By Hok Yean CHEE

Transactions in the Asia Pacific

In 2022, transaction activity in the Asia Pacific remained steady with a 4% increase in transaction volumes, achieving a transaction volume of approximately USD13.3 billion worth of hospitality assets. While some larger markets may have experienced slowed transaction volumes in the past fiscal year, most notably South Korea and China, other markets are making gains, including both Australia and Japan. Both countries registered increases in the past fiscal year (3Q 2022 to 2Q 2023) in transaction volumes of over a billion USD. Ongoing market conditions including interest rate hikes, slower than anticipated resumption of flight routes and visitors continue to extend an uncertain investment environment in the year ahead.

Transaction History in the Asia Pacific (2018 – 2Q 2023)

Source: HVS Research

*Please note mentions of “transaction values” pertain to the transaction volume based on relevant stake/interest as of the mentioned date

Top Three Most Active Markets (3Q 2021 to 2Q 2023)

Number of transactions have remained the same from 2021 to 2022, with transaction volumes increasing slightly by 4% year over year. It is clear the last four quarters of transactions (3Q 2022 to 2Q 2023 – 427 deals) have slowed compared to the four preceding quarters (3Q 2021 to 2Q 2022 – 593 deals) by 28%. In the last four quarters, the markets of Australia, Japan, and South Korea were leading the transaction volumes for the region. Japan doubled transaction volumes in the last four quarters versus the preceding period, registering an increase of USD909 million.

Transaction Volume in Top Three Most Active Markets (3Q 2021- 2Q 2023)

*Please note mentions of “transaction values” pertain to the transaction volume based on relevant stake/interest as of the mentioned date

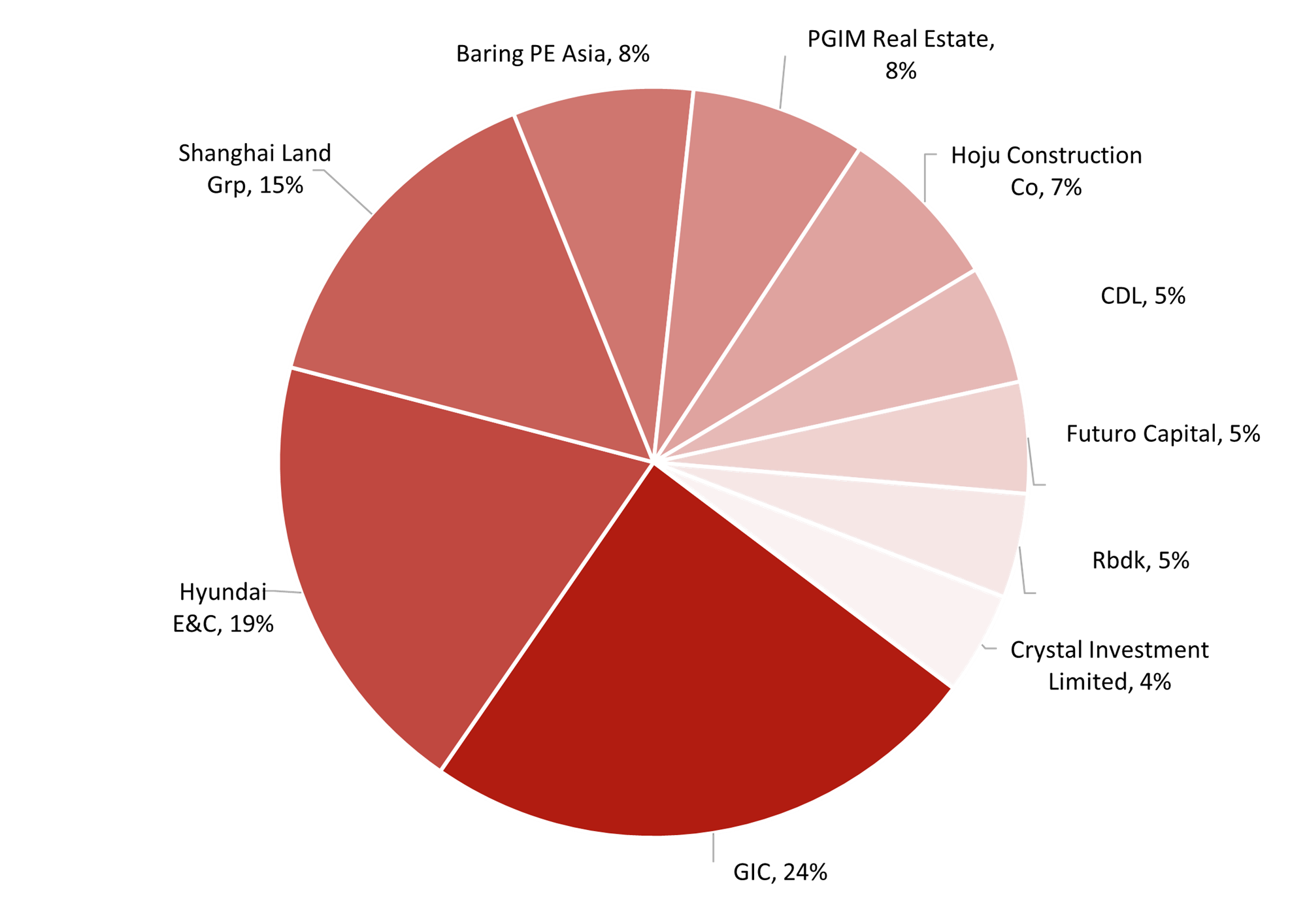

Major Investors in the Asia Pacific

In 2022, transaction activity from the top ten investors in the Asia Pacific accounted for approximately USD4.24 billion or 35% of total transaction volume. In 2022, transaction volumes have steadily increased after a period of slowed activity throughout 2021, impacted by diminished investment sentiment arising from COVID. South Korea showed resilience with over USD4 billion in investments recorded, representing an 18% increase versus the previous year. South Korea ranks first followed by China, Australia, Japan, and Taiwan in volume of transactions for 2022, representing USD10.3 billion. In reviewing activity by number of transactions, Singapore-based GIC recorded 12 transactions in Australia, and four transactions in Japan. Japan-based APA Group recorded 6 transactions, with all properties based locally. Star Lake, a South Korea based company, Japan-based Domus GK each recorded 5 transactions in 2022.

