economy.

The general sentiment for the Asia Pacific hotel markets in 2024 is one of caution, with demand levels expected to be similar to 2023 levels and ADRs anticipated to grow slowly. This outlook is dependent on the rebound of flights to pre-pandemic levels and construction activity progressing, with loans being more readily available.

About the Authors

Rod Clough is the President of HVS Americas. He is responsible for the overall direction, management, and ongoing success of 40+ offices across North and Latin America. Under his leadership, HVS Americas conducts over 3,500 valuation and consulting engagements annually. During his 30-year tenure, Rod has been instrumental in leading the growth of the firm; this includes significantly expanding the number of offices across the United States, as well as launching multiple divisions, including U.S. Hotel Appraisals, HVS Latin America, HVS Brokerage & Advisory, and HVS Asset Management & Advisory. A frequent speaker at the nation’s largest hotel conferences, Rod is a designated member of the Appraisal Institute (MAI) and a state-certified appraiser. He earned his BS from Cornell University’s School of Hotel Administration and also holds a Colorado real estate broker’s license. Furthermore, Rod is proudly Latino and gay, and his firm is welcoming of all races and colors, sexual orientations, ages, genders, and gender identities. Once associates join HVS, they tend to stay due to the extraordinary culture Rod has inspired—a culture defined by the ideals of balance, connectivity, efficiency, collaboration, honesty, integrity, kindness, and excellence, among others. Rod resides in Northern Colorado where he and his husband Jeff are raising their daughter, Rory. Contact Rod at (214) 629-1136 or rclough@hvs.com.

Rod Clough is the President of HVS Americas. He is responsible for the overall direction, management, and ongoing success of 40+ offices across North and Latin America. Under his leadership, HVS Americas conducts over 3,500 valuation and consulting engagements annually. During his 30-year tenure, Rod has been instrumental in leading the growth of the firm; this includes significantly expanding the number of offices across the United States, as well as launching multiple divisions, including U.S. Hotel Appraisals, HVS Latin America, HVS Brokerage & Advisory, and HVS Asset Management & Advisory. A frequent speaker at the nation’s largest hotel conferences, Rod is a designated member of the Appraisal Institute (MAI) and a state-certified appraiser. He earned his BS from Cornell University’s School of Hotel Administration and also holds a Colorado real estate broker’s license. Furthermore, Rod is proudly Latino and gay, and his firm is welcoming of all races and colors, sexual orientations, ages, genders, and gender identities. Once associates join HVS, they tend to stay due to the extraordinary culture Rod has inspired—a culture defined by the ideals of balance, connectivity, efficiency, collaboration, honesty, integrity, kindness, and excellence, among others. Rod resides in Northern Colorado where he and his husband Jeff are raising their daughter, Rory. Contact Rod at (214) 629-1136 or rclough@hvs.com.

Kristina D’Amico is Managing Director and Leader of the firm’s Caribbean Region consulting and valuation practice. Kristina’s significant international consulting, advisory, and appraisal experience includes assets in the Caribbean Basin across 22 Caribbean islands, as well as the Riviera Maya region of Mexico and many countries in Latin America. Given her analytical skills, her creative-thinking ability, and her aptitude for solving problems that arise in complex projects, clients particularly value Kristina’s insights and recommendations regarding hotel room counts, product positioning, amenities, and branding for many types of proposed properties, including hotels, all-inclusive resorts, and mixed-use resorts with complementary real estate. Contact Kristina at (305) 338-0354 or kdamico@hvs.com.

Kristina D’Amico is Managing Director and Leader of the firm’s Caribbean Region consulting and valuation practice. Kristina’s significant international consulting, advisory, and appraisal experience includes assets in the Caribbean Basin across 22 Caribbean islands, as well as the Riviera Maya region of Mexico and many countries in Latin America. Given her analytical skills, her creative-thinking ability, and her aptitude for solving problems that arise in complex projects, clients particularly value Kristina’s insights and recommendations regarding hotel room counts, product positioning, amenities, and branding for many types of proposed properties, including hotels, all-inclusive resorts, and mixed-use resorts with complementary real estate. Contact Kristina at (305) 338-0354 or kdamico@hvs.com.

Over the course of her 20-year career with HVS, Carrie Russell has been involved with appraisals and/or feasibility studies for over 2,000 hotel properties throughout Canada and the United States. She speaks regularly at industry conferences and has authored several articles on various topics relevant to the industry. As a member of the Appraisal Institute of Canada and the US Appraisal Institute, Carrie combines her hotel industry experience and education with her real estate credentials to assist clients in making informed hotel investment decisions. Contact Carrie at (604) 988-9743 or crussell@hvs.com.

