Hotel RevPAR Growth Expected to Remain Above Long-Run Average Through 2018

September 1, 2015, Atlanta, Ga. – Recent gyrations on Wall Street may have hoteliers questioning whether this is the beginning of the end to the good times that have characterized the U.S. hotel industry for the past five years. PKF Hospitality Research (PKF-HR), a CBRE Company, does not believe so and is reaffirming its near-to-mid-term forecast for strong lodging financial performance. According to PKF-HR’s recently released September 2015 edition of Hotel Horizons®, U.S. hotels will continue to enjoy above long-run average revenue per available room (RevPAR) growth through 2018.

“It is hard to ignore what has been happening on Wall Street, but the forecasts of employment and income that we rely on to prepare our estimates of future lodging supply, demand and average room rates (ADR) remain strong,” said R. Mark Woodworth, senior managing director of PKF-HR. “The recent volatility in the stock market is an indicator of the uncertainty that persists in the U.S. and world economies. However, the probability of a downturn in hotel industry performance remains remote.”

If the lodging industry should stumble and that causes a retraction in expected performance, PKF-HR believes U.S. hotels are in a strong position to absorb the negative variance. Since the depths of the great recession in 2009, lodging demand growth has exceeded supply increases and is projected to continue to do so through 2016. This seven-year stretch of continuous occupancy growth is the longest such streak since STR, Inc. began reporting in 1988.

“During historical recoveries, as soon as occupancy returned to pre-recession levels, we saw an immediate, strong uptick in real ADR growth. That did not occur this time around,” Woodworth said. “In real terms, prices are just now returning to their previous peak. The U.S. occupancy level is now a full three points above the 2007 mark. This performance premium represents a substantial cushion that should offset an unexpected decline in demand.”

Record Occupancy

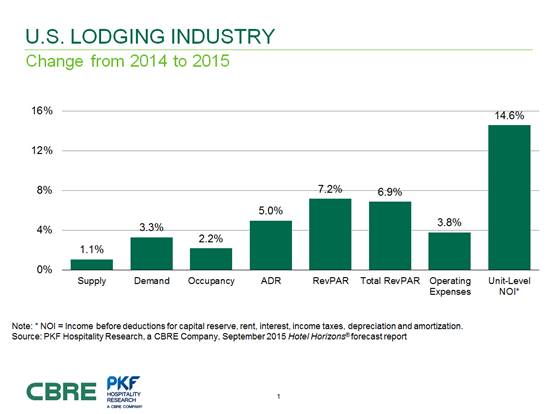

Seven years of demand outpacing supply results in PKF-HR forecasts of record levels of occupancy. From 2015 through 2017, PKF-HR is projecting the national occupancy rate to remain above 65.5 percent. According to STR, Inc., the previous high water mark for occupancy was 64.7 percent in 1995. “At such lofty occupancy levels, we are projecting ADR gains ranging from 5.0 to 6.3 percent over the next three years,” Woodworth stated. “Throw in the continued increases in occupancy, and you have some very meaningful ADR-driven RevPAR growth that, given the operating leverage characteristic of hotels, particularly at this level, will flow through nicely to the bottom-line.”

The positive outlook for the U.S. is broad-based. All chain-scale segments are forecast to enjoy RevPAR growth in excess of 6.0 percent in 2015 and 2016. “The RevPAR gains in the upper-priced segments will be driven mainly by growth in ADR. The lower priced-properties will experience a more balanced mix of increases in both occupancy and ADR,” Woodworth added.

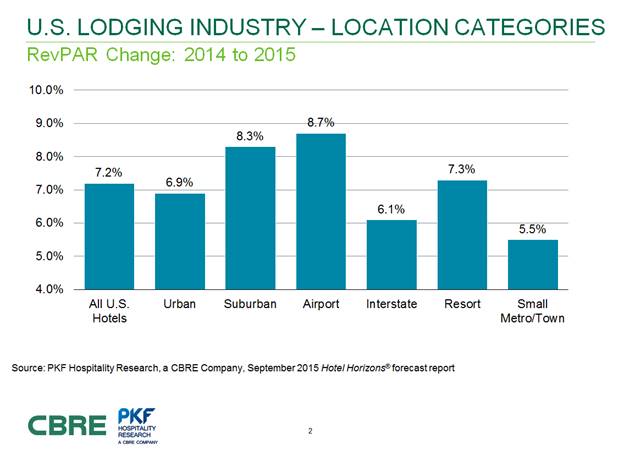

Location Matters a Lot

“Per the well-worn adage about the importance of location in real estate, location matters,” said John B. (Jack) Corgel, Ph.D., the Robert C. Baker professor of real estate at the Cornell University School of Hotel Administration and senior advisor to PKF-HR. “While all chain-scale categories are enjoying strong performance, we are observing some meaningful differences when comparing lodging performance by location.”

For 2015, hotels located in airport and suburban areas are forecast to achieve the strongest gains in RevPAR. “In several markets, the continued return of large conventions is now causing a compression that is forcing demand out of the urban core and into the suburbs. Further, recent ADR growth in 24 airport sub-markets that we track is up by 6.0 percent or more,” Corgel noted.

Lagging in RevPAR growth are properties located along the nation’s highways and in small rural markets. “The interstate market is very seasonal which places a realistic cap on annual occupancy growth. In addition, the interstate and rural lodging inventory competes almost exclusively in the lower-price tiers and have been unable to attain pricing power,” Corgel said.

Fundamentals Trump (no reference here to Donald) Headlines

“Hotel owners and operators cannot ignore the headlines entirely. They remind us that there is some level of uncertainty out there. However, the economic fundamentals that drive lodging demand are a story well worth reading,” Woodworth concluded.