By Anthony J. Jackson, Peter Caputo, Maggie Rauch, Stephen Rogers

Prolonged inflation has taken its toll on consumers’ finances. Even as inflation rates show signs of easing,1 roughly four in 10 Americans surveyed in Deloitte’s Global State of the Consumer Tracker feel financially worse off compared to a year ago.2 Many continue to cite concerns around savings and nearly half still say they’re delaying large purchases.3 Americans’ sense of financial well-being seems to have taken a hit, and over the past year, so has spending confidence.4 Recession warnings certainly aren’t making matters any better.

Through all the gloom, however, the US travel industry recovery doesn’t seem to have skipped a beat. Hotel occupancy is beginning to rival prepandemic levels.5 Rooms command significantly higher rates compared to 2019.6 And, in February 2023, more passengers moved through US airports than February 2019.7 Lagging group demand and inbound tourism must improve before the industry fully recovers. But at the very least, travel’s current momentum doesn’t seem to tell the story of a country slipping closer to potential recession.

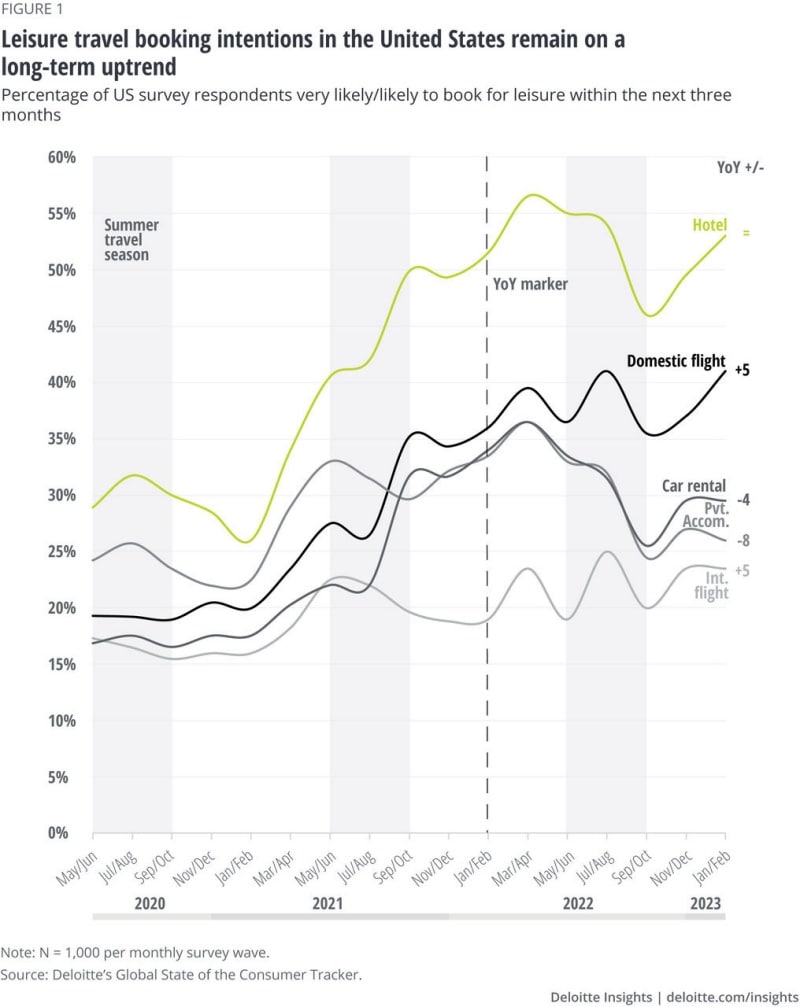

The US consumer may lie at the heart of the recovery. After years without coveted getaways, built-up pandemic demand is likely still shaping industry dynamics. Travel booking intentions (the percentage of survey respondents likely to book leisure trips within the next 3 months) have been on a clear uptrend since 2021 (figure 1). More recently, booking intentions have been particularly strong for both domestic and international travel. Both segments are up year-on-year, signaling a travel recovery still in full swing.

Travel’s recovery story probably isn’t just about growth—a bit of recalibration is also necessary. Booking intentions aren’t rising across all travel segments. Private accommodation rentals, for example, have weakened considerably since early 2022 (figure 1). Throughout the pandemic, travelers gravitated to segments better suited for social distancing. As health and safety concerns fade away, pandemic travel preferences are fading along with them.

Travel intentions continue trending higher, even as Americans contend with prolonged financial challenges. And part of the reason might be how consumers are prioritizing their overall spending.

