By Rishabh Thapar and Achin Khanna

HVS is pleased to share the analysis and insights of the 2016 Hotel Development Cost Survey – India. The development cost is an important aspect of a hotel project that determines its viability. HVS, over the years, has helped investors estimate the overall cost of developing a hospitality project as part of the multiple feasibility studies we have performed for varied asset types across all positioning. This survey endeavours to enhance the knowledge and understanding of industry stakeholders on the subject based on actual development costs of recently opened hotels in India.

The report provides comprehensive benchmarks of hotel development costs across seven different market positioning based on a sample set of 180 hotels that have opened in India over the past six years, with the majority of hotels opening between 2011 and 2015. Besides highlighting an overall development cost for a particular positioning, we have also defined the profile of the hotels by key attributes such as total inventory, built-up area (BUA), number of food and beverage (F&B) outlets, meeting facilities, and so on. Further, we have provided a breakup of the development cost into categories including construction costs, mechanical, electric and plumbing (MEP) and furniture, fixtures and equipment (FF&E), soft cost, pre-opening cost and interest during construction (IDC). However, it may be noted that the survey results do not take into account effects of inflation, change in prices of essential commodities, and currency exchange rates, and instead reflects the development cost provided by the respondents as of the opening year of the hotel. We have researched and compiled information on various physical attributes and facilities mix of the hotels and careful attention has been paid to filter out anomalies, incomplete and questionable data. Also, since land cost may vary across locations and time periods, this survey does not take into account the land cost component while computing the total development cost.

This report is segregated into three parts: (i) sample set and survey results; (ii) detailed analysis; and (iii) key insights.

Sample Set and Survey Results

This section provides the profile of hotels surveyed as well as an overview of the development cost per key by positioning. The sample set represents 29,580 rooms situated across 57 cities in India, which is more than one quarter of the nation’s branded/organised room inventory and close to 60% of the branded/organised room inventory that has opened in India over the last five years. Totally, 38 hotel companies are represented in the survey, with hotels across 78 sub-brands.

Figure 1: Hotel Companies (Branded) Represented in the Survey

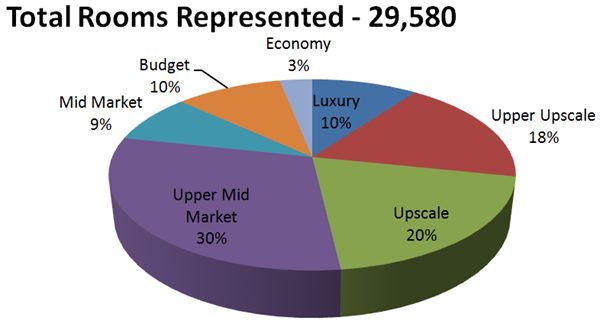

Figure 2: Survey Sample Set – Room Inventory by Positioning

Note: Figure 2 represents a sample set of 180 hotels

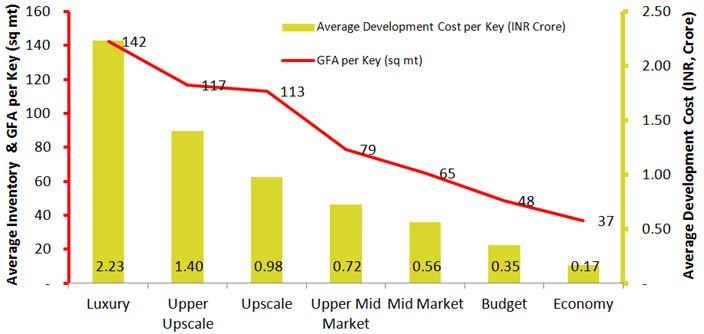

Figure 3: Average Development Cost per Key by Positioning (INR, Crore)

Note: Figure 3 represents a sample set of 180 hotels

GFA per key represents the Gross Floor Area per key calculated by dividing the total above ground area by the total inventory of the hotel

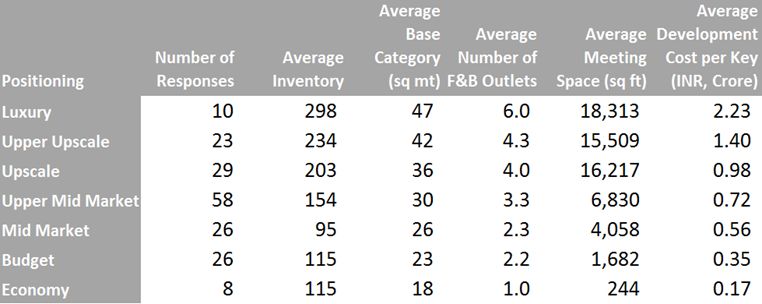

Figure 4: Key Attributes of Hotels and Average Development Cost per Key (INR, Crore)

Note: Figure 4 represents a sample set of 180 hotels

Detailed Analysis

The second part of this survey report presents a detailed analysis of the break-up of development costs of 131 hotels into major categories. The sample set for this section has shrunk from the original 180 hotels, as we have eliminated certain responses owing to insufficient data.

