By Mike McCormick

Today, the GBTA Foundation released its latest quarterly U.S. business travel forecast, slightly downgrading our expectations from the previous quarter. Uncertainty around the upcoming presidential election is among the factors influencing our more pessimistic outlook for U.S. business travel spending through 2017.

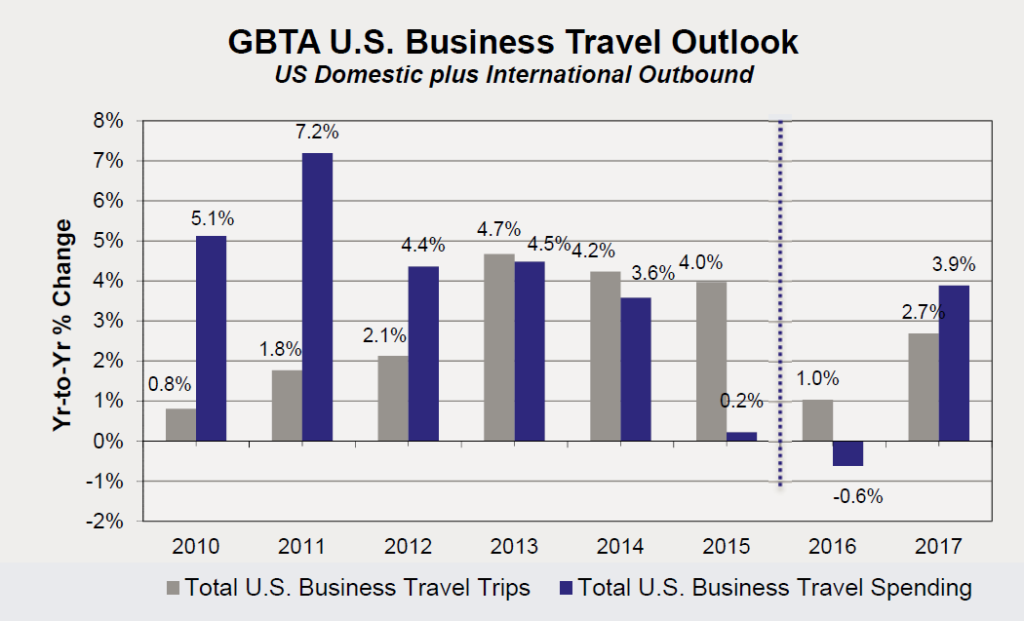

Along with the uncertainty surrounding the election, sluggish global expansion, low inflation, weak investment and choppy geopolitical conditions continue to shackle business travel volume and spending growth. GBTA forecasts business travel volume to advance just 1.0 percent in 2016, while spending falls 0.6 percent.

The report also cites three critical macro drivers of business travel that continue to provide mixed signals including business confidence, corporate profits and international trade. In general, indicators of management confidence remain weak, but narrowly positive suggesting a definitive lack of enthusiasm for the near-term outlook. After-tax profits fell for the fifth consecutive quarter in 2016 Q2, and although they appear poised to return to the plus side during the second half of 2016, expect the continuation of tighter expense controls, lethargic capital spending and constrained business travel growth for at least the rest of the year. Finally, weakness among key U.S. trading partners combined with a strong currency continues to plague export performance.

Indicators point to a better, but still-modest 2017 for the U.S. economy with 2.4 percent GDP growth. GBTA predicts business travel spending will increase 3.8 percent reaching $293.1 billion in 2017, although that will largely be driven by price inflation.

American businesses are hiring, the labor market is doing well, consumer confidence is rising, consumption spending is robust and the housing sector is improving, yet capital equipment, bricks and mortar and business travel spending remain low. Rising uncertainty and weak labor productivity are partly to blame, resulting in more caution and a wait-and-see attitude, particularly with decisions that have longer-term implications.

Businesses are hiring and paying better wages, but business travel spending is stalled – something we rarely, if ever, see happen. The ongoing global uncertainty and added heartburn from a presidential election unlike any we have ever seen are causing many businesses to stay in a holding pattern, taking an extremely cautious wait-and-see approach bordering on paranoia. This begs the question of whether many of these companies will be ready when growth does re-accelerate. To be prepared for lasting business growth, companies must be ready with the newest technologies, the most productive workforce and the critical customer relationships necessary to take full advantage.