By Dr. Isabella Blengini

How Covid hit the economy

The Covid health crisis translated into an economic crisis through two main channels. On the one hand, health issues reduced the availability of labor force, thus reducing production. On the other hand, the great lockdown, necessary to fight the disease, limited the ability of some sectors to produce (either because they were directly blocked or because they could not receive intermediary goods necessary for production).

Besides the above-mentioned negative supply shocks, the economy was also hit by a negative demand shock due to several reasons including people losing their jobs and forced cessation of certain activities.

The goal of this report is to present recent data on GDP growth in Switzerland between 2020 and 2021. A particular emphasis will be given to the reaction to the Covid crisis of individual sectors of the economy. In order to better contextualize and understand the impact of the pandemic on the Swiss economy, we will provide data on other economies, including France, Sweden, the UK and the US.

The case of Switzerland

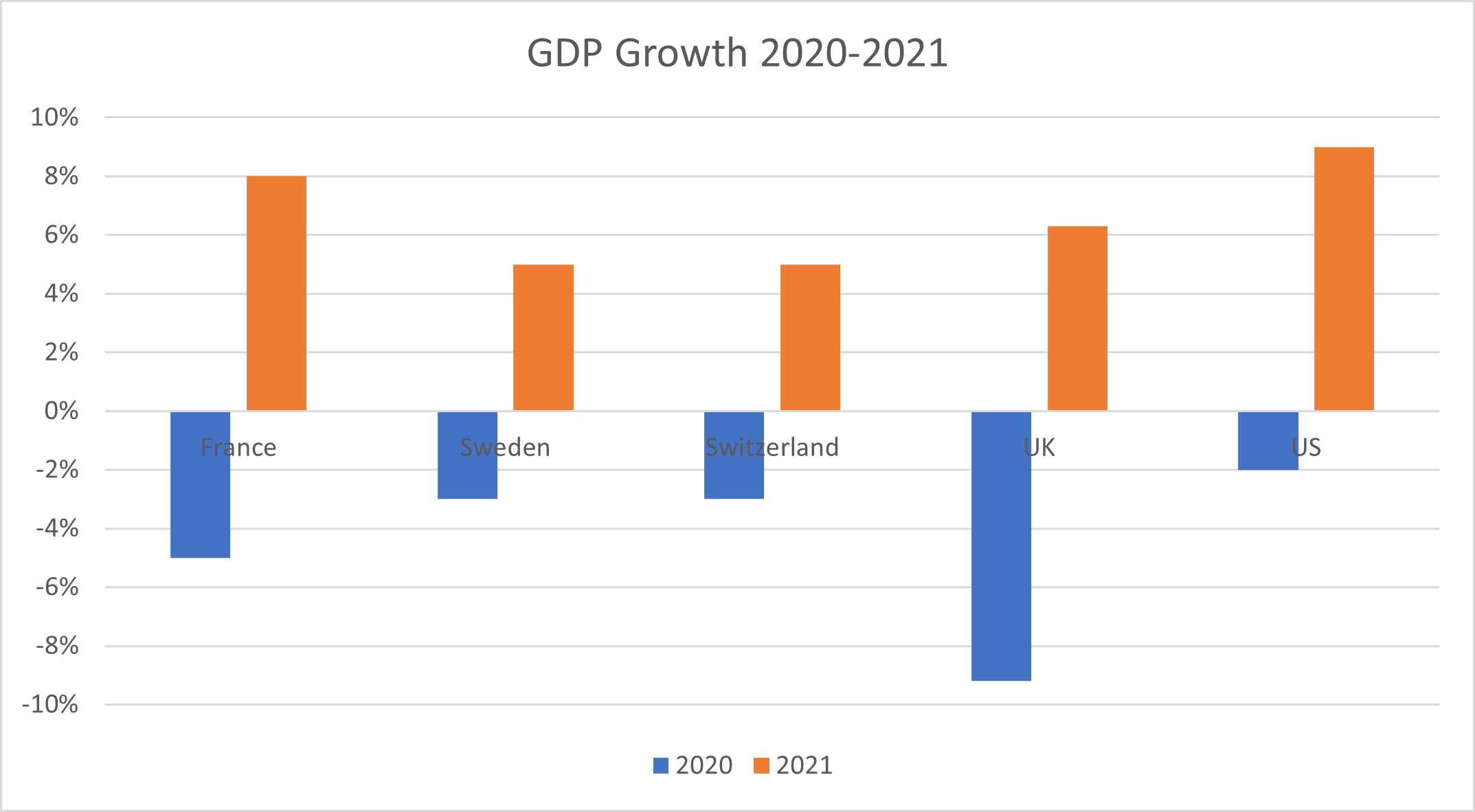

In the case of Switzerland, data show that its largest GDP contraction took place in the second quarter of 2020. Overall, in 2020 Swiss GDP went down only by 3% with respect to the previous year, and it recovered quite quickly in 2021, increasing by 5%. As you can observe in Figure 1, among the countries considered, the UK experienced the worst drop in GDP (-9%) in 2020, followed by France (-5%), Sweden and Switzerland (-3%) and the US (-2%). In 2021, the economies shown here promptly recovered. The highest growth rate was observed in the US (+9%), followed by France, UK, Sweden and Switzerland.

Figure 1: GDP Growth Rates in 2020 and 2021. Source: Individual countries’ statistical offices.

In order to better understand the aggregate contraction observed in 2020, we identified the sectors that paid the most for the pandemic.

