Subdued activity as uncertainty delays decision-making

Economic conditions remain challenging in many countries with inflation still stubbornly high, interest rates continuing to climb and softening labor markets, while distress in the banking sector has added to volatility. This is leading to more defensive strategies from occupiers as they delay requirements. Continued uncertainty and elevated borrowing costs are also impacting investor sentiment and inhibiting transaction markets.

The effects of economic headwinds on the office sector increased during the first quarter, with global leasing volumes 18% below Q1 2022 and declining across all three regions. Occupancy losses accelerated in North America, although Europe and Asia Pacific registered positive net absorption over the quarter. Activity in the logistics sector also cooled, with the U.S. and Europe posting declines in leasing activity as the impacts of occupiers’ lengthier decision-making played out.

However, the outlook is for improving conditions towards the end of the year as inflation falls further and the start of the interest rate unwinding cycle comes into sight. Growth is forecast to be weak in 2023 but is still expected to be higher than predicted just a quarter ago.

Global Real Estate Health Monitor

All eyes on interest rates and the debt market

The pressures facing markets during 2022 persisted into 2023. Uncertainty stalled decision-making further and stunted investment activity during the first quarter as price discovery continues. Amid the ongoing rate hike cycle, distress in the banking sector, beginning in the U.S. and later in Europe, introduced additional volatility to real estate lending. These factors have led to tightening lending standards in most markets around the world. The onset of the banking failures has predominantly impacted banks, as a diversity of lenders remain active with a heightened focus on sponsor, sector and asset quality.

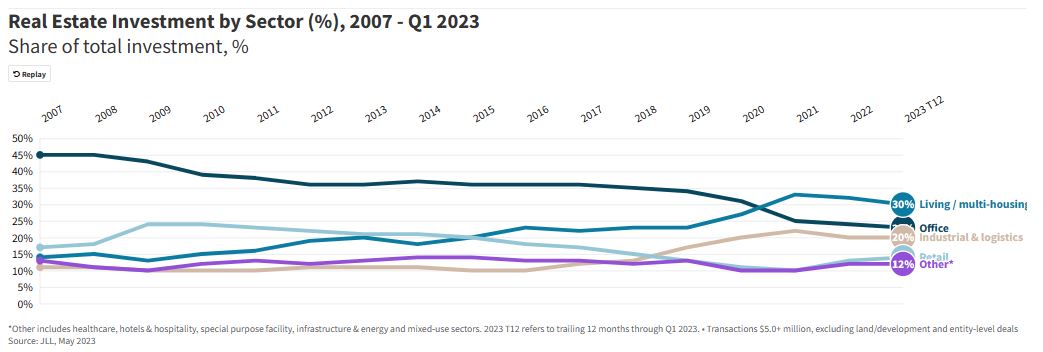

The cyclical and secular outlook for sectors remains mixed, with investor preference for growth sectors amplified as investors develop long-term strategies and portfolio shifts. This is bringing continued focus to the industrial & logistics and living sectors. High-quality retail space is in demand from growth-oriented retailers, while hotels are benefitting from pent-up leisure travel and growing group and corporate demand. The office sector continues to lag the broader market as fundamentals weaken and bidder pools remain shallow, reflecting the structural questions facing the future performance of office assets.

While market dislocation is elevated and liquidity constrained, lending and transactional markets remain active, albeit risks remain elevated in the economy.

![]()