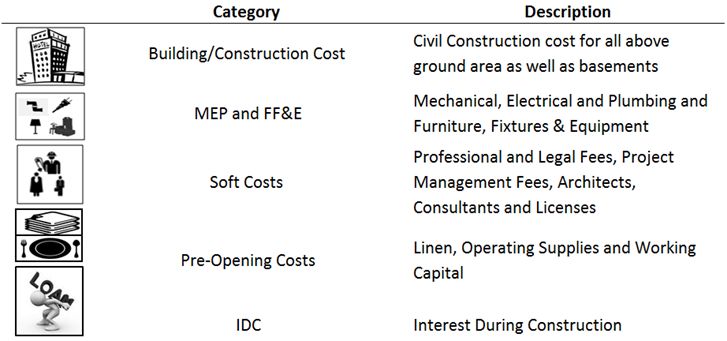

Figure 5: Development Cost by Category – Description

Figures 6 and 7 list the positioning and key attributes of hotels that constitute the detailed analysis.

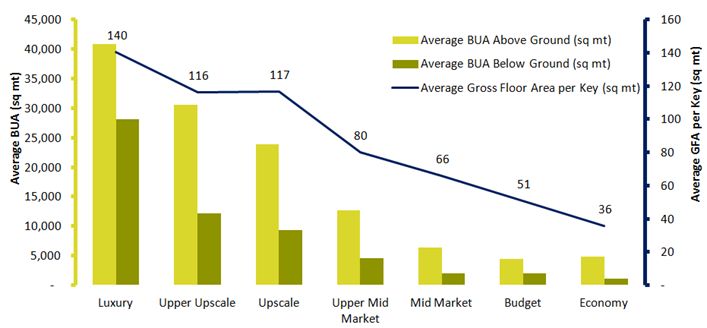

Figure 6: Key Attributes of Hotels across Positioning – Room Inventory, BUA and GFA per key

Note: Figure 6 represents a sample set of 131 hotels

GFA per key represents the Gross Floor Area per key calculated by dividing the total above ground area by the total inventory of the hotel

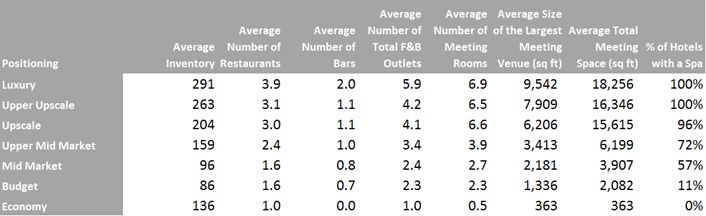

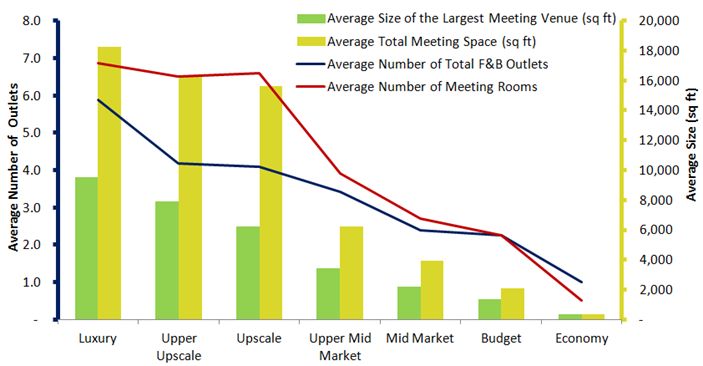

Figure 7: Key Attributes of Hotels across Positioning – F&B Outlets and Meeting Spaces