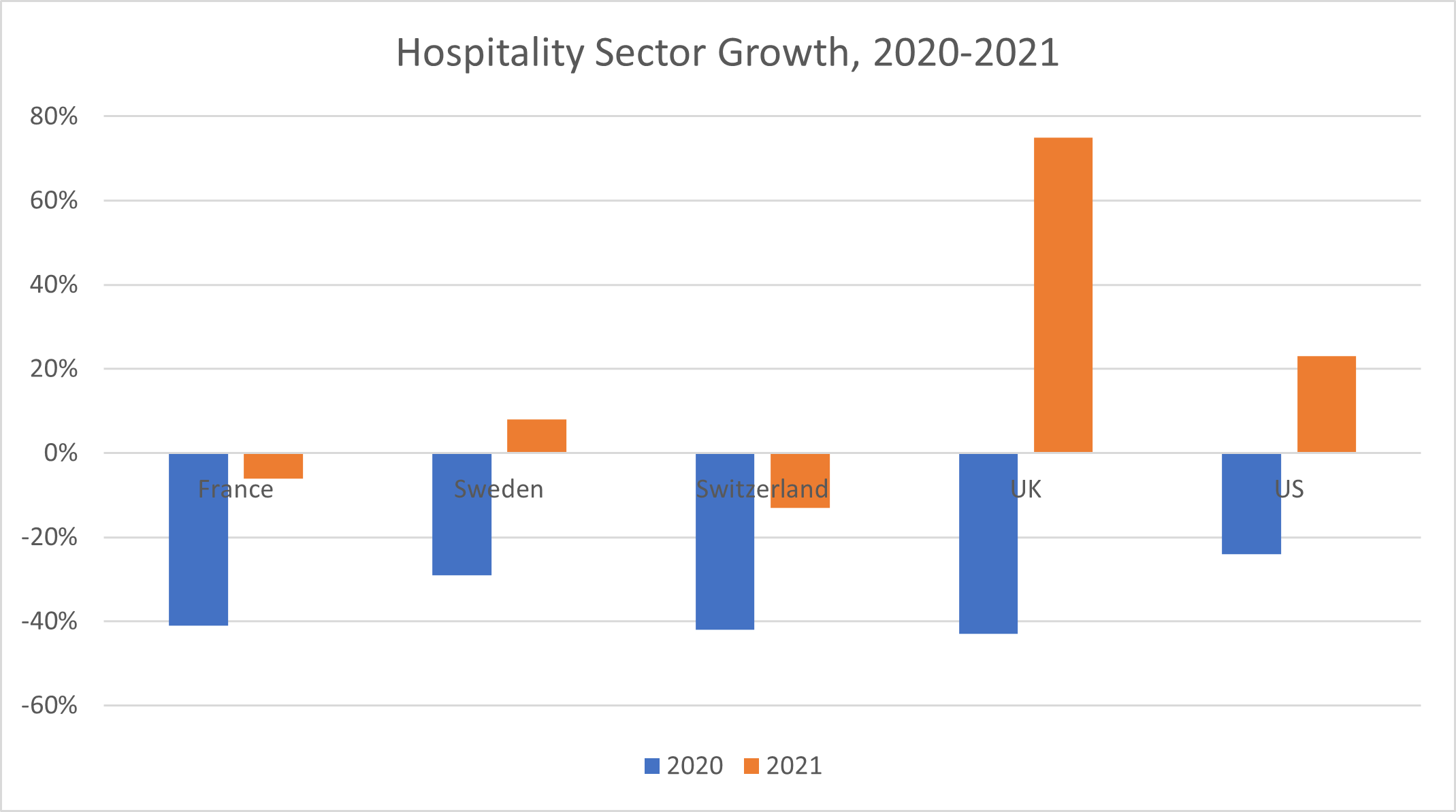

As you can observe in Figures 2 and 3, the hospitality sector, including accommodation and food & beverage, was the most hit by the crisis. In the specific case of Switzerland, the hospitality industry registered in the second quarter of 2020, a 60% reduction in production with respect to the previous quarter. In the third quarter was been a 115% recovery, and then another 20% drop in the fourth quarter of 2020.

