Both Group and Transient Leisure Travel Experience Particularly Solid Growth in Bookings

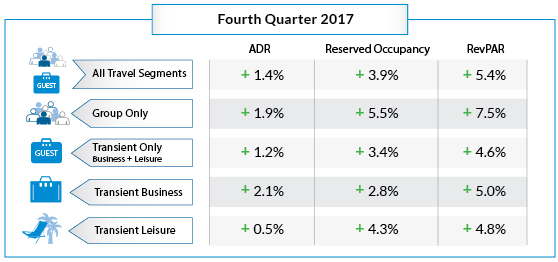

NEW YORK – November 20, 2017 – As North American hoteliers enter the holiday season and round out the year, all travel segments are seeing a noticeable increase across the board in both average daily rates (ADR) and occupancy, up 1.4 percent and 3.9 percent respectively, during the fourth quarter of 2017, according to new data from TravelClick’s November 2017 North American Hospitality Review (NAHR).

Hoteliers are also experiencing a particularly strong uptick when it comes to bookings for both the group and transient leisure segments, up 5.5 percent and 4.3 percent respectively – largely a result of favorable economic trends, coupled with an increase in holiday travel this year. Additionally, ADR is up 1.9 percent for group travel and 0.5 percent for transient leisure travel overall.

“Significant revenue per available room (RevPAR) growth accompanies these year-end increases in ADR and bookings, and hoteliers should relish in the current state of the industry and enjoy the holiday boost consequently,” said John Hach, TravelClick’s senior industry analyst. “This last quarter has given hoteliers much promise heading into the New Year, especially considering the inconsistent market that we experienced throughout most of 2017.”

Twelve-Month Outlook (November 2017 – October 2018)

For the next 12 months (November 2017 – October 2018), transient bookings are up 4.6 percent year-over-year, and ADR for this segment is up 1.1 percent. When broken down further, the transient leisure (discount, qualified and wholesale) segment is up an impressive 7.6 percent, and ADR is up 0.7 percent. Additionally, the transient business (negotiated and retail) segment is up 1.4 percent, and ADR is up 2.6 percent. Lastly, group bookings are up 1.0 percent in committed room nights* over the same time last year, and ADR is up 1.8 percent.

“While these fourth-quarter numbers are a breath of fresh air, hoteliers shouldn’t lose sight of the preparations that are needed for the post-holiday season, especially given the weakness in first-quarter 2018 group committed occupancy,” added Hach. “Given this news, hoteliers need to make proactive decisions and take advantage of business intelligence tools and forward-looking data so that they can plan accordingly in the coming months and stay ahead of the competition in 2018 and beyond.”

The November NAHR looks at group sales commitments and individual reservations in the 25 major North American markets for hotel stays that are booked by November 1, 2017, for the period of November 2017 to October 2018.

*Committed Occupancy – (Transient rooms reserved + group rooms committed) / capacity

The fourth quarter combines historical data from October and forward-looking data from November and December.