Top Ten Investors

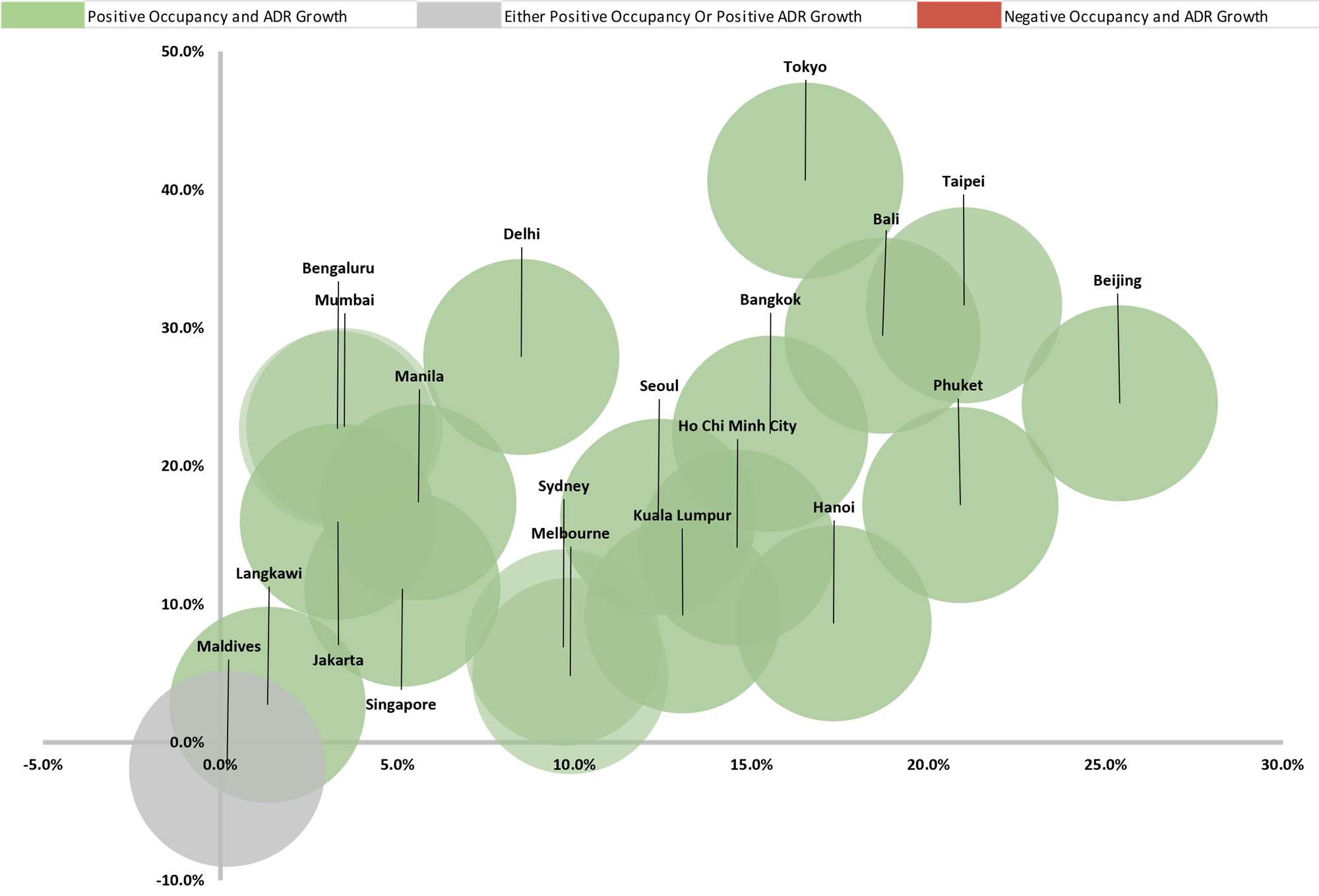

Hotel Performance in the Asia Pacific (2023)

Overall hotel performance across the tracked markets in 2023 is anticipated to continue its recovery, most markets have removed the last of their respective health and travel protocols in the first half of 2023. This includes the much-anticipated release of outbound travel restrictions for Chinese travellers, this includes removal of quarantine requirements, relaxation of outbound group travel to various countries, resumption of foreign tourist visa issuances, and removal of pre-departure COVID-19 Antigen tests requirements. Most markets were expected to recover in domestic travel followed by international, this was clearly reflected by a strong growth in Chinese outbound international flight bookings seen during the National public holidays in Q2.

The top five market growth in hotel performances are Beijing, Taipei, Shanghai, Bali, and Tokyo, while static markets are the Maldives and Langkawi. In general, hotel performance in Asia Pacific is forecasted to improve from 2023. The Maldives’ performance is expected to be static for 2023 with average rates expected to soften after a strong rate recovery in 2022 while occupancy levels are expected to remain stable.

Hotel Performance in the Asia Pacific (2023)

Source: HVS Research