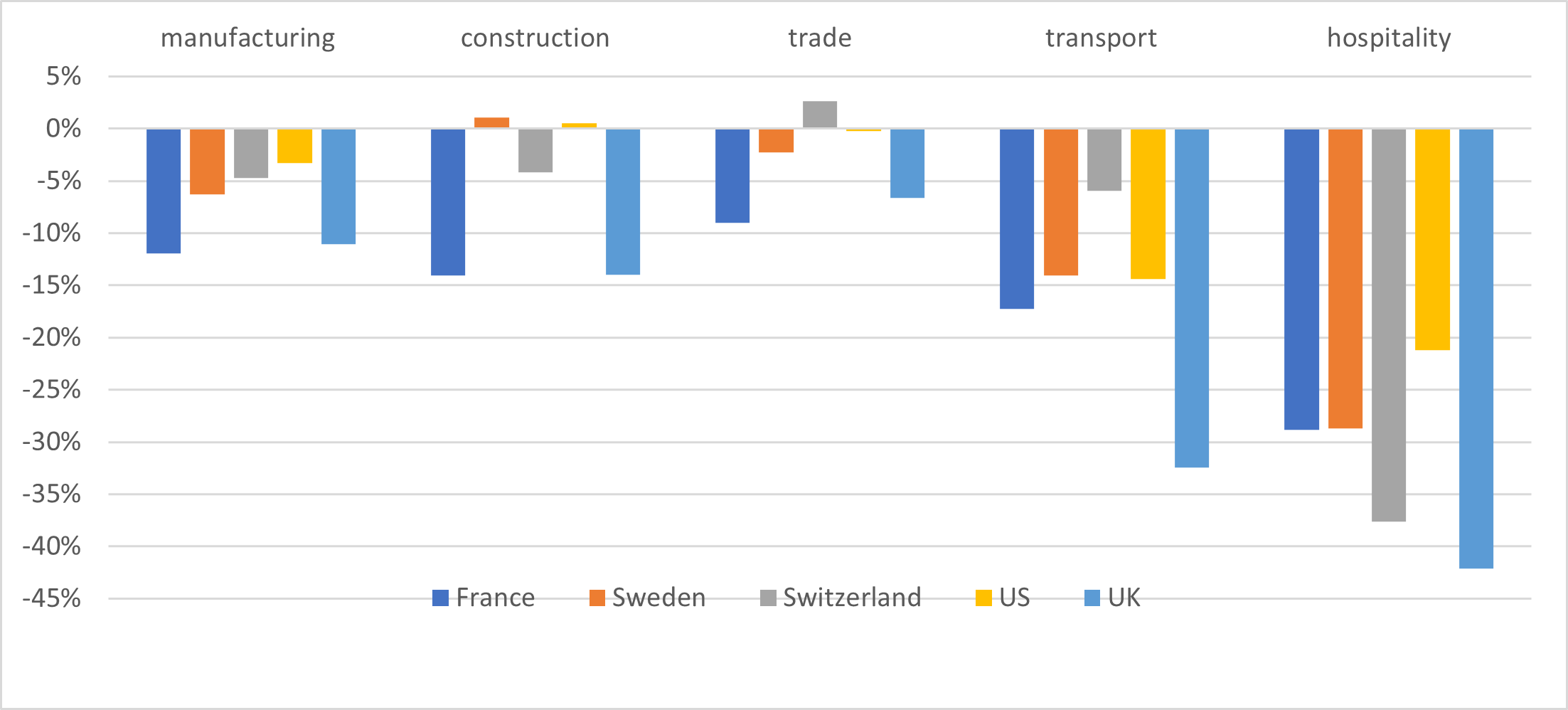

As shown in Figure 3, in 2020 other sectors [1] including manufacturing, construction, trade and transportation, experienced a slow down with respect to the previous year. It is worth noting that the higher importance of these sectors within the aggregate Swiss economy, implies that a 5% drop in manufacturing had a larger impact on GDP than a 40% drop in hospitality [2].

When considering the other countries, data suggest that the hospitality sectors in the UK, Switzerland and France were hit particularly hard by the pandemic. It is interesting to observe the difference in the reaction between the UK’s hospitality sector that had a huge expansion in 2021, while France and Switzerland’s sectors kept lagging behind the other countries also in 2021.

Figure 2: Hospitality Sector growth rates by country, in 2020-2021. Source: Individual countries’ statistical offices.

When considering the other sectors (Figure 3), it is clear that transport and manufacturing have also been affected by the crisis in an important way. The construction sector suffered especially in France, in the UK and also in Switzerland. While we observe a positive growth rate in the trade sector for Switzerland, and a quite important contraction in France and in the UK.

Figure 3: Growth rates by country and by sector in 2020. Source: Individual countries’ statistical offices.

Overall, as the data suggest, the pandemic hit more or less the same sectors in a somehow similar way, despite the very heterogeneous government interventions in the different countries.