Monique Rosszell AACI, MRICS, is Senior Managing Partner of HVS Canada and leads the Toronto and Montreal HVS teams. Upon attaining a bachelor’s degree in economics from Queen’s University, she subsequently enrolled in the Master’s program in Hotel and Restaurant Management at the Ecole Hôtelière de Lausanne, Switzerland and then attained both her AACI and her MRICS appraisal designations in Canada. Monique has been working in the hotel industry for over 30 years and has completed hundreds of valuations and feasibility studies, including transaction and portfolio valuations throughout Canada and the USA. She is fluent in French and therefore has a strong presence in the Province of Quebec and New Brunswick. She also offers litigation and expert witness support in partnership disputes, hotel expropriation, insurance claims, and general hotel industry norms. She speaks at numerous conferences and is the trusted go-to hotel industry investment advisor within the lodging industry in Central and Eastern Canada. Contact Monique Rosszell at (416) 686-2260 ext. 23 or mrosszell@hvs.com.

Richard Katzman is Senior Managing Partner for the LATAM region. He established the HVS Mexico City office in 2007. He has been active in Mexico and other Latin America countries since 1992. During this period, Richard formed Grupo Inmobiliario Inova, a real estate advisory boutique that merged in 2001 with Insignia/ESG, then among the most prominent real estate service companies in the world. In 2003, following the merger between Insignia/ESG and CB Richard Ellis, Richard elected to reestablish an independent platform prior to joining HVS in 2007. Richard was born and raised in Mexico City. He completed his undergraduate studies at Cornell University, School of Hotel Administration, and received his MBA from The Wharton School. He is fluent in English, Spanish, French, and Portuguese. Contact Richard at +52 (55) 5245-7590 or rkatzman@hvs.com.

Lorea Arnoldi is a Senior Project Manager with HVS Mexico City. Lorea is a graduate of the École hôtelière de Lausanne (EHL), where she earned her Bachelor of Science in International Hospitality Management with a specialization in Finance. Before joining HVS, Lorea gained professional operational and administrative experience through different internships. She held various positions such as Front Desk Assistant at the Hotel Arts Barcelona and Project Manager at Lang & Schwander in Miami. In addition, Lorea completed the Certification in Hotel Industry Analytics (CHIA) through the American Hotel & Lodging Educational Institute (AHLEI) and STR. Lorea’s international experience provides a strong base from which to serve HVS client interests. Please contact Paty at +52 (55) 5245-7590 or larnoldi@hvs.com.

Fernanda L’Hopital, a Vice President with HVS, has dedicated half of her 20-year professional experience to hotel consultancy. Fernanda has in-depth knowledge of the tourism, hospitality, and related real estate markets in South America. During her career in the hotel industry, she has conducted more than 200 studies and has gained plenty of experience in performing market research, feasibility studies, strategic planning, business plans, development plans, highest and best use studies, operator search, management and franchise contract negotiation, and valuations for hotels and other real estate projects. Her regional experience is mainly built on her thorough work in countries like Colombia, Peru, Chile, Argentina, Ecuador, Uruguay, Bolivia, and Paraguay, where she has worked both on operating and developing hotels and other real estate projects. Fernanda has a bachelor’s degree in Economics from Universidad de Buenos Aires and a master’s degree in Business Administration from Universidad del CEMA. For more information, contact Fernanda at flhopital@hvs.com.

Charles Human is President of HVS Europe and managing director of the HVS’s brokerage arm, HVS Hodges Ward Elliott. A qualified Chartered Surveyor, he has worked throughout his career in the real estate industry, specialising during the last 26 years in the hotel sector with HVS. Having worked on projects throughout Europe, Asia and the Middle East, he has a unique knowledge of global hotel markets and hotel concepts. He has led HVS’s activities in the sale, acquisition, and financing of hotels, portfolios and development projects. Charles is a Member of the Royal Institution of Chartered Surveyors. For more infformation, contact Charles at chuman@hvs.com.

