After twelve months of declining occupancy and improving ADR from April 2023 through March 2024, the U.S. lodging market appears to have entered a period of relative stability, with changes in both metrics more subdued than in the recent past. However, as with most averages, these aggregate results comprise notable variations among individual markets and lodging segments.

The meeting and group segment continues to increase, supported by both improving convention activity and continued growth in corporate group meetings and events. These trends are particularly beneficial to the luxury and upper-upscale segments of the market, as well as in metro areas where these types of properties maintain a strong presence. Commercial demand also continues to recover, as more companies and entities implement return-to-office requirements. Amazon’s recently announced return-to-office policy may be the harbinger of a broader trend, which would be expected to benefit both occupancy and ADR levels.

Leisure demand continues to normalize from the spike that followed the initial impact of the pandemic. As a result, markets and submarkets that depend on this sector are reporting some corrections. However, although occupancy and/or ADR have shown recent softness, both metrics remain above—and in some cases, well above—pre-pandemic norms. And the broad consensus is that leisure travel will remain a significant influence on markets throughout the United States.

The supply outlook remains a positive factor. Although the pipeline is, by some standards, robust, the realistic expected increase in supply is less significant. Hotel openings in the next several years would include projects that began from 2021 through 2024. The elevated construction costs and limited financing availability for new construction that characterized these years raised the bar for project feasibility, with the result that supply growth is expected to remain well below historical norms for the next several years.

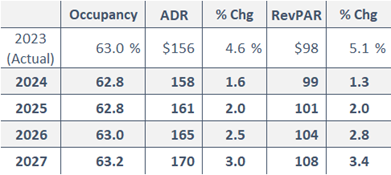

Overall, we anticipate stability or modest growth during the balance of 2024 and in 2025, followed by stronger growth through 2027. As with current statistics, these forecasts are averages and, thus, encompass a fairly wide array of anticipated results.

Source: HVS