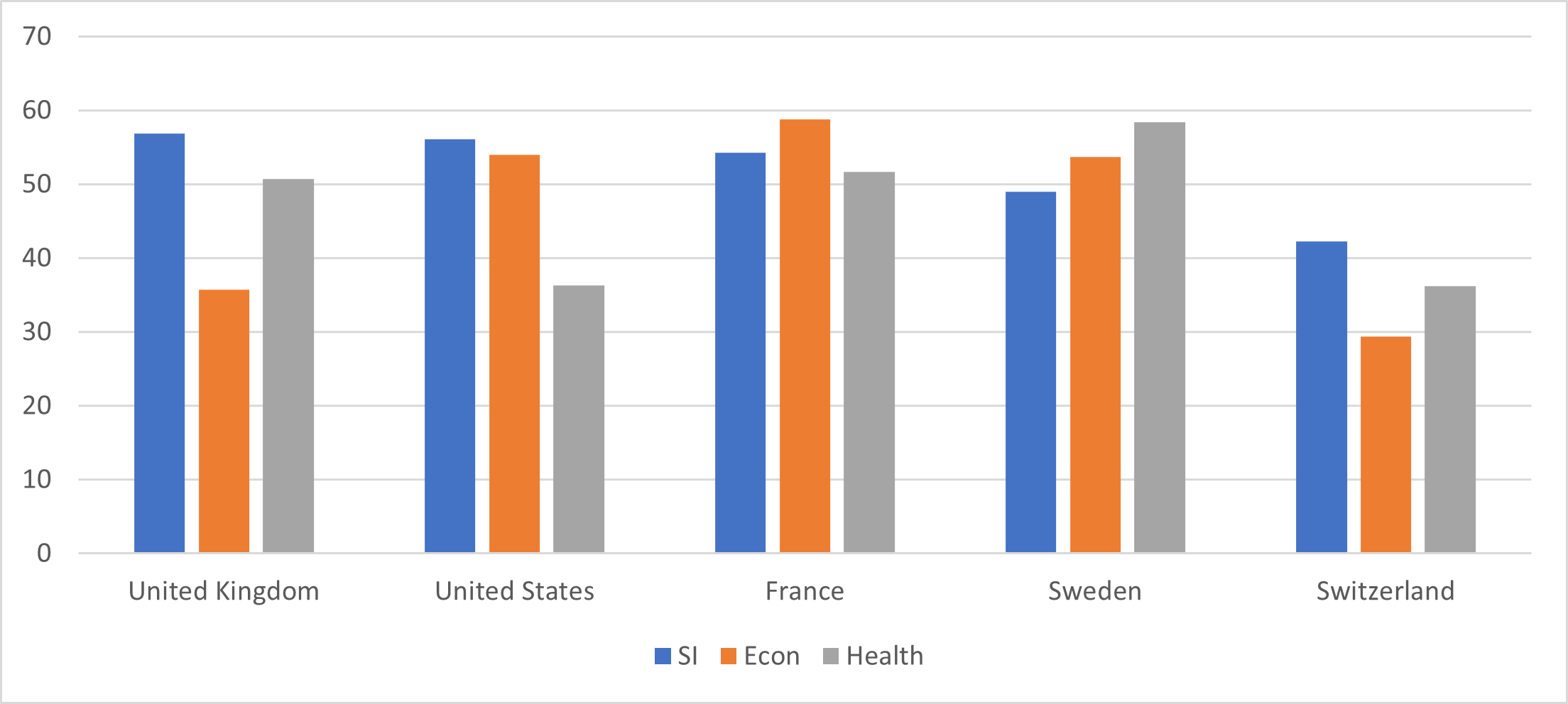

Government interventions can be classified as “Pharmaceutical Interventions (PI)”, strictly related to health, or Non-Pharmaceutical Interventions (NPI)”, including lockdown-style policies and economic support. The Oxford Covid-19 Government Response Tracker (OxCGRT) collects systematic information on policy measures that governments have taken to tackle COVID-19 and created the following three indexes measuring the intensity of government interventions in different areas:

- Containment and health index (PI, Health)

The index measures interventions as testing policy and contact tracing, short term investment in healthcare, as well investments in and adoption of vaccines. - Stringency index (NPI, SI)

The index records the strictness of ‘lockdown style’ policies that primarily restrict people’s behavior. It is calculated using all ordinal containment and closure policy indicators, plus an indicator recording public information campaigns. - Economic support index (NPI, Econ)

The index records measures such as income support and debt relief.

As illustrated in Figure 4, the five countries identified followed different strategies in terms of intervention. Switzerland is the least interventionist country, while Sweden decided not to rely a lot on lockdown-type policies, to instead privilege health and economic interventions. The UK relied a lot on policies limiting people’s mobility, while France and the US mostly used lockdown-style as well as economic support policies.

Now the question is: what is the relationship between policy intervention and economic recovery? A more rigorous analysis will determine whether and how policy instruments played a role in determining countries’ economic performance and if other structural factors have naturally protected or exposed economies to the COVID-19 shock.

[1] We separated hospitality from the other sectors because the huge contraction in hospitality would not allow to graphically evaluate the “more moderate” drops in the other sectors.

[2] In the Swiss economy, the manufacturing sector contributes to 18% of aggregate production, while the contribution of the hospitality sector equals 1.7%.