Optimistic outlook for further growth in 2018 and 2019

NEW YORK, June 28, 2018 – New York is a hot spot of major transformational real estate development that is rapidly changing the city’s landscape and lodging environment, according to JLL’s 2018 New York Hotel Market Report.

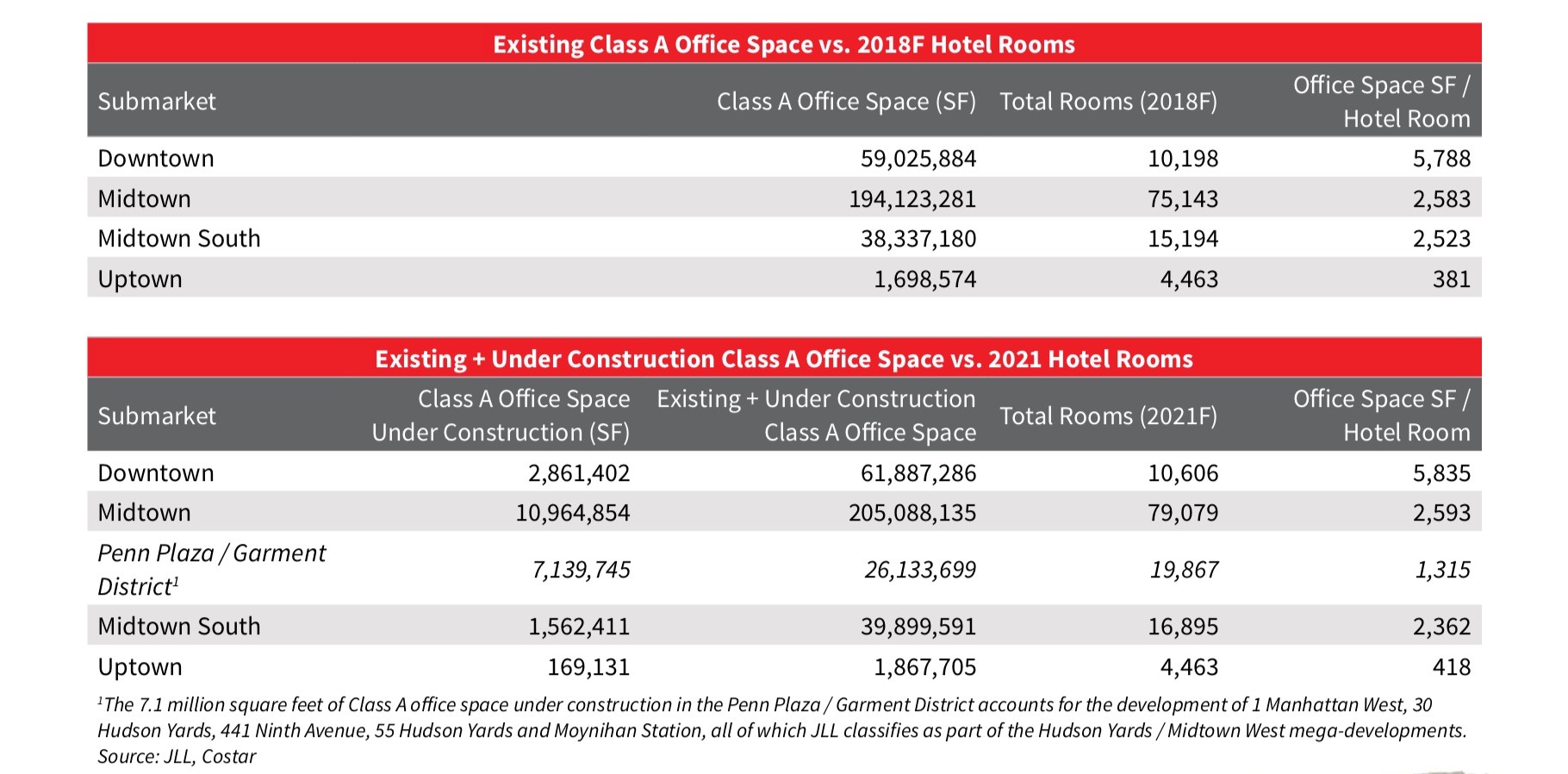

Hudson Yards, situated in the Midtown West submarket, currently represents the largest private real estate development in the history of the United States and the largest development in New York since the Rockefeller Center. The Manhattan West District and Moynihan Station developments will also grace the Midtown West submarket and are targeted for delivery by 2022.