Sophie Perret is a senior director at the HVS London office. She joined HVS in 2003, following ten years’ operational experience in the hospitality industry in South America and Europe. Originally from Buenos Aires, Argentina, Sophie holds a degree in Hotel Management from Ateneo de Estudios Terciarios, and an MBA from IMHI (Essec Business School, France and Cornell University, USA). Since joining HVS, she has advised on hotel investment projects and related assignments throughout the EMEA region, and is responsible for the development of HVS’s business in France and the French-speaking countries. Sophie completed an MSc in Real Estate Investment and Finance at Reading University in 2014. Sophie is also a certified surveyor and a member of the RICS. For further information, please contact: sperret@hvs.com or +44 20 7878- 7722.

Sophie Perret is a senior director at the HVS London office. She joined HVS in 2003, following ten years’ operational experience in the hospitality industry in South America and Europe. Originally from Buenos Aires, Argentina, Sophie holds a degree in Hotel Management from Ateneo de Estudios Terciarios, and an MBA from IMHI (Essec Business School, France and Cornell University, USA). Since joining HVS, she has advised on hotel investment projects and related assignments throughout the EMEA region, and is responsible for the development of HVS’s business in France and the French-speaking countries. Sophie completed an MSc in Real Estate Investment and Finance at Reading University in 2014. Sophie is also a certified surveyor and a member of the RICS. For further information, please contact: sperret@hvs.com or +44 20 7878- 7722.

Senior Director of Southern Europe, Ezio Poinelli has more than 25 years experience in Hospitality, Real Estate, and Leisure Real Estate markets in Europe, Caribbean, Latin America, and South Africa. Before joining HVS, Ezio was Head of Southern Europe at Northcourse Advisory Services (Madrid), the hospitality and real estate consulting arm of Wyndham Worldwide, one of the largest hospitality companies in the world. He was also Head of Expansion & International Development at Compañia de Las Islas Occidentales (Canary Islands) and Director – Head of Real Estate and Hospitality at Ernst & Young Financial Business Advisors (Milan). Ezio is a native of Italy, graduate in Economics and Business Administration, Master in Tourism Economics at Bocconi University. He is fluent in Italian, Spanish, and English. For more information, contact Ezio at epoinelli@hvs.com.

Senior Director of Southern Europe, Ezio Poinelli has more than 25 years experience in Hospitality, Real Estate, and Leisure Real Estate markets in Europe, Caribbean, Latin America, and South Africa. Before joining HVS, Ezio was Head of Southern Europe at Northcourse Advisory Services (Madrid), the hospitality and real estate consulting arm of Wyndham Worldwide, one of the largest hospitality companies in the world. He was also Head of Expansion & International Development at Compañia de Las Islas Occidentales (Canary Islands) and Director – Head of Real Estate and Hospitality at Ernst & Young Financial Business Advisors (Milan). Ezio is a native of Italy, graduate in Economics and Business Administration, Master in Tourism Economics at Bocconi University. He is fluent in Italian, Spanish, and English. For more information, contact Ezio at epoinelli@hvs.com.

Demetris Spanos has more than 20 years experience in Hospitality and Leisure Real Estate markets in Europe and the Mediterranean region. Before setting up the Athens office of HVS in 2006, he was the Head of the hospitality team for the South Eastern European region of Ernst & Young Financial Business Advisory (Athens-based) as well as for Arthur Andersen & KPMG for a number of years. He started his career in the hospitality industry back in 1992 as a Managing Director of a major hotel chain in Cyprus. Demetris holds a B.Sc. degree from the University of Patra as well as a M.Sc. from the University of Manchester and an MBA form the Manchester Business School. For more information, contact Demetris at dspanos@hvs.com.

Demetris Spanos has more than 20 years experience in Hospitality and Leisure Real Estate markets in Europe and the Mediterranean region. Before setting up the Athens office of HVS in 2006, he was the Head of the hospitality team for the South Eastern European region of Ernst & Young Financial Business Advisory (Athens-based) as well as for Arthur Andersen & KPMG for a number of years. He started his career in the hospitality industry back in 1992 as a Managing Director of a major hotel chain in Cyprus. Demetris holds a B.Sc. degree from the University of Patra as well as a M.Sc. from the University of Manchester and an MBA form the Manchester Business School. For more information, contact Demetris at dspanos@hvs.com.