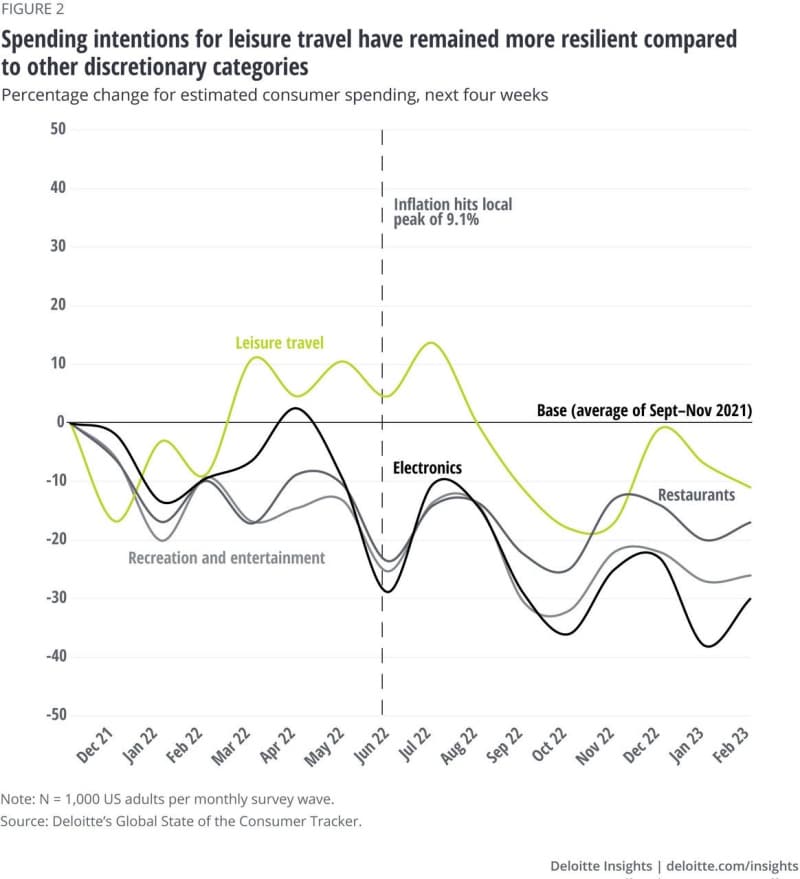

Discretionary spending intentions have weakened considerably since the fall of 2021, when inflation first began putting a strain on household budgets (figure 2). But planned spending cutbacks, however, have been deepest in categories such as restaurants, recreation and entertainment, and electronics. Spending intentions for leisure travel, however, have remained much more resilient. The prioritization of travel over other discretionary categories is further evidence that built-up demand still exists in the market.

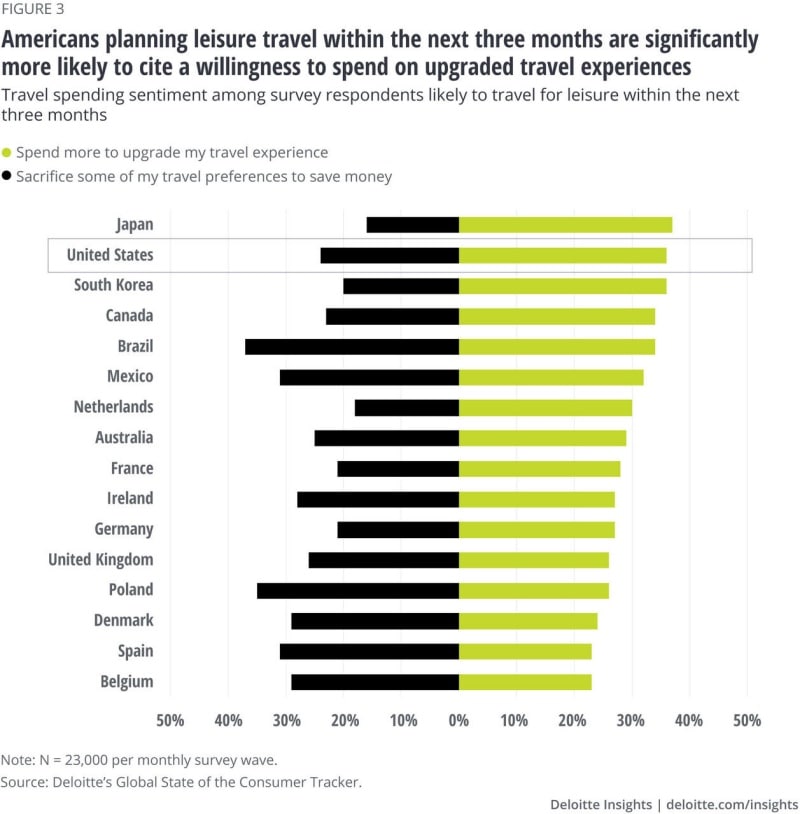

Additionally, Americans planning to take vacations within the next three months are significantly more likely to cite a willingness to spend on upgraded travel experiences, rather than sacrifice some of their travel preferences to save on travel costs (figure 3). For US-focused travel suppliers, this sentiment perhaps shouldn’t be taken for granted. In many countries, including Spain, Belgium, Denmark, Ireland, and Brazil, savers outnumber spenders.