Transformative redevelopments are also occurring in Midtown East and Downtown, all of which will elevate each respective neighborhood’s profile. One Vanderbilt is underway in the Midtown East submarket—a 1.7 million gross square foot office skyscraper that will stand next to Grand Central Terminal. When complete, One Vanderbilt will represent the second tallest building in the city.

Lower Manhattan is also being rejuvenated and with the expected delivery of 3 World Trade Center by year-end. The World Trade Center hub and memorial have recently been activated and millions of square feet of retail have been added, including Pier 17, a quaint boardwalk in the area.

This unprecedented surge creates a dynamic where submarkets previously concerned with increasing hotel room supply may become under-supplied in the next five years. This is because the level of existing and anticipated Class A office space in the market will support rapid hotel room absorption.

RevPAR performance to date suggests that new supply additions are slowing and being absorbed. Therefore, we expect RevPAR growth to become more pronounced in 2019 and 2020, as fewer rooms are anticipated for delivery over these two years than are projected to be delivered in 2018 alone.

Opportunity to improve margins

In an analysis of 90 P&L statements of New York City hotels from 2013 to 2017 by JLL, the data suggests that gross operating profit (GOP) performance bottomed in 2016. Performance in 2017 started trending upward and performance in 2018 is off to a promising start, driven by YTD May 2018 demand growth of 6.0 percent.

“Over the analyzed period, we noted that GOP is more sensitive to changes in RevPAR than supply. On average, when RevPAR shifts one percentage point (negative or positive direction), GOP will shift a corresponding three percentage points,” said Gilda Perez-Alvarado, Managing Director, JLL. “As such, with sustained improvement in demand fundamentals and muted supply growth, the market will gain more rate integrity, resulting in positive RevPAR growth and stabilized margins at year-end.”

New York transaction volume to reach robust levels supported by acquisitions from private equity and New York centric owners/developers

With YTD June hotel sales of $2.3 billion, New York’s hotel transaction volume is nearly five times the volume achieved during the same period in 2017. The drivers behind the exceptional level are the sale of Edition Times Square for $1.53 billion (inclusive of retail and signage) and the disposition of W Hotel New York for $190 million.

Since 2017, capital in the market has primarily originated from domestic private equity and New York centric owners/development companies, accounting for 81.0 percent of acquisitions. However, over the past five years, foreign investors have acquired nearly $10 billion in New York hotels. As such, we expect cross-border investment to pick up throughout the remainder of the year as the product quality brought to market continues to improve.

Opportune time to invest in New York hotels

Reviewing the data on a per-room basis, hotel transaction values peaked in 2015. Today, the twelve-month moving average price per room is at approximately 80 percent of the level seen in early 2015, indicating that right now, hotels in New York are transacting at multi-year lows.

Hot debt markets

The hospitality debt markets are performing well and notwithstanding New York’s elevated supply pipeline, lenders such as commercial banks, insurance companies, debt funds and CMBS, remain interested in financing New York hotels.

Further, indicators suggest that the current economic expansion is only accelerating as the effects of the recently passed tax legislation have yet to be felt. This dynamic bodes well for the debt markets and as such, in the second half of 2018 we anticipate additional spread compression, greater liquidity available in the market, and more aggressive underwriting and loan structures.

New York: a coveted hotel investment destination

New York is one of the most coveted hotel investment destinations. Its unwavering economic strength and tourism appeal will help the market overcome current supply challenges, allowing the market to experience meaningful growth in the near future.

From 2012 to YTD June 2018, New York has recorded $17.6 billion worth of single-asset sales, placing it ahead of other major gateway markets such as London ($12.9 billion), Paris ($5.8 billion) and Hong Kong ($3.1 billion) for the same period.

For more insights on how New York’s transformational real estate developments are impacting the lodging sector, download JLL’s 2018 New York Hotel Market Report.

JLL's Hotels & Hospitality Group has completed more transactions than any other hotels and hospitality real estate advisor over the last five years globally, totaling more than $77.5 billion worldwide. Between negotiating property deals, the group's 350-person global team also closed more than 5,300 advisory, valuation and asset management assignments. To find out more visit: www.jll.com/hospitality.