Note: Figure 7 represents a sample set of 131 hotels

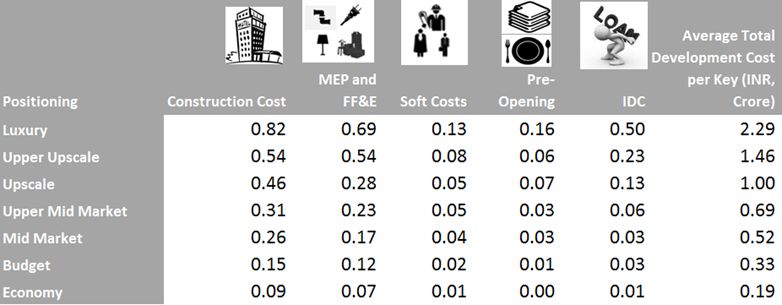

Figure 8: Development Cost per Key by Major Categories

Note: Figure 8 represents a sample set of 131 hotels

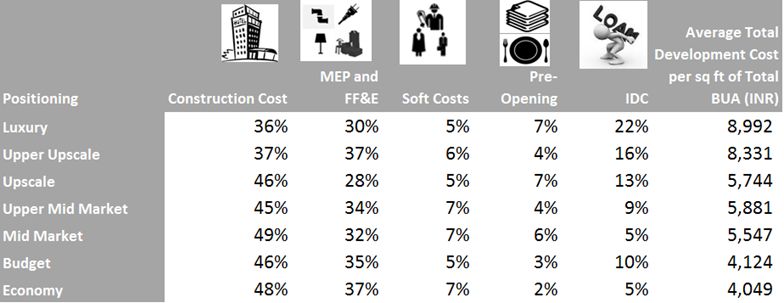

Figure 9: Development Cost per Square Foot of Total Built-Up Area by Major Categories

Note: Figure 9 represents a sample set of 131 hotels

Here, we observe that the total development cost per square foot for Upscale hotels (Figure 9) is lower than that of Upper Mid Market hotels. This is primarily because of the larger incremental spaces in the former, which are not as expensive to build/furnish as rooms. Upscale hotels that were surveyed average 106% higher basement area and 152% more meeting space than the sample set of Upper Mid Market Hotels, bringing down the total average cost per square foot in the former. Analysing further we note that although 17 of the 25 Upscale hotels with an average meeting space of less than 15,600 sq ft have a development cost of INR6,402 per square foot, and the sub set average is dragged down by eight hotels with over 15,600 sq ft of meeting space and a development cost of INR5,127 per sq ft. Thus, development costs must not be evaluated on a per square foot basis only, but rather analysed alongside the facilities mix of the hotel.

Key Insights

The survey results while providing the overall development cost estimate for a positioning, highlight the need for an investor to be cognizant of the many variables that may influence it. Development costs may further vary by the facilities mix, overall built-up area, debt/interest levels and so on. From our analysis and experience in the industry, we highlight below some key insights for an investor.

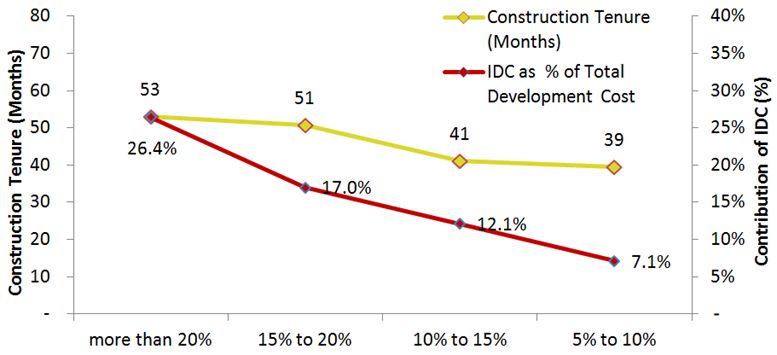

Construction Tenure vs IDC

The Interest during Construction (IDC) on an average is approximately 15% of the total development cost of hotels in India, which is very high when compared to that in advanced hotel markets/countries. The reason lies in the relatively high lending rate and long construction tenure in India. Figure 10 highlights the correlation between long construction tenure and the higher IDC (as a % of the total development cost).

Figure 10: Correlation between Construction Tenure and IDC

Note: Figure 10 represents a sample set of 86 hotels

It is important to note that this trend is not a function of positioning (based on the assumption that hotels with a higher positioning have longer construction tenures). For instance, 14 of the 24 hotels in the 10% to 15% IDC contribution category were built in the Budget, Mid Market and Upper Mid Market segments that normally average an IDC contribution of less than 9%. Thus, the impact of compounded interest as a result of delays, poor financial planning and higher cost of debt – a phenomenon observed on multiple occasions in the last five years – must be avoided to retain the viability of the project.