Hala Matar Choufany is the President for HVS Middle East, Africa & South Asia and Managing Partner of HVS Dubai.Hala is an experienced Managing Partner and Hospitality Advisor with a demonstrated history of working in the hospitality industry. Skilled in Contract Negotiation, Feasibility Studies, Development Recommendation, Valuation, Asset Management, and Strategic Advisory; she has advised on more than 2,500 hospitality and mixed-use projects in the last 15 years across Europe, MEA and Asia. Hala has in-depth expertise in regional hotel markets and a broad exposure to international markets and maintains excellent contacts with developers, owners, operators, investment institutions and government entities. Hala speaks frequently at investment coneferences on a range of topics including asset valuation, management issues and women leadership. For more information, contact Hala at hchoufany@hvs.com.

Hala Matar Choufany is the President for HVS Middle East, Africa & South Asia and Managing Partner of HVS Dubai.Hala is an experienced Managing Partner and Hospitality Advisor with a demonstrated history of working in the hospitality industry. Skilled in Contract Negotiation, Feasibility Studies, Development Recommendation, Valuation, Asset Management, and Strategic Advisory; she has advised on more than 2,500 hospitality and mixed-use projects in the last 15 years across Europe, MEA and Asia. Hala has in-depth expertise in regional hotel markets and a broad exposure to international markets and maintains excellent contacts with developers, owners, operators, investment institutions and government entities. Hala speaks frequently at investment coneferences on a range of topics including asset valuation, management issues and women leadership. For more information, contact Hala at hchoufany@hvs.com.

Mandeep S. Lamba, President – South Asia, oversees the HVS global hospitality practice for South Asia. He has spent over 30 years in the hospitality industry of which the last 19 have been in CEO positions. Having worked with leading International and domestic Hotel Companies such as IHG, Radisson & ITC Hotels, he also set up joint venture companies with Dawnay Day Group UK and Onyx Hospitality, Thailand to own and operate hotels in India giving him a broader exposure to the hospitality business. An established industry leader, Mandeep has won several awards and recognitions in India and abroad for his accomplishments and contribution to the hospitality industry. He is a Certified Hospitality Administrator from the American Hotels Association (CHA), a member of the Royal Institute of Chartered Surveyors, UK (MRICS) and a member of the Tourism Council of CII (Northern India). Contact Mandeep at +91 981 1306 161 or mlamba@hvs.com.

Mandeep S. Lamba, President – South Asia, oversees the HVS global hospitality practice for South Asia. He has spent over 30 years in the hospitality industry of which the last 19 have been in CEO positions. Having worked with leading International and domestic Hotel Companies such as IHG, Radisson & ITC Hotels, he also set up joint venture companies with Dawnay Day Group UK and Onyx Hospitality, Thailand to own and operate hotels in India giving him a broader exposure to the hospitality business. An established industry leader, Mandeep has won several awards and recognitions in India and abroad for his accomplishments and contribution to the hospitality industry. He is a Certified Hospitality Administrator from the American Hotels Association (CHA), a member of the Royal Institute of Chartered Surveyors, UK (MRICS) and a member of the Tourism Council of CII (Northern India). Contact Mandeep at +91 981 1306 161 or mlamba@hvs.com.

Dipti Mohan, Associate Vice President – Research with HVS South Asia, is a seasoned knowledge professional with extensive experience in research-based content creation. She has authored several ‘point of view’ documents such as thought leadership reports, expert opinion articles, white papers, and research reports across industries including hospitality, real estate, infrastructure, cement, and construction. Contact Dipti at dmohan@hvs.com

Dipti Mohan, Associate Vice President – Research with HVS South Asia, is a seasoned knowledge professional with extensive experience in research-based content creation. She has authored several ‘point of view’ documents such as thought leadership reports, expert opinion articles, white papers, and research reports across industries including hospitality, real estate, infrastructure, cement, and construction. Contact Dipti at dmohan@hvs.com

Hok Yean Chee is the Regional President of HVS Asia Pacific. She has 30 years of experience in more than 30 markets across 19 countries in Asia Pacific, providing real estate investment advisory services for a wide spectrum of property assets. Her forte lies in providing investment advisory on hotels and serviced apartments including brokerage, strategic analyses, operator search, market feasibility studies, valuations and litigation support. For further information, please contact Hok at hychee@hvs.com.

Hok Yean Chee is the Regional President of HVS Asia Pacific. She has 30 years of experience in more than 30 markets across 19 countries in Asia Pacific, providing real estate investment advisory services for a wide spectrum of property assets. Her forte lies in providing investment advisory on hotels and serviced apartments including brokerage, strategic analyses, operator search, market feasibility studies, valuations and litigation support. For further information, please contact Hok at hychee@hvs.com.