What’s in a trip? Many ways to adjust based on budget

Despite the many positive signals around travel spending, roughly one-quarter of soon-to-be travelers surveyed say they’re in savings mode. And this group is important to pay attention to. If economic conditions worsen, travel savers could quickly grow in number.

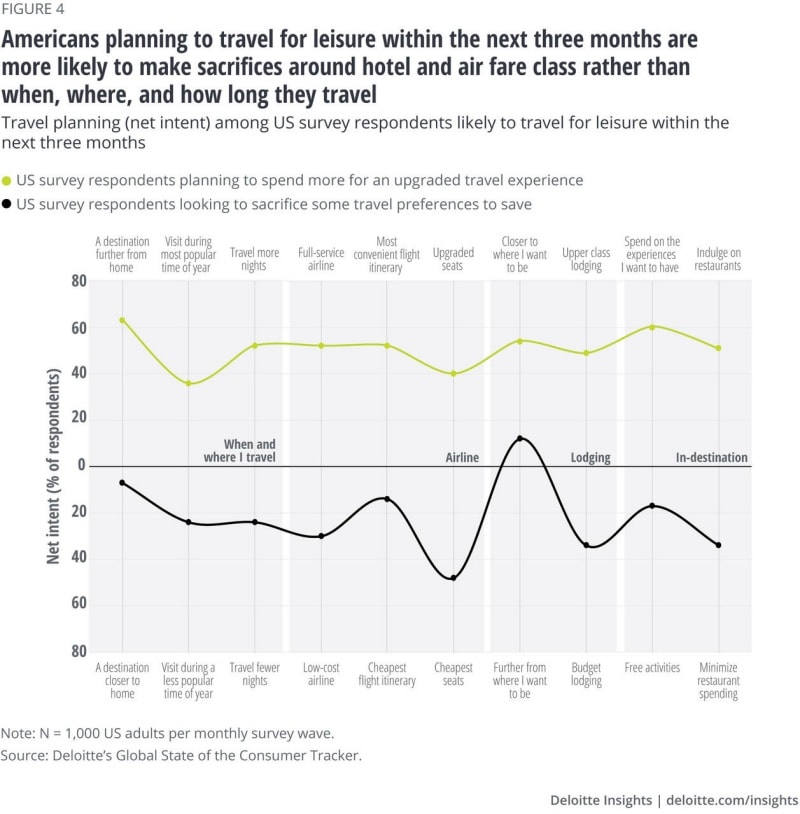

Figure 4 presents 10 distinct points in the travel journey (from planning to in-destination)—and illustrates where “spenders” intend to splurge and where “savers” intend to make sacrifices on upcoming leisure trips.

Following are some key takeaways:

- Lodging location is king: Consumers are less likely to compromise by staying further from the beach/city center; instead, more travelers cite a willingness to downgrade on amenities or class of lodging.

- Location in terms of destination is another high priority: More travelers would prefer to find a less popular time of year to travel than miss out on visiting the destination they want to visit. This sentiment lines up with stronger booking intentions for international travel in recent months.

- Itinerary is the “location” of aviation: When it comes to flights, soon-to-be travelers will book a lower-fare class or forego an upgrade before they will accept an inconvenient itinerary. Even savers appear to be trying to avoid those painful itineraries.

- Let me do my thing! In-destination travel activities remain a high priority for savers and spenders alike. More travelers would rein in their restaurant spending than miss out on the experiences they want to have.

After being dealt a heavy hand throughout the pandemic, airlines, hotels, and other travel suppliers face new economic uncertainties that bring the potential to weaken consumer spending confidence. But sentiment data suggests Americans are prepared to put up a fight to protect their vacations, which could help mitigate some headwinds from a potential downturn. Barring any further economic volatility, the 2023 summer season could be shaping up to be a strong one.

In the coming months, Deloitte’s 2023 summer travel survey and corporate travel study will offer further insight into consumer vacation intentions and trajectory for corporate travel’s recovery.