Government Licenses and Approvals

Acquiring licenses and approvals for a hotel project is a major obstacle in development of hotels in India. The Indian Hotel Owner’s Survey 2016 revealed the need for ease of setting up and doing business and reducing the number of licenses and having a single window clearance to develop and operate hotels as two of the top five demands from the Indian government.

A developer in India typically invests a lot of time, money and effort obtaining licenses and approvals for a hotel project much before breaking ground, and in many states a hotel has to obtain approximately 100 licenses and approvals before it can see the light of day. Unforeseen delays such as those experienced by hotels in Delhi Aerocity are a prime example of how lack of planning by authorities can lead to massive losses for developers and add to the development costs.

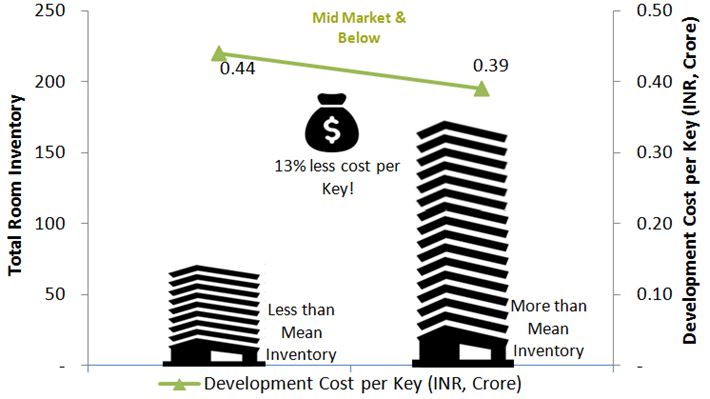

Lower Incremental Cost of Higher Inventory

An analysis of the development cost per key by inventory reveals that hotels with a higher inventory have a lower cost per key owing to efficiencies of scale. This is especially true for hotels built at a mid market or lower positioning. The difference in the development cost per key for a higher inventory (as represented in Figure 11) can be significant, and hence, the viability of developing higher inventory must be evaluated in context of the market conditions.

Figure 11: Correlation between Inventory and Development Cost per Key

Note: Figure 11 represents a sample set of 60 hotels

Not Just Rooms

The survey reveals that more than 60% of all hotels with Mid Market to Luxury positioning have an estimated rooms to total area (above ground) ratio of less than 50%. This means that more than half of the valuable floor space index (FSI) area is being utilised for building what was previously known to be the “ancillary and supporting functions/areas” of a hotel. Today, F&B outlets and meeting spaces form an integral part of hotel operations/revenue mix, and serve as important selection criteria for guests. Thus, effective planning and efficient use of FSI areas is imperative and can go a long way in enhancing functionality and maximizing return on investment for a developer.

Architects and Project Management Companies (PMC)

Hotels, being a highly dynamic real estate asset class, pose a unique challenge on the design front. The job of an architect is especially difficult as he has to balance the need for high functionality and aesthetic appeal with a developer’s vision and passion which oftentimes results in prohibitive overspends. Equally challenging are the coordination and detailing that go along with the execution during the construction and furnishing phases (often requiring feedback, revision and rework). An experienced architect and PMC can make all the difference to not only the construction tenure of a project but the overall product and guest experience. Developers must rely on experts with the requisite skills to manage the intricacies of building hotels, and thus add value by reducing the overall cost and enhance the life of the asset in the long run by leveraging on the architect and PMC’s past experiences.

Highest and Best Use

Hotels entail huge investments that are expected to generate returns over decades, and investors must pay careful attention to the planning process to avoid delays and rework. An efficiently built functional hotel may not yield a good return if built with an inappropriate positioning having a facilities mix that is not in line with the current market conditions and forecasted trends. Hence, a careful assessment of the site, market trends and local bylaws must be made before determining the positioning and facilities mix of a hotel in order to ascertain the highest and best use of the real estate – highlighting the importance of a feasibility study.

In Closing

Hotels are capital intensive investments with long gestation periods. Even as the hospitality landscape in India explores the concept of hotels as part of mixed-used developments and combo-hotels with large meetings facilities, efficiencies in development of hotels though effective cost control and a sensible facilities mix will remain a quintessential ingredient in determining the success of a project. Thus, developers must ensure quality planning and execution of a hotel project along with constant vigilance for compliance and an appropriate financing structure.

Valuable inputs and editing support was provided by Juie S. Mobar.